Week 10 Economics I Topics of Week 10

– Jerry convinces Babu to")

Number of Customers (Q) Total")

Price/Month (P) Number of Customers (Q)")

Price/Month (P) Number of Customers (Q) Total Revenue")

$180 165 150 135 120 105 90 75 60 45")

cartel • 1988")

, 1")

- Slides: 71

Week #10 Economics I

Topics of Week #10 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. 11. 12. 13. 14. 15. 16. 17. Monopolistic Competition* Comparing Market Structures* Product Differentiation Forms Monopolistic Competition in Short-run* Monopolistic Competition in Long-run* Markup* Long-run Equilibrium* Scale and Output Excess Capacity and Efficiency* Advertising* Oligopoly* Comparing Market Structures* Concentration Ratio Duopoly* Cartel* Mutual Interdependence Oligopoly with More than Two Firms* "*" Indicates the most important topics. Mateer and Coppock: Chapter #12 and #13

Previously • Price discrimination – Occurs when a firm sells the same good at different prices. – Will increase firm profitability. – Can increase economic efficiency. • General rule for price discrimination – Charge a higher price to relatively inelastic consumer group – Charge a lower price to relatively elastic consumer group

Big Questions 1. What is monopolistic competition? 2. What are the differences among monopolistic competition, competitive markets, and monopoly? 3. Why is advertising prevalent in monopolistic competition?

What Is Monopolistic Competition? • Monopolistic competition – A market structure characterized by • Free entry and exit • Many different firms • Product differentiation – The process that firms use to make a product more attractive by contrasting its unique qualities with competing products.

Comparing Market Structures Perfectly Competitive Markets Monopolistic Competition Monopoly Many sellers One seller Similar products Differentiated products A unique product without close substitutes Free/Easy entry and exit High barriers to entry and exit

Product Differentiation Forms • What are some ways firms differentiate their products? • 1. Style or type – Clothing stores – Food court at mall • 2. Location – Gas stations – Dry cleaners – Barber shops

Product Differentiation Forms • 3. Quality – Low quality versus high quality – Taco Bell versus Baja Fresh – Subway versus Quiznos – Mc. Donald's versus White Castle • Trade-off: – Lower quality, lower prices, faster service – Higher quality, higher prices, slower service

Economics in Seinfeld • "Seinfeld" – "The Café" (1991) – Jerry convinces Babu to serve Pakistani food—he'll be the only Pakistani restaurant in the neighborhood. When the restaurant fails, Jerry blames it on a bad location.

Monopolistic Competition in the Short-Run and Long-Run • Monopolistically Competitive Firm – Sells a differentiated product. – Has market power. – Uses profit-maximizing rule of MR = MC. – Charges a price on the demand curve corresponding to this point, and P > MC. – Long-run profits will depend on firm entry and exit. Generally, there is free/easy entry and exit which causes zero long-run profits.

Monopolistic Competition in the Short-Run

Monopolistic Competition in the Short-Run • Graph summary – Firm chooses output level where MR = MC – The price is determined by the height of the demand curve at this level of output. – Firm could make a profit or loss. This depends on whether price is greater than or less than the ATC of production at the profit-maximizing output level.

Monopolistic Competition in the Long-Run

Monopolistic Competition in the Long-Run • Graph summary – A key idea is free/easy entry and exit. – If the industry is profitable, other firms will enter, causing the demand for existing firms' products to decrease. – If the industry is experiencing losses, firms will exit, causing demand for remaining firms' products to increase. – Entry and exit will stop when profits are zero. This occurs when P = ATC. – Check this website for long-run adjustments.

Relationship between Price, Marginal Cost, and LRATC • Markup – The difference between P and MC – Markups are possible when a firm has market power and sells a differentiated product. – Results in consumers paying more • Price, Marginal Cost and Long-Run ATC – – Monopolistic competition: P > MC Monopolistic competition in the Long-run: P > min ATC Perfect competition: P = MC Perfect competition in the Long-run: P = min ATC

Long-Run Equilibrium in Two Market Structures

Scale and Output • Excess capacity – Firms are relatively small, so they are not at the output level where ATC is minimized. • Why not produce more? – To sell more, the firm would have to lower the price of output. It is more profitable to produce at excess capacity (below efficient scale). • Compare to perfect competition – Perfectly competitive firms operate at capacity at the minimum of ATC. Overall output is higher in perfect competition.

