US BROKERAGES Amrit Gill Ning Liu Sizu Warren

Jiang")

US BROKERAGES Amrit Gill Ning Liu Sizu (Warren) Jiang

Table of Contents 1. Industry 2. Morgan Stanley Overview 3. Risk Management 4. Employee Compensation

What Do They Do? v Capital Raising v Wealth Management v Equity and debt underwriting v Merger and acquisitions Advisory v Fixed Income Securities v Investment advisory and financial planning services v Market making activities

Market Value

Industry Growth Rate

MARKET SEGMENTATION I

MARKET SEGMENTATION II

MARKET SHARE

COMPETITIVE LANDSCAPE v M&A n n n Morgan Stanley acquired Goldfish in Feb. 2006 HSBC acquired the credit card issuer Metris in Aug. 2005 M&A between JP Morgan Chase & Co and Bank One v Outsourcing n n Lower operational costs India v The Asia-Pacific region n Growing market Political and regulation barriers China, India, Russia and Middle East

GLOBAL LEADING COMPANIES v JP Morgan v Morgan Stanley v UBS AG v Goldman Sachs Group

Bulge Bracket v Goldman Sachs v Morgan Stanley v Merrill Lynch v J. P. Morgan & Co. v Lehman Brothers

MARKET FORECASTS

GENERAL RISKS v Liquidity Risk n n n Inability to trade or transfer funds Inability to sell and collect the proceeds for a specific asset Inability to meet financial obligations v Market Risk n Adverse movements in the level or volatility of market prices of interest rate instruments, equities, commodities and currencies. v Credit Risk n The risk that there may be default on payment of interest or capital by a borrower

GENERAL RISKS v Operational Risk n The risk of loss due to system breakdowns, employee fraud or misconduct, errors in models or natural or man-made catastrophes, among other risks. It may also include the risk of loss due to the incomplete or incorrect documentation of trades. Operational risk may be defined by what it does not include: market risk, credit risk, and liquidity risk. v Legal Risk n n Non-compliance with applicable legal and regulatory requirements and standards. Contractual and commercial risk such as the risk that a counterparty's performance obligation will be unenforceable

Stock Today

1 Year Daily

Business Segments Institutional Securities Global Wealth Management Group Asset Management Discover

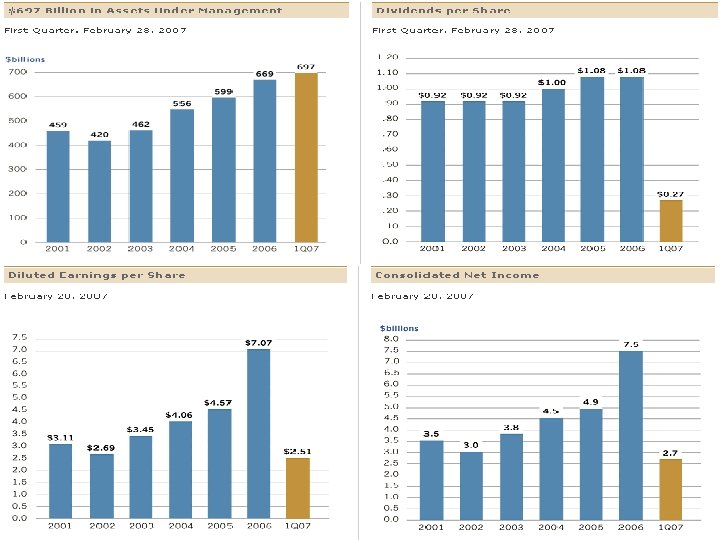

Overview

Business Segments

Over 600 Offices in 31 Countries

History • 1854 – American Junius S. Morgan joined a London banking business and his son J. Piermont Morgan became the financial titan of his day, acting as the US unofficial central banker • Helped form GE and US Steel • He was succeeded by his son J. P. Morgan Jr. • 1933 – The Glass Steagall Banking Act forced firms to choose between commercial banking and investment banking • Henry S. Morgan and Harold Stanley left J. P. Morgan & Co to form Morgan Stanley & Co • 1935 – Sept 16, Firm opened its doors on 2 Wall Street

Achievements

Expansion

Innovation

Community

Risk Management Philosophy “Risk is an inherent part of the Company’s business and activities. The Company’s ability to properly and effectively identify, assess, monitor and manage each of the various types of risk involved in its activities is critical to its soundness and profitability. The Company’s broad-based portfolio of business activities helps reduce the impact that volatility in any particular area or related areas may have on its net revenues as a whole. The Company seeks to identify, assess, monitor and manage, in accordance with defined policies and procedures, the following principal risks involved in the Company’s business activities: market, credit, operational, legal, and liquidity and funding risk. ”

INTEGRITY HOTLINE!!!!!! The cornerstone of the philosophy is the protection of the Company’s franchise, reputation and financial standing.

