Whats Brewing in Insurance Distribution Bancassurance and Alternative

What’s Brewing in Insurance Distribution Bancassurance and Alternative Distribution Seminar 27 May 2008

2008 Bancassurance & Credit Life Survey __________________________________________________________________________________________________________________________________ Feedback Presentation Bernard Ross FIA, FASSA Executive Director: Business Development RGA Reinsurance Company of South Africa Alternative Distribution Workshop 27 & 29 May 2008 www. rgare. com

Agenda • Introduction • Section I • • • The Survey Process • Results • Changes from 2006 Survey Section II • The National Credit Act • The ‘Nienaber’ Consumer Credit Enquiry • Impact of Changing Economic Environment Questions

Introduction • Reason for survey • RGA as a bancassurance specialist • International benchmarking • External Factors • National Credit Act • Nienaber CCI • Past surveys • LOA survey in 2003 • RGA Survey 2006 – “Giving Credit Where Credit is Due” • RGA Survey 2007 – “Bridging the Cultural Divide”

Participants • Absa Life • Metropolitan Life • Ned. Group Life • FNB Life • Liberty Life & Standard Bank • Momentum Aspire • Hollard • Guardrisk • Capitec Bank • Ooba (previously MSA) • Sanlam • Regent Life • Channel Life • SA Home Loans

Data Collection • The Questionnaire • 31 questions, split across product lines • Data collected online • Included Funeral and non-Credit Life, complex underwritten business • Follow-up questions • Gross Annual Premium • Strike rates

• Changes from 2006 • Major change – data collected online")

Data Collection (continued) • Changes from 2006 • Major change – data collected online • Data scrubbed by RGA • Adjustments to the Data • Alternative Sources of Data • from National Credit Regulator – Form 45 Returns • NCR reports expected in Q 3 2008

The Survey Process • Analysed by RGA • Responses weighted by 2007 Premium • Single Premium vs. . Recurring Premium – mostly changed fully by start of year already • Double counts • Terminology

Distribution of Players Total 2007 Premium for participants estimated at R 5. 4 bn

Products Offered • Products shown as a proportion of total number of offerings in survey (total 53): • Proportion of participants offering each product (total 14):

Process Features

Underwriting • In general microloans business continues to be automatically issued. • Vehicle finance is showing slightly more underwriting being conducted. • Quite a varied response for mortgages. • Credit card business is mostly automatically issued. • For personal loans business, some questions are being asked again. • Funeral appears to be issued with basic questions. • Complex underwritten: speaks for itself.

Underwriting at claims stage • Change from 2005: • More products have moved to 12/12

Mortality Experience

")

Mortality Experience (cont. )

Morbidity Experience

Lapse Experience

Overview • Gazetted 15 March 2006 • Came into effect in stages • 1 June 2006 • 1 September 2006 • 1 June 2007 • Purposes include: • regulate credit extension market better • ensure better protection for clients (also stop reckless lending) • fairer charges, prohibit unfair credit marketing practices

• Replaces Usury Act, Integration of Usury Act Laws Act and Credit")

Overview (continued) • Replaces Usury Act, Integration of Usury Act Laws Act and Credit Agreements Act • Sees the creation of National Credit Regulator • Supersedes all regulatory bodies under Usury Act • Maintain register of all credit providers • Establish national register of credit agreements • Monitor trends in the credit market • Establish National Credit Tribunal • Several sections of the Act relate to assurers • Sections 8, 102 – 106

Impact • A significant reduction in credit life sales. • More NTU's. • Lower premium volumes due to change from SP to RP. • Increased period between grant and registration.

Background • Purpose of the Inquiry • LOA raised concerns about practices in Consumer Credit Insurance (CCI) • Highlighted by media reports • Inquiry self-appointed, with SAIA, to investigate CCI practices • Terms of reference • Improper and inappropriate marketing and distribution practices. • The payment of excessive commissions or improper fees or incentives. • The fairness of standard terms and conditions. • The adequacy of the overall value to consumers. • Pre- and post-sale disclosures and information provided to consumers. • Promoting greater consumer understanding of credit life products, their benefits and the consumer’s rights.

The Report • Important findings and recommendations • Credit Insurance is an enabler for credit extension • Inefficiencies exist • Complex interpretations of remuneration in the credit life industry • Establishment of LOA / SAIA Subcommittee to consider, inter alia: • what is due by the consumer by way of premiums • to the consumer by way of benefits and fees • the simplification and standardisation of policy terminology; • the standardisation of limitations to cover, exclusion clauses and waiting and notification periods for different product lines; • the highlighting of the health declaration; • the introduction of an industry practice of a follow-up letter; and • in the case of direct marketing, core questions and answers.