Inefficiency and Social Welfare • Two sources of inefficiency in monopolistic competition – ATC is higher compared to perfect competition. • Firm could lower the price it charges and sell more. – Markup • P > MC • If the firm tries to set P = MC, the level of output sold would occur where ATC > P, and the firm would lose profits.

Inefficiency and Social Welfare • Could government intervention be helpful? – Due to free entry, firms are not able to earn long-run profits like monopolists. – Regulation may put many firms out of business. • Less firms may mean more inconvenience and fewer choices for consumers. • Already have seen problems of marginal cost pricing regulation – Inefficiency not large enough to warrant government intervention

Is the Inefficiency So Bad? • Perfect competition – – Lower prices Higher quantities Efficiency (P = MC, minimum ATC) Homogenous products (no variety) • Monopolistic competition – – Slightly higher prices Slightly lower quantities Inefficiency (P > MC, not at minimum ATC) Differentiated products (variety and choice)

Varying Degrees of Product Differentiation • A highly differentiated product means – Higher prices and markups. – Larger excess capacity. • A less-differentiated product means – Lower prices and markups. – Less excess capacity.

Differentiation, Excess Capacity, and Efficiency

Economics in “Hugs” • “Free Hugs Prank: $2 Deluxe Hugs” – Is a $2 hug better than a free hug?