Risk Governance Structure Audit Committee Internal Audit Committee Firm Risk Committee Company Control Groups Institutional Securities Global Wealth Management Group Asset Management Discover Firm Risk Committee Segment Control Groups

Risk Factors v Liquidity Risk v Market Risk v Credit Risk v Operational Risk v Legal Risk v Competitive Environment v International Risk v Acquisition Risk v Credit Card Risk v Risk Management

Liquidity and Funding Risk Liquidity and funding risk refers to the risk that Morgan Stanley will be unable to finance its operations due to a loss of access to the capital markets or difficulty in liquidating its assets.

Liquidity and Funding Risk v Liquidity is essential to the business and they rely on external sources to finance a significant portion of operations n n Liquidity could be substantially negatively affected by the inability to raise funding in the long-term or shortterm debt capital markets or access secured lending market Caused by: n Disruption of the financial markets n Negative perception of the financial industries n Negative perception of Morgan Stanley n Trading losses, downgraded or negative watch, decline in level of business activity, regulatory actions, employee misconduct or illegal activity

Liquidity and Funding Risk v Borrowing costs and access to debt capital markets depend significantly on credit ratings n Factors significant to determine credit ratings n Level and volatility of earnings n Relative competitive position n Geographic and product diversification n Ability to retain key personnel n Risk profile n Risk management policies n Cash liquidity n Capital adequacy n Corporate lending credit risk n Legal and regulatory developments

Liquidity and Funding Risk v A holding company and depend on payments from subsidiaries n Regulatory and other legal restrictions may limit ability to transfer funds freely, either to or from subsidiaries. v If liquidity and funding policies are not adequate, may be unable to access sufficient financing

Liquidity and Capital Resources v Senior management establishes the overall liquidity and capital policies n n Review business performance relative to these policies Monitor the availability of alternative sources of financing Oversee the liquidity and interest rate and currency sensitivity of the Company’s asset and liability position Evaluate, monitor and control the impact the company’s business activities have on its consolidated balance sheet, liquidity and capital structure

Liquidity and Funding Risk Management Framework The key objectives of the liquidity and funding risk management framework are to support the successful execution of the Company’s business strategies while ensuring the ongoing and sufficient liquidity through the business cycle and during periods of financial distress.

Basel II Capital Accord v Introduces the concept of economic capital into the regulatory capital consideration by requiring banks to determine capital adequacy based on the level of risk posed by specific business activities v Overcomes shortcoming of Basel I, which did not require banks to develop their own methods, processes, systems to measure the capital level adequate for the risks they assume.

Regulatory Capital vs. Economic Capital

Economic Capital v Uses an economic capital model to determine the amount of equity needed to support the risk of its business activities and to ensure that the Company remains adequately capitalized. v Calculated on a “going-concern basis” n Amount of capital needed to run the business through the business cycle and satisfy the requirements of regulators, rating agencies, and the market v Business unit economic capital allocations are evaluated by benchmarking to similarly rated peer firms by business segment

Economic Capital v Assigns common equity to each business unit based on regulatory capital usage plus additional capital for stress losses, including principal investment risk n n Stress losses are defined at the 90% to 95% confidence interval in order to capture the worst potential losses in 10 to 20 years Types of stress losses: n Market: systematic, idiosyncratic (unsystematic) or random risk n Credit: counterparty defaults n Business: earnings volatility n Operational: legal risk

Linking Risk to Capital

Risk Components of Economic Capital

Economic Capital

Economic Capital Beginning in the first quarter of fiscal 2007, economic capital will be met by regulatory Tier 1 equity (including common shareholders’ equity, certain preferred stock, eligible hybrid capital instruments and deductions of goodwill and certain intangible assets and deferred tax assets), subject to regulatory limits.

