Welcome to the Federal Reserve Bank of Dallas

Welcome to the Federal Reserve Bank of Dallas Business Continuity Department

The Federal Reserve America’s Central Bank Princeton Williams Director of Economic Education The views expressed are those of the presenter and not necessarily those of the Federal Reserve Bank of Dallas or the Federal Reserve System.

is the central")

What is the Fed? • The Federal Reserve System (the Fed) is the central bank of the United States • It was founded by Congress in 1913 in response to the nation’s recurring banking panics

The Federal Reserve Act of 1913 “ To provide for the establishment of Federal reserve banks, to furnishing elastic currency, to afford means of rediscounting commercial paper, to establish a more effective supervision of banking in the United States, and for other purposes. ”

Other Central Banks Bank of England 1694 Bank of Japan 1882 Federal Reserve 1913 European Central Bank 1998

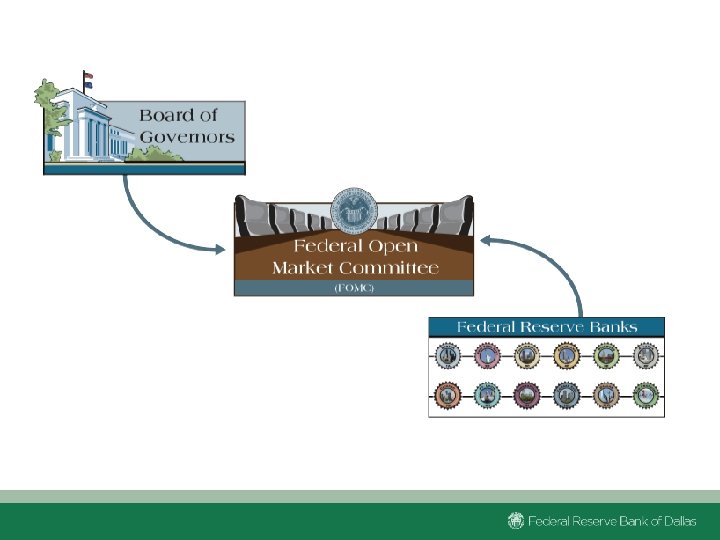

Structure of the Federal Reserve Board of Governors Regional Banks Federal Open Market Committee

Board of Governors Stanley Fischer Daniel K. Tarullo Open Jerome H. Powell Lael Brainard Open Janet Yellen Chair

Federal Reserve Banks

Who owns the Federal Reserve Bank of Dallas?

District Board of Directors Three nonbankers appointed by the Board of Governors to represent the public Three bankers Three nonbankers elected by member banks to represent member represent the banks public

The Eleventh District El Paso Houston Dallas San Antonio

Federal Open Market Committee

Federal Reserve Functions • Supervise and regulate banks • Provide financial services • Conduct monetary policy

Supervision vs. Regulation What is the difference between supervision and regulation?

Goals Safe and sound financial institutio ns Financial stability Fair and equitable treatment of consumer s

Institutions the Fed Supervises Holding companies State memberbanks Foreign branches of U. S. banks U. S. branches of foreign banks Some payment, clearing and settlement systems

Financial Services How has the world of payments changed over time?

Financial Services Bank for Banks • Cash services • Electronic payments • Check processing

Financial Services Bank for U. S. Treasury • Banking services • Issue, transfer and redeem U. S. government securities

Monetary Policy

Monetary Policy The actions of a central bank that influence the availability and cost of money and credit to achieve national economic goals.

The Fed’s Congressional Mandate Maximum employment Stable prices Moderate long-term interest rates

Achieving the Goal Availability and cost of money and credit Consumer and business spending Employment and prices

Monetary vs. Fiscal Policy Monetary Policy Fiscal Policy • Conducted by the Fed • Availability and cost of money and credit • Congress and president • Tax policy and spending decisions

Structure Board of Governors Regional Reserve Banks FOMC Function s Supervise and regulate banks Provide financial services Conduct monetary policy

Questions? Next Topic : Federal Reserve Financial Services in Times of Disaster

Federal Reserve Financial Services in Times of Disaster North Texas Association of Contingency Planners Aug. 2, 2016 28

Six Payment Types � Cash � Check � Wire � ACH � Credit Card � Debit Card 29

The Role of the Federal Reserve • Ensure the safety, efficiency, and accessibility of the U. S. payments system • “Bank for banks” Monetary Policy Financial Services Banking Supervision ◦ Currency and coin ordering ◦ “Wholesale” payments (Fedwire and book-entry securities) ◦ “Retail” payments (check clearing and ACH) ◦ Settlement • “Fiscal agent” for the U. S. Treasury ◦ Maintain accounts for the U. S. Treasury ◦ Process government checks ◦ Disburse electronic Social Security benefits, tax refunds, etc. 30

provides system leadership")

The Role of the Federal Reserve The Cash Product Office (CPO) provides system leadership and direction for the Federal Reserve’s cash business. The Wholesale Product Office (WPO) manages Fedwire Funds, Fedwire Securities and the National Settlement Service. Roughly $35 m passes through Fedwire Funds every second! The Customer Relations and Support Office (CRSO) manages Fed. Line and provides customer set-up and support. The Retail Payments Office (RPO) processes paper and electronic check payments and electronic exchange of debit and credit transactions through the ACH network. Processes $98. 6 b in ACH transactions and $32. 9 b in checks per day. 31