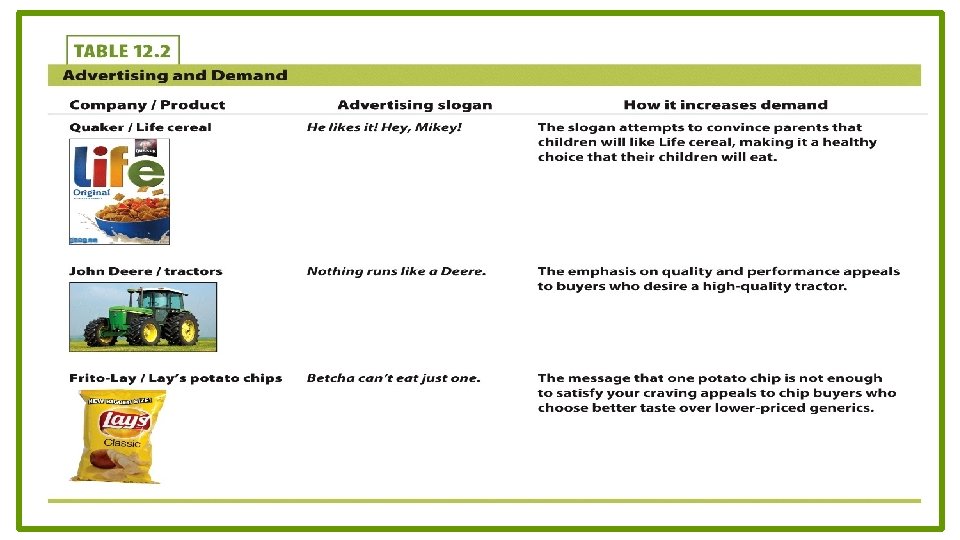

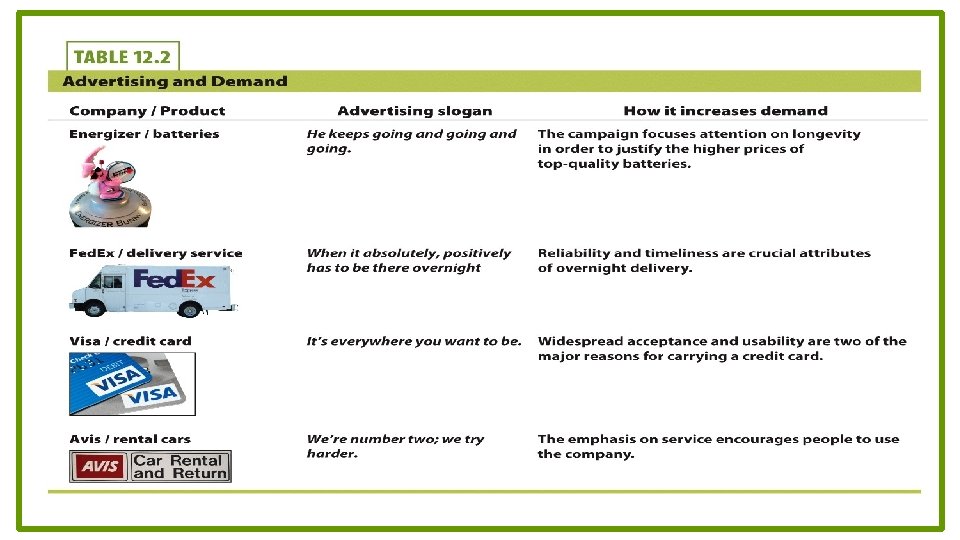

Advertising • Advertising – A method of nonprice competition – Represents 2% of U. S. annual economic output • Why advertise? – Provide information for consumers – Further differentiate the product – Increase demand for the product

Advertising and Demand Advertising is designed to decrease the price elasticity of demand (makes more inelastic) for the firm and shift firm's demand curve right.

Who Advertises? • Perfect competition – – Homogenous products means that advertising won't help an individual firm. Advertising is less effective in a perfectly competitive industry. A single firm that advertises would be at a cost disadvantage. However, the industry can still benefit from advertising. • Examples: – Beef – Milk – Orange juice

Who Advertises? • Monopolistic competition – Advertising is widespread and beneficial to individual firms with differentiated products. – Advertising can increase demand for single firm's product. • Examples: – Fast-food restaurants – Clothing stores

Who Advertises? • Monopoly – Not as necessary to advertise since the product has no close substitutes and consumer choice is limited – May advertise simply to inform consumer about the product and stimulate demand. • Example: – De Beers (diamond monopoly)

Negative Effects of Advertising • Advertising raises costs – One firm advertises, others follow suit. • When all firms advertise, the demand-increasing effects may cancel each other out. • No overall demand change, but higher costs still exist. • Price for consumers raise as well. • Business stealing externality: no individual firm can easily gain market share but feels compelled to advertise to protect its customer base. – Inspiring brand loyalty • Creates more inelastic demand, which raises prices

Advertising Increases Cost

Economics in Mad Men • "Mad Men" – “Smoke Gets in Your Eyes” – “Everybody else’s tobacco is poisonous. Lucky Strike’s is toasted. ”

Negative Effects of Advertising • Many advertisements are persuasive rather than informative – May cross the line from beneficial to manipulative – Creates an incentive to lie about a product • Advertising regulations – – FTC (Federal Trade Commission) regulates advertising. Goal: enforce truth-in-advertising laws Special attention paid to food, drugs, supplements, alcohol, and tobacco Internet has increased unsubstantiated claims.

Conclusion • Monopolistic competition – Exists when many competing firms produce differentiated products. – Has features of both perfect competition and monopoly. – Is closer to perfect competition than monopoly in terms of prices, output, and efficiency. – Is prevalent throughout our economy.

Summary • Monopolistic competition is a market characterized by free entry and many firms selling differentiated products. • Differentiation of products takes on three forms: – Style or type – Location – Quality

Summary • Monopolistic competitors, like monopolists, are price makers who have downward-sloping demand curves. – Whenever the demand curve is downward-sloping the firm is able to mark up the price above marginal cost. – This leads to excess capacity and an inefficient level of output. • Monopolistic competition is largely beneficial.

Summary • In the long-run, free entry and exit do not allow monopolistically competitive firms to make positive economic profits. • Advertising performs useful functions: – Information, location, new products, quality differences • However, advertising also increases costs. • Advertising can be misleading.