Liquidity Management Framework Contingency Funding Plan Cash Capital Liquidity Reserve

Contingency Funding Plan v Ascertain the Company’s ability to manage a prolonged liquidity contraction and provide a course of action over a one-year time period v Incorporates a wide range of potential cash outflows during a liquidity stress event v Sets forth the process and the internal and external communication flows necessary to ensure effective management of the contingency event

Types of Potential Cash Outflows v Repayment of all unsecured debt maturing within one year v Maturity roll-off of outstanding letters of credit with no further issuance and replacement with cash collateral v Return of unsecured securities borrowed any cash raised against these securities v Additional collateral required in the event of ratings downgrade v Higher haircuts on or lower availability of secured funding v Client cash withdrawals v Drawdowns on unfunded commitments provided to third parties v Discretionary unsecured debt buybacks

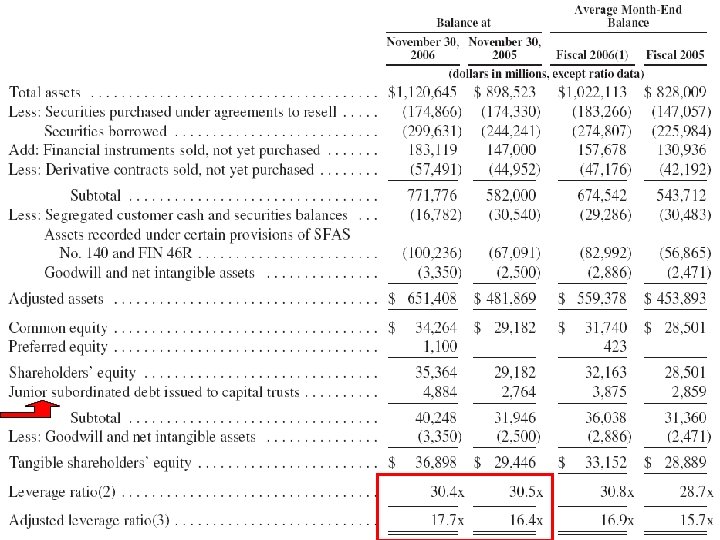

Cash Capital v Ensure that the Company can fund its balance sheet while repaying its financial obligations maturing within one year without issuing new unsecured debt. v Achieved by maintaining sufficient cash capital (long-term debt and equity capital) to finance illiquid assets and the portion of its securities inventory that is not expected to be financed on a secured basis in a credit-stressed environment. v Seeks to maintain a surplus cash position n Nov 30, 2006: $162, 134 million

Liquidity Reserve v Maintain, at all times, a liquidity reserve composed of immediately available cash and cash equivalents and a pool of unencumbered securities that can be sold or pledged to provide same-day liquidity to the Company v Determined by day-to-day funding requirements and strategic liquidity targets v In 2006, averaged approximately $44 billion.

Additional Sources v Committed Credit Facilities n n Senior revolving credit agreement with a group of banks to support general liquidity needs n Issuance of commercial paper etc. Secondary component Diversification of lenders covering geographic regions (North America, Europe, Asia) As of Nov 30, 2006 no borrowings were outstanding with the Credit Facility

Funding Management Policies v Designed to provide for financings that are executed in a manner that reduces the risk of disruption to the Company’s operations that would result from an interruption in the availability of funding sources. v Pursues a strategy of diversification of funding sources (by product, by investor, and by region) v Attempt to ensure that the term of the Company’s liabilities equals or exceeds the expected holding period of the assets being financed (refinancing risk)

Funding Management Policies v Funds its balance sheet through diverse sources: n n n n Company’s equity capital Long term debt Repurchase agreements US, Canadian, Euro, Japanese and Australian commercial paper Asset-backed securitizations Letters of credit Unsecured bond borrowings Securities lending Buy/Sell agreements Municipal reinvestments Promissory notes Master notes Committed and uncommitted lines of credit

Credit Ratings v In connection with certain OTC trading agreements and certain other agreements associated with the Institutional Securities business, the Company would be required to provide additional collateral to certain counterparties in the event of a downgrade by either Moody’s Investors Service or Standard & Poor’s n Nov 30, 2006: $1, 184 million (one notch downgrade)

Credit Ratings

Market Risk Interest Rate Risk Currency Risk Equity Price Risk Commodity Price Risk

Risk Mitigation Strategies v Diversification n Manages the market risk associated with its trading activities on a Company-wide basis, on a worldwide trading division level and on an individual product basis v Hedging n Consist of the purchase or sale of positions in related securities and financial instruments, including a variety of derivative products (e. g. , futures, forwards, swaps and options)

Measurement of Market Risk in Trading Activity v Va. R versus Volatility v New science of risk management v What is the worst case scenario? v Three components of Va. R: n n n A time period A confidence level A loss amount

Application of Va. R in MS v Historical method: re-organizes actual historical returns, putting them in order from worst to best. It then assumes that history will repeat itself, from a risk perspective. v Four years of historical data v Use Monte Carlo simulation as a supplement to capture name-specific risk in equities and credit products