• Issues raised in the report • Deregulation of initial and")

The Report (continued) • Issues raised in the report • Deregulation of initial and / or service commissions • Regulation of credit insurance by the National Credit Regulator • Arbitrage between short- and long-term licence • Use of cell captives • Consumer education and awareness • Product value proposition

Possible Implications • Issues that remain unanswered • Fair pricing and possible profiteering • Creating better value for money • Interesting findings / Points to note • Panel and NCR views on premium and commission capping, overregulation: Source: Consumer Credit Insurance Enquiry, April 2008

Changes in Economic Environment • Interest rates have soared. • Credit extension believed to have been brought to bear • • Motor vehicles sales had dropped off significantly in second half of 2007 • Yet, SARB statistics as recent as March 08 suggested that credit lending continued to grow in the low 20%’s. This is similar to that in 2005! Oil prices and food prices are sky rocketing…

• So what to make of this? • Not")

Changes in Economic Environment (continued) • So what to make of this? • Not clear what specific impact each of the factors highlighted in this analysis had on credit life business. • Interesting to note the diversification happening, in that non -credit life sales had grown. • Clear that NCA, worsening economic conditions and resultant tightening of the credit cycle is impacting on the sale of credit life business.

Final Comments • NCA, worsening economic conditions and resultant tightening of the credit cycle have negative impact on the sale of credit life business. • Not clear what specific impact each of these factors has on credit life business. • Diversification – standalone insurance sales have grown. • NCA – impact of single vs. recurring premium • Credit Enquiry – highlights important issues going forward

Target Segments and Alternative Insurance Channels __________________________________________________________________________________________________________________________________ Johannesburg, South Africa Sean Gilday 27 May 2008 www. rgare. com

Agenda • Target Segments • Needs • Alternate Channels • Case Studies • Questions

• Typically 30 -55 • Both spouses working with")

Segments/Needs • Family Market (Mass-Affluent) • Typically 30 -55 • Both spouses working with kids • Spending and incurring debt • Disposable income can be low Looking for: 1. Mortgage cover, Credit Card Covers 2. Education plans 3. Health Coverage 4. Income replacement on death, disability, illness 5. Retirement Planning

Segment Product Solutions Sales Channel Family • Term Life, UL, Whole Life • Internet Market • Critical Illness, TPD • Bank • PHI • Agent/Broker • AD&D • Tele-sales • Credit Card, loan covers • Direct Mail Underwriting Type • For bank sales and telesales simplified • For agent and broker sales full underwriting • Variable Annuities • Long Term Care • Agent/Broker • Tele-underwriting Seniors • Guaranteed Issue Whole Life • Bank Market • Simple Premium Whole Life • Tele-Sales • Simplified and Guaranteed Issue • Payout Annuities Business • Term Life, Whole life, UL • Agent/Broker Market • Group Products • Business Banking • Disability Protection (DI, TPD) High Net Worth • Whole Life • Universal Life • Generally full underwriting including significant financial underwriting • Full financial and medical underwriting • Use smart underwriting Tele-underwriting • Para-medicals

• Typically over 65 • Close to retirement/already retired")

Segment/Needs • Seniors Market (Mass-Affluent) • Typically over 65 • Close to retirement/already retired • May have shortfall on retirement needs • May have decent assets accumulated • Needs: 1. Estate conservation 2. Funeral Expenses 3. Payout Annuities 4. Health Care –Medical and old age

Segment Product Solutions Sales Channel Family • Term Life, UL, Whole Life • Internet Market • Critical Illness, TPD • Bank • PHI • Agent/Broker • AD&D • Tele-sales Underwriting Type • For bank sales and tele-sales simplified • For agent and broker sales full underwriting • Credit Card, loan covers • Variable Annuities • Long Term Care • Agent/Broker • Tele-underwriting Seniors • Guaranteed Issue Whole Life • Bank Market • Single Premium Whole Life • Tele-Sales • Simplified and Guaranteed Issue • Payout Annuities • Direct Mail Business • Term Life, Whole life, UL • Agent/Broker Market • Group Products • Full underwriting • Generally full underwriting including significant financial • Business Banking underwriting • Disability Protection (DI, TPD) High Net Worth • Whole Life • Universal Life • Private Bank via Agent/Broker • Full financial and medical underwriting • Agent/Broker • Use smart underwriting Teleunderwriting • Para-medicals

• Family owned or limited partnership • Small Management")

Segment/Needs • Business Market (SME) • Family owned or limited partnership • Small Management Team • Under 100 employees • Needs include: 1. Group insurance –Life, Health, Pension 2. Key Man, Buy Sell, Business Continuation 3. Business Loan Cover 4. Retirement Planning