Practice What You Know Which of the following industries fits most closely with the model of monopolistic competition? A. B. C. D. Automobile production Farming Diamond mining Fast-food restaurants

Practice What You Know Which of the following is a monopolistic competitor? A. B. C. D. a local farm that grows Granny Smith apples a big and tall clothing store your local electric company General Motors

Practice What You Know Which of the following is true about monopolistic competition? A. B. C. D. It results in higher prices than monopoly. It results in higher prices than perfect competition. It results in lower quantity than monopoly. It is economically more efficient than perfect competition.

Practice What You Know What is a possible negative effect when many competitors all advertise? A. B. C. D. Demand increasing effects cancel out and costs are higher. Consumers want the products more. Products become too differentiated. Firms will begin to cooperate instead of compete.

Practice What You Know What is true about the long-run equilibrium for firms in a monopolistically competitive industry? A. B. C. D. MR < MC, P < min(ATC) P = MR = MC = min(ATC) P = ATC, P > MC, P > min(ATC) P > ATC, P = MC

Practice What You Know Which of the following is true about product differentiation? A. More differentiation means products are more substitutable for each other B. More differentiation leads to greater differences in price C. More differentiation leads to converging prices D. Differentiation lowers firm profits

Previously… • Monopolistic competition is a market structure characterized by free entry, many different firms, and differentiated products. • Differentiated products are substitutable, but not identical. • Firms advertise in order to increase demand for their product.

Oligopoly • Oligopoly is a market structure with the following characteristics: – Small number of firms – Differentiated products – Significant entry barriers – Firms interact strategically.

Comparing Market Structures

Measuring Concentrations of Industries • Concentration ratio – Used to measure oligopoly power in an industry – What percentage of industry sales are owned by the biggest firms? • Four-firm concentration ratio • Eight-firm concentration ratio – Is a rough gauge of oligopoly power—not an absolute measure due to international activity in the market. Consider the domestic car industry and international car industry.

Four-Firm Concentration Ratios in the United States

Duopoly • Duopoly – An oligopoly with only two firms – May happen in localized markets with cell phones or utilities • Duopoly behavior – Firms feel competitive pressure, but can enjoy advantages of market power. – Firms may have the incentive and the ability to cooperate, or collude.

Duopoly • Collusion – Agreement among rivals specifying prices or quantities – Firms ask: "What would a monopoly do? " and then do that action. • Cartel – Two or more firms acting in unison to form a joint monopoly.

Cartels • Cartels tend to be unstable over a long period of time. Why? – Each firm in the cartel often has an incentive to "cheat. " – Could occur by one firm lowering its price – Firm could also overproduce output (in situations with homogenous output, such as oil cartels).