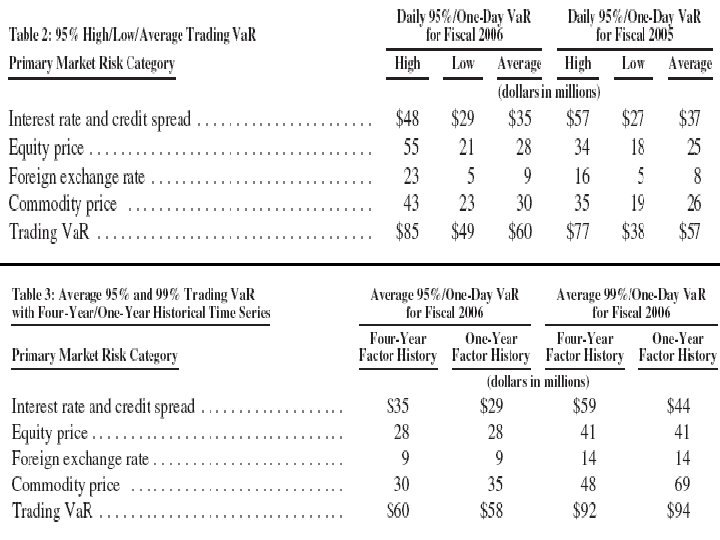

The increase in Aggregate Va. R and Trading Va. R at year-end was driven primarily by increased directional exposure to equity products.

Evaluation of Va. R v Compare the Va. R with actual trading revenue. v Assuming no intra-day trading, for a 95%/one-day Va. R, the expected number of times that trading losses should exceed Va. R during the fiscal year is 13, and, in general, if trading losses were to exceed Va. R more than 21 times in a year, the accuracy of the Va. R model could be questioned.

There is a net trading loss of $87 million on only one business day during fiscal 2006, which exceeded the 95%/one-day Va. R for that day

Advantages of Va. R v Takes into account linear and non-linear exposures to price risk and interest rate risk, and linear exposures to implied volatility risks. v Market risks that are incorporated in the Va. R model include equity and commodity prices, interest rates, foreign exchange rates and associated implied volatilities. v Able to evolve over time in response to changes in the composition of trading portfolios

Disadvantages of Va. R v Past changes in market risk factors may not always yield accurate predictions of the distributions and correlations of future market movements v Changes in portfolio value in response to market movements (especially for complex derivative portfolios) may differ from the responses calculated by a Va. R model v Va. R using a one-day time horizon does not fully capture the market risk of positions that cannot be liquidated or hedged within one day

Measurement of Market Risk in Consumer lending Activity v Interest rate sensitivity analysis n For purposes of presenting the possible earnings effect of a adverse change in interest rates over the 12 -month period from its fiscal year-end, they assume that all interest rate sensitive assets and liabilities will be impacted by a hypothetical, immediate 100 basis-point increase in interest rates as of the beginning of the period

Results of Sensitivity Analysis v The pre-tax income of consumer lending and related activities over the following 12 -month period would be reduced by approximately $125 million. v In 2005, the estimation is only $36 million v The increase in the reduction in pre-tax income at November 30, 2006 was due to a higher level of variable rate funding.

Assumptions and Limitations of Sensitivity Analysis v The balances of interest rate sensitive assets and liabilities will remain constant over the next 12 -month period v No growth, no change in business focus and no change in asset pricing philosophy v So, the model cannot adequately portray how MS would respond to significant changes in market conditions. Furthermore, the analysis does not necessarily reflect the MS’s expectation about the change of interest rates in the near future

