Welcome Tony Craddock tony craddockemergingpayments org EPAssoc Tony

- Slides: 27

Welcome Tony Craddock tony. craddock@emergingpayments. org @EPAssoc @Tony. Craddock t: +44 20 7378 9890 m: +44 7803 203405

Our members Benefactors Members: Patrons

And to our Advisory Board and Ambassadors Our Advisory Board John Davies CEO, Just Loans Group Our Ambassadors Rich Wagner Chairman of EPA Founder and CEO, APS Financial Andrea Dunlop Deputy Chair, EPA, CEO, Card Solutions & Acquiring, Paysafe Tony Craddock Director General, EPA John Campbell, The Plenderleith Partnership John Bohan, Jigsaw Business Solutions David Carr, European Prepaid Limited Peter Cocks, Consulting Stream Neira Jones, Phoenix Edge Chris Dunne Payment Services Director, Vocalink Monica Eaton. Cardone CIO, Chargebacks 911 Siân Jones, COINsult Mark Mc. Murtrie, Payments Consultancy Ross Musgrove, Musgrove Consulting David Parker, Polymath Consulting Sarah Francis, Freelance Nadja Van Der Veer, Payment Counsel David Hunter Non Executive Director, W 2 Neira Jones Independent Advisor Anders la Cour CEO, Saxo Payments Mike Laven CEO, Currency Cloud Kriya Patel Managing Director, Bancorp Inc. Anne Pieckielon Director of Product & Strategy, Bacs Judith Rinearson Partner, K & L Gates Myles Stephenson CEO, Modulr Andrea Mc. Geachin, Amack Consultants Morten Bebe, Coinfy Rohit Bhatnagar, Leadership Trail Suresh Vaghjiani Executive Vice President, GPS

ACCESS

Inadequate access in three areas ACCESS CONSUMER ACCESS BUSINESS ACCESS INDUSTRY ACCESS

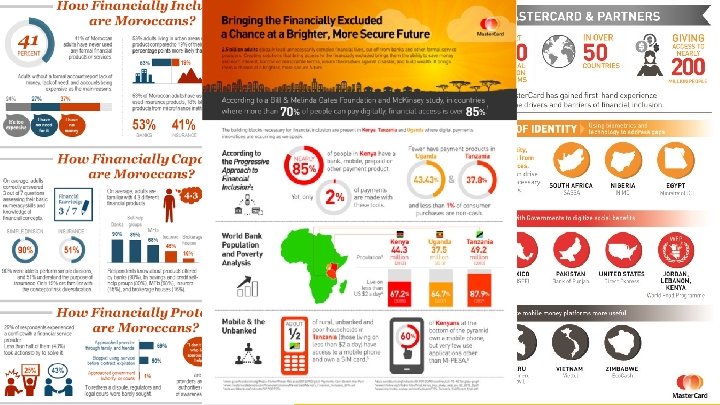

Access to accounts for consumers

It’s not just payments

Financial inclusion has made a difference

UK also has a financial inclusion problem £ 1, 300 1. 5 m the financially excluded pay a ‘poverty premium’ of £ 1, 300 each year 1 adults without a bank account in the United Kingdom 2 78% of people likely to be eligible for Universal Credit would need help managing monthly payments 3

EPA members § BACS and the Social Foundation for Inclusion – ‘Switching the measure’ § Access for consumers is a significant problem even in developed countries

Access is denied in three areas ACCESS CONSUMER ACCESS BUSINESS ACCESS INDUSTRY ACCESS

Access for SMEs and micro-businesses

Made by hand by Wolof women in the Thiès region of Senegal, West Africa and imported directly from the weavers

But access is prevented § Account withdrawn by HSBC with no notice – No reason given § Local correspondent bank – Delay, over-charging, confusion § International remittance using Western Union – High costs, reconciliation errors § Maersk Line’s global cyber attack in June – Container lost for 7 weeks

§ § Artisanne is a winner But will our industry allow them to win?

Access is denied in three areas ACCESS CONSUMER ACCESS BUSINESS ACCESS INDUSTRY ACCESS

Access for Financial Services companies § Access to products, services, accounts, expertise and funding all constrained through combination of: – Old ‘technology’ • IT such as RTGS, mindset, processes, reporting – Monopolistic pressures – Fear of change • Regulators, incumbents, new entrants – Weakness of new entrants • Inexperienced • No common voice – De-risking by banks due to market failure

De-risking § § De-risking represents a clear instance of market failure Regulators are scrambling to catch up with the current money laundering and terrorist financing landscape As a result, they are increasingly shifting monitoring burdens to financial institutions The customer base is feeling the brunt of this shift

Good news § We’re making some progress 1. Consumers 2. Businesses 3. Industry

The EPA’s Projects set out to enable access With the help of our Benefactors

EPA’s project teams contain 84 volunteers EPA Projects: 1. Financial Inclusion 2. Retail 3. Media 4. Regulator 5. International Trade 6. Rome 7. Women in Pay. Tech 8. Futures Consumers Businesses FS Industry

The EU

By solving the access problem, we can change lives Tony Craddock tony. craddock@emergingpayments. org @EPAssoc @Tony. Craddock t: +44 20 7378 9890 m: +44 7803 203405