Fed. Line � Secure electronic payments delivery network � Provides FIs access to Federal Reserve Financial Services (FRFS): ◦ Cash ◦ Check ◦ Fedwire ◦ Fed. ACH 32

system � Participants initiate funds transfers")

Fedwire Funds Service � Real-time gross settlement (RTGS) system � Participants initiate funds transfers that are immediate, final, and irrevocable once processed � Credit transfers only � Typically used for high-dollar transactions and/or transactions with a need for immediate funds availability � Financial institution must hold a Fed account to be eligible to participate 33

◦")

Fedwire Funds Service � Funds transfers may be originated: ◦ Online (Fed. Line) ◦ Offline (telephone) 34

� Nationwide network � Open to all FIs � Batch")

Automated Clearing House (ACH) � Nationwide network � Open to all FIs � Batch processing, “store-and-forward” � Credits and debits � Settlement takes place the next business day ◦ ACH credits can be sent to the Fed 1 or 2 days in advance of the intended settlement date; debits only 1 day in advance � Two ACH operators: ◦ The Federal Reserve ◦ Electronic Payments Network (EPN; parent company is The Clearing House) 35

FRFS Business Continuity � Each FRB business function has prepared business continuity plans to address various types of disaster scenarios. ◦ Internal ◦ External � Plans are continuously tested and updated as new threats become apparent 36

Cash Business Continuity � E. g. , Hurricane Katrina: FRB Atlanta and Memphis Branch (of FRB STL) backup for cash processing at New Orleans Branch � Hurricane Rita: Dallas and San Antonio offices prepared to back up Houston Branch as needed 37

Resiliency Statement � The Federal Reserve Banks’ Resiliency Statement ◦ Intended to provide assurance regarding our readiness to provide BC during emergency situations ◦ National Business Continuity Guide ◦ Fedwire Funds & Securities Business Resiliency Statement ◦ Fed. ACH Business Resiliency Statement 38

Fedwire Business Continuity � Out-of-region backup facilities for Fedwire applications and all integral support and related functions � Routine test of Fedwire BC procedures across a variety of contingency situations (unavailability of facilities, hardware, network, staff) � Fedwire applications and associated recovery procedures are regularly enhanced and tested to address various emerging risk scenarios ◦ E. g. , pandemic 39

Fedwire Business Continuity � Offline wires ◦ NOTE: This is not a valid contingency solution in the case of a major outage, due to limited number of staff able to accept incoming calls. 40

Fed. ACH Business Continuity � Two data processing centers ◦ Primary ◦ Active, “warm-site” backup facility � � Separately located to mitigate the effects of natural disasters; power/telecomm outages. Both include various contingency features: ◦ Redundant power feeds ◦ Environmental and emergency control systems, ◦ Dual network operations centers ◦ Dual customer service centers ◦ Data backup 41

Fed. ACH Business Continuity � Fed. ACH Agreement, Part 4: Sending Point and Receiving Point Contingency Information ◦ Formerly known as Alternate Access Point or “Buddy Bank” 42

9/11 � Fedwire and Fed. ACH: Continued to run smoothly throughout the country – Electronic payments were unaffected � Cash: Fed arranged with NYC Police and NJ State Troopers to deliver more than $425 m to keep local banks and ATMs stocked with cash � Checks: Majority of checks required air transportation for clearing o At that time 55 m checks per day were delivered by ground air transportation to processing sites 43

9/11 � Planes not allowed to fly for several days � The Fed accepted and credited FIs’ checks even though we could not clear a large majority of those checks ◦ Sept. 12: Fed incurred ~$23 b worth of “float” ◦ About 30 times our historical daily average, to provide liquidity for the payments system 44

Impact of 9/11: “Check 21” � After 9/11 disruption Fed worked with Congress to draft legislation giving a “substitute check” the legal equivalency of the original physical item for the purpose of collection and presentment � Led to passage of Check Clearing for the 21 st Century Act (a. k. a. “Check 21”) in 2003 o o Allowed checks to be collected electronically Electronic check collection has now become the primary method for collecting checks 45

c d p es k c s 0 at h e r 21 ec ese d b 45 03, t kc ” ◦S n y h l o t e oll ed the inc ca F e t ec ion d h us at e e Fe t i i the arl s ad o dt n n g y ch od At se t h ec lan 2010 rvi e F a k ta -p , ce ed Fe pap roc s ’s d er e n 2 ic ch e ck s are ssi ng pr oc op era ti es se do nly

Non-Fed Rules and Regulations � E. g. , NACHA Operating Rules contain language around permissible late return items 47

“Cyber 9/11”? 48")

Physical vs. Cyber Attack � Physical Attack (9/11) “Cyber 9/11”? 48

Supervisory Practices… � FRB Supervisory Letter SR 13 -6/CA 13 -3 � “Supervisory Practices Regarding Banking Organizations and their Borrowers and Other Customers Affected by a Major Disaster or Emergency” (March 29, 2013) ◦ Working with Borrowers and Other Customers �Waiving ATM fees for customers/non-customers �Increasing ATM daily cash withdrawal limits �Waiving overdraft fees, etc. ◦ Beware of potential for increased fraud 49

Questions? Matt Davies, AAP, CTP, CPP Assistant Vice President Federal Reserve Bank of Dallas Phone: 214 -922 -5259 E-mail: matt. davies@dal. frb. org 50

- Slides: 50