Segment Product Solutions Sales Channel Underwriting Type Family • Term Life, UL, Whole Life • Internet • For bank sales and telesales simplified Market • Critical Illness, TPD • Bank • PHI • Agent/Broker • For agent and broker sales full underwriting • Long Term Care • Agent/Broker • Tele-underwriting Seniors • Guaranteed Issue Whole Life • Bank Market • Simple Premium Whole Life • Tele-Sales • Simplified and Guaranteed Issue • AD&D • Credit Card, loan covers • Variable Annuities • Payout Annuities Business • Term Life, Whole life, UL • Agent/Broker Market • Group Products • Business Banking • Disability Protection (DI, TPD) High Net Worth • Whole Life • Universal Life • Generally full underwriting including significant financial underwriting • Private Bank via Agent/Broker • Full financial and medical underwriting • Agent/Broker • Use smart underwriting Tele-underwriting • Para-medicals

Segments/Needs • High Net Worth Market • Estate Conservation • Tax Planning • Business Coverage • Complex needs with high-end solutions • Global solutions

Segment Product Solutions Sales Channel Underwriting Type Family • Term Life, UL, Whole Life • Internet • For bank sales and telesales simplified Market • Critical Illness, TPD • Bank • PHI • Agent/Broker • For agent and broker sales full underwriting • Long Term Care • Agent/Broker • Tele-underwriting Seniors • Guaranteed Issue Whole Life • Bank Market • Simple Premium Whole Life • Tele-Sales • Simplified and Guaranteed Issue • AD&D • Credit Card, loan covers • Variable Annuities • Payout Annuities Business • Term Life, Whole life, UL • Agent/Broker Market • Group Products • Business Banking • Disability Protection (DI, TPD) High Net Worth • Whole Life • Universal Life • Critical Illness • Generally full underwriting including significant financial underwriting • Private Bank via Agent/Broker • Full financial and medical underwriting • Agent/Broker • Use smart underwriting Tele-underwriting • Para-medicals

Segment Product Solutions Sales Channel Underwriting Type Family • Term Life, UL, Whole Life • Internet • For bank sales and telesales simplified Market • Critical Illness, TPD • Bank • PHI • Agent/Broker • For agent and broker sales full underwriting • Long Term Care • Agent/Broker • Tele-underwriting Seniors • Guaranteed Issue Whole Life • Bank Market • Simple Premium Whole Life • Tele-Sales • Simplified and Guaranteed Issue • AD&D • Credit Card, loan covers • Variable Annuities • Payout Annuities Business • Term Life, Whole life, UL • Agent/Broker Market • Group Products • Business Banking • Disability Protection (DI, TPD) High Net Worth • Whole Life • Universal Life • Generally full underwriting including significant financial underwriting • Private Bank via Agent/Broker • Full financial and medical underwriting • Agent/Broker • Use smart underwriting Tele-underwriting • Para-medicals

• Direct Mail • Telesales • Internet")

Alternate Channels • Direct Response TV (DRTV) • Direct Mail • Telesales • Internet • Shop-assurance

Direct Response -Background US Life Premium by Channel, 2003 Source: Limra 2004

DRTV • Insurers have increased their spend on this channel in the last few years • 93% increase in 2006 for US spending • Both short form to long form ad campaigns • Simple to complex products • Companies use both “Hard Offers” and “Soft Offers” • Life companies use soft offers as a lead generation tool • The Hartford uses DRTV to AARP Members

DRTV –AIG Life Canada • AIG Canada • Product: Guaranteed Issue Whole Life • Target Market: Seniors • Model: DRTV and Direct Mail –”Patrick” Ad • Self Enrollment • Successful Global Model • Used by other companies in the US and Canada

DRTV –Shopping Channels Korea • Korean insurers use shopping channel approach • Use infomercials for product and needs explanation • Customers can buy over the phone after viewing the product • Done in South Africa as well

Direct Mail- Torchmark • One of the largest direct response operations in the US • Over USD 1. 5 billion in revenue • 38% of Premium comes from targeted Direct Mail as the main sales model • 8% average growth in DR premiums over 5 years • Targets middle market households

Direct Mail -Torchmark • Products: Term and Whole Life • Face offered of 5, 000/10, 000/20, 000/50, 000 • Premium and Benefits Guaranteed for life • Simple Underwriting • No medical exams • Typical 30 -day money back offer • Average face amount in 2002 was $12, 000

Torchmark –DM KSFs 1. Control of Acquisition Costs 2. Look for Economies of Scale 3. Sufficient Capital to fund campaigns 4. Strong database mining capabilities Goal: Increase Underwriting Profit