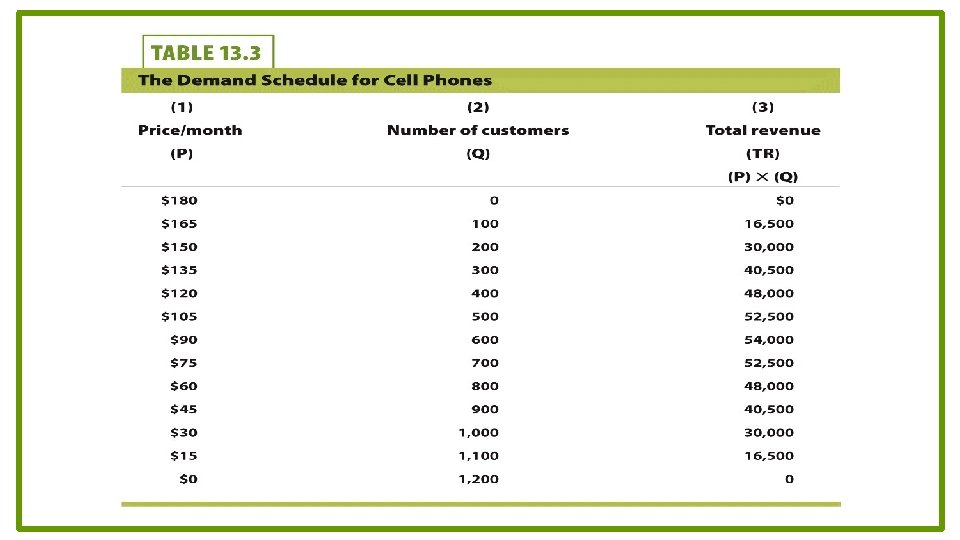

Cellphone Duopoly Market Perfect Competition vs. Monopoly Price/Month (P) Number of Customers (Q) Total Revenue (TR) TR = P × Q $180 165 150 135 120 105 90 75 60 45 30 15 0 0 100 200 300 400 500 600 700 800 900 1, 000 1, 100 1, 200 $0 16, 500 30, 000 40, 500 48, 000 52, 500 54, 000 52, 500 48, 000 40, 500 30, 000 16, 500 0 • Assume MC = 0 • Perfect Competition – – Result: P = MC P = $0 Q = 1, 200 Socially efficient • Monopoly – – No competition to drive price down P = $90 Q = 600 Loss of efficiency compared to competition

Cellphone Duopoly Market Duopoly Results with Collusion (Cartel) Price/Month (P) Number of Customers (Q) Total Revenue (TR) TR = P × Q $180 165 150 135 120 105 90 75 60 45 30 15 0 0 100 200 300 400 500 600 700 800 900 1, 000 1, 100 1, 200 $0 16, 500 30, 000 40, 500 48, 000 52, 500 54, 000 52, 500 48, 000 40, 500 30, 000 16, 500 0 • Duopoly – AT-Phone and Horizon • Collusion (Cartel) result: act like a joint monopoly by charging the monopoly price – – P = $90 Q = 600 (each firm produces 300) Profit of $27, 000 for each, assuming equal split Does each firm have an incentive to undercharge the competitor? What if that happens?

Cellphone Duopoly Results: Competing (or Cheating) Price/Month (P) Number of Customers (Q) Total Revenue (TR) TR = P × Q $180 165 150 135 120 105 90 75 60 45 30 15 0 0 100 200 300 400 500 600 700 800 900 1, 000 1, 100 1, 200 $0 16, 500 30, 000 40, 500 48, 000 52, 500 54, 000 52, 500 48, 000 40, 500 30, 000 16, 500 0 • Duopoly Competition – AT-Phone still believes Horizon will serve 300 customers. – AT-Phone lowers its price to P = $75. – Market demand is Q = 700. – AT-Phone profit: • 400 x $75 = $30, 000. • Horizon's reaction – Also wants 400 consumers – For both firms to do this, price must be P = $60 – Horizon and AT-Phone lower price to P = $60. • Profits now $24, 000 for each.

Cellphone Duopoly Price/Month (P) $180 165 150 135 120 105 90 75 60 45 30 15 0 Number of Customers (Q) Total Revenue (TR) TR = P × Q 0 100 200 300 400 500 600 700 800 900 1, 000 1, 100 1, 200 $0 16, 500 30, 000 40, 500 48, 000 52, 500 54, 000 52, 500 48, 000 40, 500 30, 000 16, 500 0 • Would a price war result in which the price falls to zero? – No, duopolist will try to gain more market shares and wait to see how competitor responds. – Each firm has what is called a response function. Each firm will respond to what the other firm does. – Duopoly outcome is more efficient than monopoly. – This outcome is called the second-best option or Nash Equilibrium (We will not cover Nash Equilibrium in this course, it is a topic part of game theory). – What is the first-best option?

Mutual Interdependence • Mutual interdependence – A market situation in which the actions of one firm have an impact on the price and output of its competitors. – AT-Phone's response depends on the actions of Horizon, and Horizon's response depends on the actions of AT-Phone. – Note the difference between interdependence and independence

Competition, Duopoly, and Monopoly Competitive Markets Duopoly Monopoly Price $0 $60 $90 Output 1200 800 600 Socially Efficient? Yes No No Explanation Each firm is mutually Since the marginal cost of interdependent and adopts a providing cellphone strategy based on the actions service is zero, the price is of its rival. This leads both eventually driven to zero. firms to charge $60 and service 400 customers. The monopolist is free to choose the profitmaximizing output. In this example it maximizes its total revenue.

