What Is Agency Theory Agency theory is the

,")

- Slides: 14

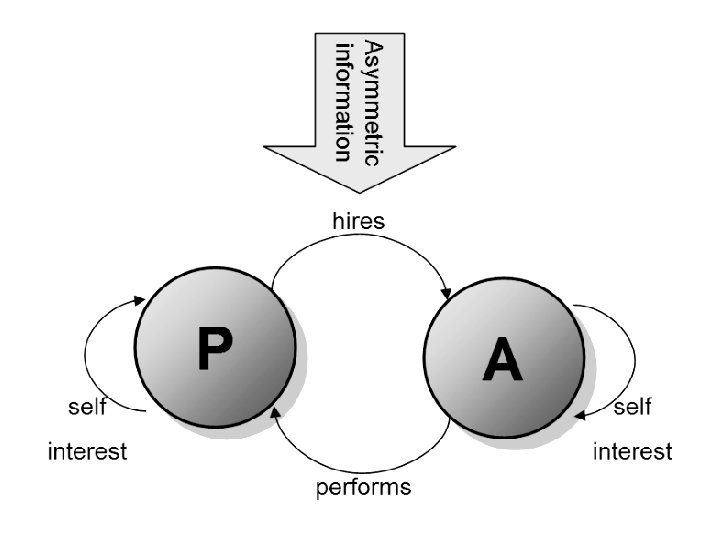

What Is Agency Theory ? Agency theory is the branch of financial economics that looks at conflicts of interest between people with different interests in the same assets. • • This most importantly means the conflicts between: shareholders and managers of companies shareholders and bond holders. The theory explains the relationship between principals, such as a shareholders, and agents, such as a company's managers. In this relationship the principal delegates (or hires) an agent to perform work. • • The theory attempts to deal with two specific problems: how to align the goals of the principal so that they are not in conflict (agency problem), and that the principal and agent reconcile different tolerances for risk.

Origins Of agency Theory ? During the 1960 s & 1970 s , economists explored risk sharing among individuals or groups. This literature described the risk sharing problem as one that arises when co-operating parties have different attitudes toward risks. Agency Theory broadened this risk sharing literature to include the so called agency problem that occurs when co-operating parties have different goals and division of labour. Specifically, this theory is directed at the ubiquitous agency relationship , in which one party delegates work to another agent who performs that work. Agency Theory attempts to describe this relation using the metaphor of a contract. Agency Theory suggests that the firm can be viewed as a nexus of contracts (loosely defined) between resource holders.

CONFLICTS BETWEEN MANAGERS AND SHAREHOLDERS Why conflict of interest between shareholders and management? To address the conflict of interest between shareholders and management, it is important to stress that even within the same class of shareholders, there may be conflicts, this conflict may relate to what proportion of the company’s profit should be paid in the form of dividend and what proportion should be retained for future investments and for capital investment purposes. Other potential conflicts may involve company’s ethical policies, its corporate and social responsibilities policies. The agency theory, considering the potential conflicts of interest between shareholders and management may arise as a result of several factors, some of such factors include: Reward to management Risk attitudes of management and shareholders Takeover decisions by management Time horizon of management

SELF-INTERESTED BEHAVIOR Agency theory suggests that, in imperfect labor and capital markets, managers will seek to maximize their own utility at the expense of corporate shareholders. Agents have the ability to operate in their own self-interest rather than in the best interests of the firm because of asymmetric information (e. g. , managers know better than shareholders whether they are capable of meeting the shareholders' objectives) and uncertainty (e. g. , myriad factors contribute to final outcomes, and it may not be evident whether the agent directly caused a given outcome, positive or negative). Evidence of self-interested managerial behaviour includes the consumption of some corporate resources in the form of perquisites and the avoidance of optimal risk positions, whereby risk-averse managers bypass profitable opportunities in which the firm's shareholders would prefer they invest. Outside investors recognize that the firm will make decisions contrary to their best interests. Accordingly, investors will discount the prices they are willing to pay for the firm's securities.