Direct Mail -Torchmark’s DR Operating Performance, 2004 Source: 2004 Torchmark Annual Report

Outbound Telephone-Inbursa • Large Mexican-based conglomerate • Have banking, insurance and telecommunications • Targeted telco customers with simple life offer • Small face amount with simple underwriting • High Take-up rates • Premiums added to phone bill

Outbound Telephone –BMO Life • Large Canadian Bank • Over 4 million retail banking customers • Developed call centre outbound tele-sales solution • Use bank’s database to target market customers • Have full tele-underwriting • Good Straight through processing model • Term life –pick your term

Inbound Telephone –Direct Line • UK-based company • Short Term and Long Term • Developed inbound model with strong advertising and branding campaign • Sell Term and CI • Known to tweak program daily

Inbound Telephone –Direct Line • Use a preferred underwriting model • “Life-style” factor preferred model (not US style medically preferred) • Allows them to offer discounts • The underwriting rules, scripts and process was set up to be very flexible – they could change it over night! (including the associated rate changes) • Mail • Send a letter to the customer a post-sale Welcome Letter

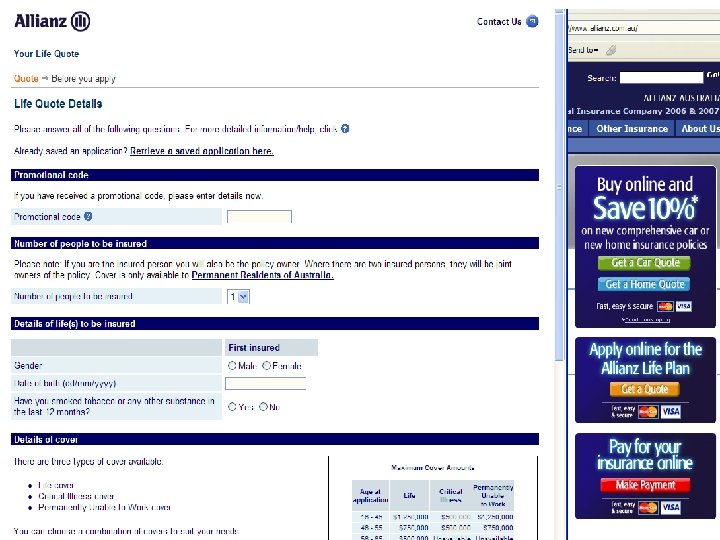

Internet Sales –Allianz Australia • Online Sales of Short Term and Long Term • To develop a direct life insurance offer to compete with the IFA channel • Sell Life, TPD, and CI • Up to AUS$1. 25 million life and TPD, 500, 000 CI • Will issue full face amount without fluids or medical • Use drill-down full underwriting model

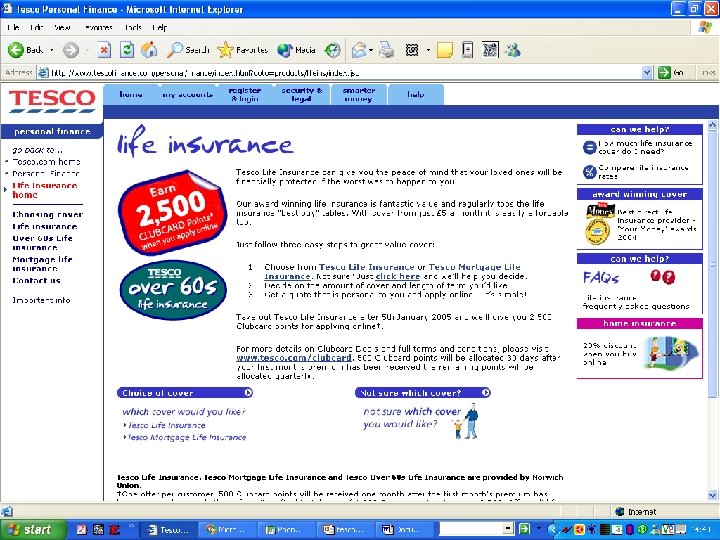

Internet Sales –Shop-assurance • Web & phone with in-store & TV advertising • Term Cover (+CIC) – underwritten • Over 60’s – guaranteed acceptance • In store – self underwriting? • 20 to 39, 5 year age bands • T 10, £ 100, 000 cover only • Sex & smoker differentiated • The in-store product is totally different from any other UK product

Key Success Factors • Executing on Customer Needs • Matching product to customer needs and sales model • Ensuring quick and easy sales process • Use modern underwriting methodologies • Try to make insurance sale “transactional” • Sales Management • Use the most effective sales models • Continuous access to sales people for training and advice • Create and use effective needs-based insurance sales approaches where possible

- Slides: 65