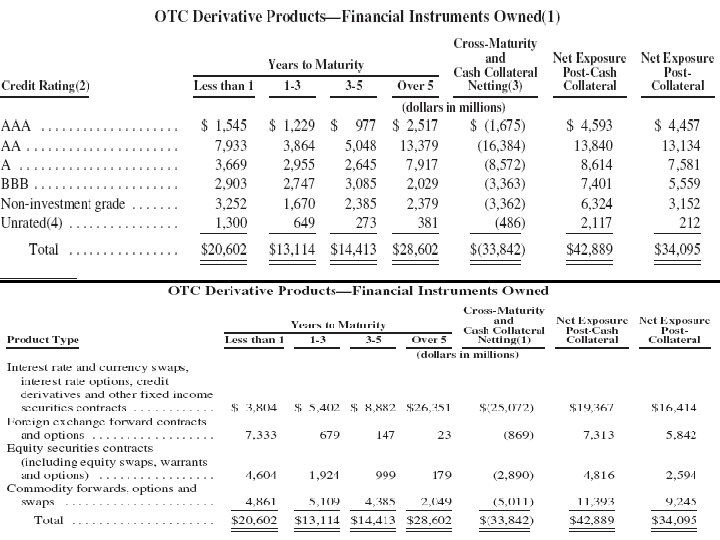

Credit Risk v The risk of loss arising from borrower or counterparty default when a borrower, counterparty or obligor is unable to meet its financial obligations. v 3 Types: n n n Single name risk Individual customer risk Customer portfolio risk

v MS has its own credit rating system for the counterparties v Hedges its risk through selling the loans in the primary and secondary loan market and sign the master netting agreements and collateral agreements with the counterparties

Individual Customer Risk v Margin Lending n n n Collateralized in accordance with internal and regulatory guidelines. monitors required margin levels established credit limits daily v Commercial Lending n n Clients are required to submit a comprehensive credit application, including financial statements Comprehensive analysis is performed to assess the business model and to determine appropriate structure, guarantors’ strengths, debt and cash flow capacity, liquidity and collateral coverage

Customer Portfolio Risk v Credit review for Credit Card application based on the information obtained from applicants and credit bureaus. v Each card member's credit line is reviewed at least annually, and actions resulting from such review may include raising or lowering a card member's credit line or closing the account

Employee Compensation Plans v SFAS No. 123 R v Measurement of compensation cost for equity-based awards at fair value and recognition of compensation cost over the service period, net of estimated forfeitures.

Employee Stock Options v Total intrinsic value of stock options exercised during fiscal 2006: $326 million v As of Nov 30, 2006, the intrinsic value of in-the -money exercisable stock options was $2, 292 Million

Executives Compensation Philosophy v Performance-based n n Pay levels should be determined based on Company, business unit and individual results compare to quantitative and qualities performance priorities set at the beginning of the year Profit before taxes and ROE v Shareholder-aligned n Equity should be awarded as a significant component of incentive compensation v Competitive and fair relative to industry standards n Pay levels should be perceived both internally and externally as competitive and fair relative to industry standards

Executives Compensation

GENERAL RISKS v Operational Risk n The risk of loss due to system breakdowns, employee fraud or misconduct, errors in models or natural or man-made catastrophes, among other risks. It may also include the risk of loss due to the incomplete or incorrect documentation of trades. Operational risk may be defined by what it does not include: market risk, credit risk, and liquidity risk. v Legal Risk n n Non-compliance with applicable legal and regulatory requirements and standards. Contractual and commercial risk such as the risk that a counterparty's performance obligation will be unenforceable

Employee Compensation Plans v SFAS No. 123 R v Measurement of compensation cost for equity-based awards at fair value and recognition of compensation cost over the service period, net of estimated forfeitures. v The fair value of stock options is determined using the Black-Scholes valuation model.

Deferred Stock Awards v The plans provide for the deferral of a portion of certain key employees’ discretionary compensation with awards made in the form of restricted common stock or in the right to receive unrestricted shares of common stock in the future v The weighted average price of restricted stock units at the beginning and end of fiscal 2006 was $51. 47 and $53. 57, respectively. v The total fair value of restricted stock units converted to common stock during fiscal 2006, fiscal 2005 and fiscal 2004 was $768 million, $986 million and $791 million, respectively.

Deferred Stock Awards v Unvested restricted stock units represent awards where recipients have yet to satisfy either the explicit vesting terms or retirement eligible requirements.

Stock Option Awards v key employees’ discretionary compensation with awards made in the form of stock options v generally having an exercise price not less than the fair value of the Company’s common stock on the date of grant v generally become exercisable over a one- to five-year period and expire 10 years from the date of grant, subject to accelerated expiration upon termination of employment.

Stock Option Awards v Total intrinsic value of stock options exercised during fiscal 2006: $326 million v As of Nov 30, 2006, the intrinsic value of in-themoney exercisable stock options was $2, 292 Million

Executives Compensation Philosophy v Performance-based n n Pay levels should be determined based on Company, business unit and individual results compare to quantitative and qualities performance priorities set at the beginning of the year Profit before taxes and ROE v Shareholder-aligned n Equity should be awarded as a significant component of incentive compensation v Competitive and fair relative to industry standards n Pay levels should be perceived both internally and externally as competitive and fair relative to industry standards

Executives Compensation

- Slides: 89