The interest of shareholders may include: • • • Increasing earning per share (EPS), and current share prices Increasing investor ratios such as dividend per share (DPS), dividend cover, dividend yield, price-earning (P/E) ratio Others may include the company improving its corporate and social responsibilities Management interest may include: • Managing the firm to achieve its objectives • Increasing the wealth and size of the company, by expanding the company’s activities, the bigger the size of the company they manage the better they are perceived to be. • Increasing their personal wealth by paying themselves high remunerations and other benefits

COSTS OF SHAREHOLDER-MANAGEMENT CONFLICT Agency costs are defined as those costs borne by shareholders to encourage managers to maximize shareholder wealth rather than behave in their own self-interests. There are three major types of agency costs: (1) expenditures to monitor managerial activities, such as audit costs; (2) expenditures to structure the organization in a way that will limit undesirable managerial behaviour, such as appointing outside members to the board of directors or restructuring the company's business units and management hierarchy; and (3) opportunity costs which are incurred when shareholder-imposed restrictions, such as requirements for shareholder votes on specific issues, limit the ability of managers to take actions that advance shareholder wealth.

MECHANISMS FOR DEALING WITH SHAREHOLDER-MANAGER CONFLICTS There are two polar positions for dealing with shareholder-manager agency conflicts. At one extreme, the firm's managers are compensated entirely on the basis of stock price changes. In this case, agency costs will be low because managers have great incentives to maximize shareholder wealth. It would be extremely difficult, however, to hire talented managers under these contractual terms because the firm's earnings would be affected by economic events that are not under managerial control. At the other extreme, stockholders could monitor every managerial action, but this would be extremely costly and inefficient. (1) (2) (3) (4) The optimal solution lies between the extremes, where executive compensation is tied to performance, but some monitoring is also undertaken. In addition to monitoring, the following mechanisms encourage managers to act in shareholders' interests: performance-based incentive plans, direct intervention by shareholders, the threat of firing, and the threat of takeover.

STOCKHOLDERS VERSUS CREDITORS: A SECOND AGENCY CONFLICT In addition to the agency conflict between stockholders and managers, there is a second class of agency conflict between creditors and stockholders. Creditors have the primary claim on part of the firm's earnings in the form of interest and principal payments on the debt as well as a claim on the firm's assets in the event of bankruptcy. The stockholders, however, maintain control of the operating decisions (through the firm's managers) that affect the firm's cash flows and their corresponding risks. Shareholder-creditor agency conflicts can result in situations in which a firm's total value declines but its stock price rises. This occurs if the value of the firm's outstanding debt falls by more than the increase in the value of the firm's common stock.

AGENCY VERSUS CONTRACT Although the notions of agency and contract are closely intertwined, some academics bristle at the suggestion they are essentially the same. A conventional view holds that agency is a special application of contract theory. However, some argue that the reverse is true: a contract is a formalized, structured, and limited version of agency, but agency itself is not based on contracts

AGENCY AND ETHICS Since agency relationships are usually more complex and ambiguous (in terms of what specifically the agent is required to do for the principal) than contractual relationships, agency carries with it special ethical issues and problems, concerning both agents and principals. Ethicists point out that the classical version of agency theory assumes that agents (i. e. , managers) should always act in principals' (owners') interests. However, if taken literally, this entails a further assumption that either: (a) (b) the principals' interests are always morally acceptable ones or managers should act unethically in order to fulfill their "contract" in the agency relationship. Clearly, these stances do not conform to any practicable model of business ethics.

Key idea • Principal-agent relationships should reflect efficient organization of information and risk-bearing costs Unit of analysis • Contract between principal and agent Human assumptions • Self-interest • Bounded rationality • Risk aversion Organizational assumptions • Partial goal conflict among participants • Efficiency as the effectiveness criterion Information asymmetry between principal and agent Information assumption • Information as a purchasable commodity Contracting problems • Agency (moral hazard and adverse selection) • Risk sharing Problem domain • Relationships in which the principal and agent have partly differing goals and risk preferences (e. g. , compensation, regulation, leadership, impression management, whistle-blowing, vertical integration, transfer pricing)

THANK YOU