What is Economics How do economists study the

- Slides: 17

What is Economics? How do economists study the ways people make decisions on how to use their time, money, and resources?

Economic Choices � Responsible citizens make economic decisions everyday. We have to make these choices because we have limited resources. � Economics is the study of how people make decisions in a world of limited resources. � Scarcity - Needs: things we must have in order to survive Food, Water, Shelter, Clothing - Wants: things we can live without but find desirable. - Scarcity: the fact that we do not have enough resources (water, food, money, time) to satisfy everyone’s needs and wants. Think “Musical Chairs”.

Goods and Services � Goods: tangible objects that we use to satisfy our wants and needs � Examples of goods: pencil, candy bar, computer, car, etc. � Durable Good: a good that can be used repeatedly, or yields benefits over a long period of time. - Examples: cars, washing machine, computers � Non-durable Good: Goods that either can only be used once, or yield a benefit for less than three years. - Examples: food, office supplies, cosmetics, gasoline. � Services: work that is performed for someone else. � Examples of Services: haircut, landscaping, babysitting, drycleaner, etc.

The Four Factors of Production The 4 resources necessary to produce goods and services 1. Natural Resources: all of the “gifts of nature” that make production possible EX: 2. Labor aka Human Resources: physical and mental efforts that people contribute to the production of goods and services 3. Capital/Capital Goods: tools, machinery, and goods used to make other things 4. Entrepreneurs: individuals who start new businesses, introduce new products, and improve management techniques

Economy and Economic Models Economy: all of the activity in a nation that affects the production, distribution, and use of goods and services. Economists use models (usually graphs and tables) to try to predict how things will play out in the economy. One of the most important models is the “Production Possibilities Model/Curve”. It shows what things can possibly be produced at a given time. It is easier to create models that are simplified, so let’s assume our economy is only producing two goods: i. Pods and Industrial Robots.

Production Possibilities Table i. Pods Industrial Robots A 0 10 B 1 9 C 2 7 D 3 4 E 4 0

Production Possibilities Curve The Production possibilities curve is a graphical representation of the table. - Points on the curve represent maximum possible combinations of two goods given resources and technology. - Points inside the curve represent underemployment or unemployment - Points outside the curve are unattainable at present If we assume we have a set number of resources to produce goods, this model shows us that we are limited in the number of a certain good we can produce. When we choose to produce more of one good, we must give up production of the other.

-1 +1

Making Economic Decisions Trade Offs: the alternative you face if you decide to do one thing rather than another. You cannot do more than one activity at a time. By deciding to do something, you are also deciding not to do several other possible things. You face trade-offs in deciding how to spend your time and money. Society faces trade-offs in determining how to distribute scarce resources.

Making Economic Decisions Whenever you make a decision to spend money or time, you are costing yourself the opportunity to do many other things, but you could only have done of those trade-offs. Opportunity Cost: A specific type of trade-off; if you list all of the trade offs for a specific decision, the opportunity cost is trade off which you would most like to do if you had not made your decision. It is the next best alternative to the thing you actually chose. The Production Possibilities Model shows the opportunity cost a society faces when deciding to produce one good over another.

Cost-Benefit Analysis How can businesses and individuals make good economic decisions?

Cost-Benefit Analysis All people and producers of goods and services must consider how they will spend their time or how many units of a good or service to produce. The best way to do this is to consider the costs and benefits of each possibility. Production Costs: - Fixed Cost: money that must be paid no matter how many units are produced. Ex: you must pay the rent/mortgage, and taxes on your factory whether you produce 500 units or 0 units. - Variable Cost: The additional money (on top of fixed cost) that must be paid to produce. The amount changes as the number of units produced change. - Total Cost (TC): Fixed Cost (FC) + Variable Cost (VC). Businesses often focus on the Average Total Cost divided by the number of units produced. - Marginal Cost: The additional money that must be paid in order to produce one more item. Marginal Cost (MC) = TC producing two units – TC producing one unit

C-B Analysis �continued… Revenue/Benefit: the money brought in by a business by selling their goods and services. - Total Revenue: all revenue brought in from sales TR = Price x # of units sold - Marginal Revenue: additional revenue brought in by selling one more unit. MR always equals price �Analysis: compare Marginal Cost to Marginal Revenue to determine the number of units to produce. Businesses produce and sell goods to make a profit. You make a profit by bringing in more revenue than money spent to produce - If MC is less than MR, always produce at least one more unit. - If MC is greater than or equal to MR, don’t produce that # of units.

C-B Analysis of Widget Factory: Assume widgets sell for $300 each # of Units Fixed Cost Variable Cost Total Cost Marginal Total Cost Revenue Marginal Revenue 0 100 100 0 - 1 100 500 600 500 300 2 100 800 900 300 600 3 100 1, 000 1, 100 200 900 300 4 100 1, 160 1, 260 1200 300 5 100 1, 340 1, 440 180 1500 300 6 100 1, 540 1, 640 200 1800 300 7 100 1, 780 1, 880 240 2100 300

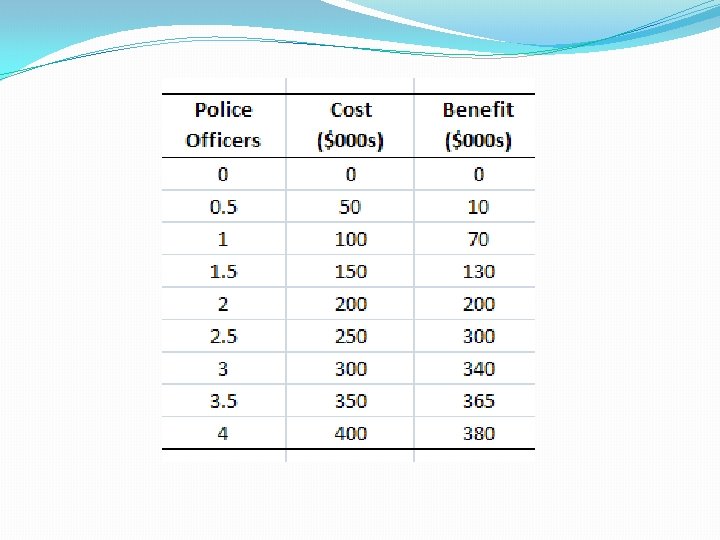

Individual C-B Analysis When you make decisions about how to spend your time and money, it is smart to consider costs and benefits as well. Look at your possible decisions and determine the total cost of each. Consider not only the monetary cost of a decision, but also time and activities given up. Determine the benefits of each decisions as well. An easy way to do this is to ask yourself how much someone would have to pay you to not make the purchase/activity. Good economic decision makers only choose options where the benefits outweigh the costs.

C-B Analysis of Widget Factory: Now lets make things more complicated: each unit sells for $10 less than the previous unit # of Units Fixed Cost Variable Cost Total Cost Marginal Total Cost Revenue Marginal Revenue 0 100 100 0 - 1 100 500 600 500 300 2 100 800 900 300 590 290 3 100 1, 000 1, 100 200 870 280 4 100 1, 160 1, 260 1, 140 270 5 100 1, 340 1, 440 180 1, 400 260 6 100 1, 540 1, 640 200 1, 650 250 7 100 1, 780 1, 880 240 1, 890 240 8 100 2, 140 2, 240 260 2, 120 230