US Economy Forecast 2011 2012 Till Schreiber College

US Economy Forecast 2011, 2012 Till Schreiber College of William & Mary August 4 th 2011 Nafa Annual Convention, Williamsburg, VA

Forecast for 2011, 2012 • What would we like to happen? – Deficit deal – Entitlement reform – Fewer but smarter regulations – Less uncertainty – …. • What’s actually going to happen? – Not all of that.

Realistic forecast must make assumptions about some of these factors • No ideological agenda • Based on current and historical data, facts (and some theory) • Where is the economy now? • What do some leading indicators suggest about the near future?

Snapshot of the economy • Unemployment rate 9. 2% – Little job creation – Government sector shedding jobs • GDP growth disappointing – Less than 2% in first quarter, likely not better than that for the second quarter • Economy slowed down by multiple “headwinds” – Oil (and other commodities) prices – Supply chain disruptions because of Japan – Depressed housing market • Inflation expected to be about 2% each year going forward

Government spending cuts • Absolutely necessary over the long term – Unless you are ok with living in a country like France; most Americans don’t seem to be • Big cuts right NOW will slow the economy down for the rest of the year – Higher unemployment – Reduction in growth – All bets are off, if debt ceiling is not increased. This would lead to a massive reduction of spending right NOW • Assume: Assume Some further cuts this year, no “stimulus” from government sector

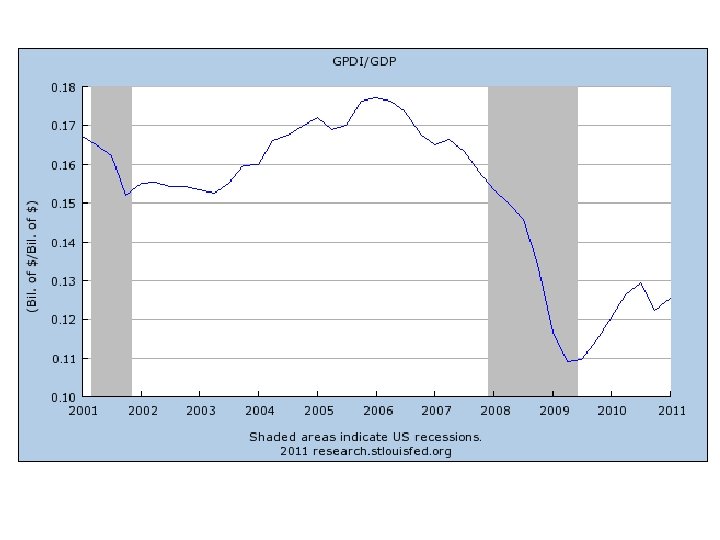

Investment, Investment • Main issue of disappointing “recovery” – Private sector investment fell of a cliff in late 2008, early 2009 – Has not recovered since to anywhere near normal levels

– According")

Housing Market • Residential fixed investment (People building houses, or major remodel/improvements) – According to latest numbers still only 42% of 2005 level. For every $100 spend on housing construction in 2005, now only $42 are spent. – Building permits, housing starts, existing home sales, foreclosures all do not suggest major boom ahead anytime soon. • Assume: Assume Housing market continues to be depressed, at least no major improvement in sight

Business Sector • You guys! • High levels of uncertainty – Regulations and Taxes – Consumer and Industry demand going forward • Consumer Confidence Measures still very low – Down compared to last year • Purchasing Managers’ Index (ISM) – Lower compared to April, how temporary are the “headwinds”?

Hiring

What does this picture mean? • Even where there are job openings many businesses take it relatively slow to fill them • Assume: Assume No jobs miracle likely to be coming soon from the private sector under current conditions

show loan")

Financial Markets • Reports on Banking and Finance activity nationwide (Beige Book) show loan demand as “mixed” or “slightly improved” • Senior Loan Officer Opinion Survey shows some (minor) improvements in availability of credit to businesses nationwide – Banks state they are mostly held back by an increased uncertainty of the economic outlook and a reduced tolerance for risk

Exports • Still strong growth in China, India, Brazil – Even larger growth for products pitched at new middle class – Chinese apartments with two air conditioners – Currency manipulation will continue • Eurozone faces internal issues, so does Japan • No export boom likely overall

What to make of all this? • Growth in the second half of 2011 will likely be at most around 3%, maybe lower. – Not enough to make major progress in terms of reducing unemployment; no surprise if rate remains around 9% over the rest of the year – Combined with growth of less than 2% in the first half, overall growth for the year of 2011 will be below 3%

Forecast for 2012 • Growth should pick up once the recovery really takes hold – Has been predicted since late 2009 • Crucial market: Housing! • No government policies in sight to address housing market boldly – Muddling through • Economist: Housing market now potentially undervalued in US (based on rent to price ratios), does not mean has reached bottom

Forecast for 2012 • Households and many businesses are still paying down debt from the bubble years – Will continue in 2012 – Debt levels have come down but not nearly to prebubble levels • “Disappointing” recovery may continue • Growth of 3 -3. 5% unlikely to be topped next year • Unemployment comes down very, very slowly

Forecast for 2012 • Assumes no major new “headwinds” • Also no miracles • Assumes no major policy changes – Safe assumption for Congress – Also unlikely that the Federal Reserve will be willing to do something dramatic • Forecast consistent with forecast from Federal Reserve, economists at Goldman Sachs etc. – Sorry, I am not more cheerful but I have good company…

- Slides: 17