Organization of Petroleum Exporting Countries

Cheating in a Cartel • OPEC (Organization of Petroleum Exporting Countries) cartel • 1988 Iraq – Virtually bankrupt – Economy was depended mostly on exporting oil. – Low oil prices hurting Iraq further – Iraq accused Kuwait of "cheating" and overproducing oil, which lowered the price. – What did Iraq do?

Cheating in a Cartel • Gulf War • Iraq invades Kuwait City

Oligopoly with More Than Two Firms • Imagine if a third firm entered the phone market and builds a cell tower: – So it is not duopoly anymore but Oligopoly. • Price effect – The total number of cellphone contracts sold (supply) increases, and the price firms are able to charge decreases. – The price effect by itself is a loss (selling units at lower prices). • Output effect – The new firm sells an additional unit (due to low price) in which it generates additional profits. – The output effect is a gain (selling more units increases revenue).

Oligopoly with More Than Two Firms • Price and output effects make maintaining a cartel (joint monopoly) difficult. – As firms enter, each individual firm will have a smaller impact on market price. – Firms will produce more as long as it is profitable. • Not all firms in oligopoly are the same size. – Each firm's actions affect price and output; and thus, affect decisions made by other firms (interdependence). – Small firms and large firms will behave differently, yet will act strategically.

Price Taking Price Making Perfect Competition 1. Many firms Monopolistic Competition 1. Many firms Oligopoly Monopoly 1. Few firms 1. One firm 2. Atomistic assumption—firms are so small 2. Each firm has some that no single buyer or seller has ANY control over price 2. Medium to high entry barriers to entry. The firm has more control over price. 2. Extremely high barriers to entry. The firm has significant control over price. 3. Firms are so small that no single buyer or seller has ANY control over price 3. Product differentiation 3. Mutual interdependence 3. The firm IS the industry 4 Homogeneous output 4. Free/Easy entry/exit 4. Long run economic profit possible 4. Long run economic profit probable 5. There is perfect information about product price and quantity 5. Output can be homogenous or differentiated 6. Free/Easy entry/exit

Conclusion • Oligopoly – – A market structure in which there a small number of firms Firms interact strategically. Can be competitive (results closer to monopolistic competition). Can be collusive (results closer to monopoly). • Antitrust policies – Restrain excessive market power. – Give incentives to compete instead of collude. – Each industry is examined on a case-by-case basis.

Summary • Oligopoly: a small number of firms sell a differentiated product in a market with significant barriers to entry. – An oligopolist is like a monopolistic competitor in that it sells differentiated products. – It is also like a monopolist in that it enjoys significant barriers to entry. • The small number of sellers in oligopoly leads to mutual interdependence. • Oligopolists have a tendency to collude and to form cartels in hope of achieving monopoly like profits. • Oligopolistic markets are socially inefficient since P > MC. • The result under oligopoly will fall somewhere between the competitive and monopoly outcomes.

Practice What You Know Which of the following is true about oligopoly? A. Oligopolies are illegal in the United States. B. All oligopoly industries will try to collude. C. Oligopoly industries generally have a high concentration ratio. D. Firms in an oligopoly act independently from other firms in the oligopoly.

Practice What You Know Why do cartel deals tend not to last? A. Each firm in the cartel has a dominant strategy to be uncooperative and defect from the cartel agreement. B. Cartel profits are lower than competitive profits. C. Cartels create more competition. D. Firms know that cartels are often illegal so they break the deal to escape.

Sources • "Principles of Economics with Smartwork Access (ISBN: 978 -0 -26314 -5), 1 st Edition, 2013" by Mateer and Coppock • "Economics: Custom Edition for NCSU (ISBN: 9781937435202" by David Hyman