UNIT V INVENTORY CONTROL MEANING Inventory control is

• VED (Vital, Essential,")

ØEssential (E) ØDesirable")

• M")

")

• D-Difficult material")

Intuitive method • This is the want book method’. Here the items are recorded")

Perpetual inventory method • Keeping book inventory continuously in agreement with stockon hand within")

• Stores ledger (quantitative cum valued Perpetual")

• This is containing only quantity details of stock.")

• In the Store Ledger the")

• Record the result of stock verification in a")

Two bin method • Stock of each item is held in two bins. •")

- Slides: 56

UNIT V: INVENTORY CONTROL

MEANING • Inventory control is a method of stocking adequate number and kind of stores so that materials are available whenever required. • This has to be done at an outlay of financial and human resources.

Objectives of inventory control Main objective is to minimize the total cost of inventory. • • Protection against fluctuations in demand Better use of men, machines and material Protection against fluctuations in output Control of stock volume and stock distribution

• To carry adequate stock to avoid stockouts • To order sufficient quantity per order to reduce order cost • To stock just sufficient quantity to minimize inventory carrying cost

• To provide safety stock to take care of fluctuation in demand/ consumption • To ensure optimum level of inventory holding to minimize the total inventory cost.

Methods of Inventory Control • ABC analysis (Always Better Control) • VED (Vital, Essential, Desirable) • FSN (Fast moving, Slow moving, Not moving) • HML (High, Medium, Low) • SDE (Scarce, Difficult, Easy)

• A items- Represents high cost centre • B items- Intermediate cost centre • C items- Low cost centre.

CLASSIFICATION % OF ITEMS % OF VALUE A 10 70 B 20 20 C 70 10

ABC METHOD OF INVENTORY CONTROL A ITEMS: Tight controls Rigid estimates strict and close watch Safety stocks should be low Handled by top management level

B ITEMS Moderate controls Purchase based on rigid requirements Reasonably strict watch and control Safety stocks moderate Handled by middle management level

C ITEMS Ordinary control measures Purchase based on usage estimates Controls exercises by storekeeper Safety stocks high Handled by lower management level

Advantages • Provides a mechanism for identifying items that will have a significant impact on overall inventory cost • It helps to segregate those items which ought to be given priority to maximize results. • Proper use of valuable time of store personnel.

LIMITATION • When number of items runs into several thousands, it is not convenient to compute and carry out this analysis. • More chances of deterioration in storage exist. • Loose control on C may result in shortages.

• ABC focuses on money value and not on functional importance of such items, resulting in shortages of critical items. • ABC ignores market conditions, market availability, competitions, seasonal variations etc.

Ved analysis • classified as per the functional importance ØVital (V) ØEssential (E) ØDesirable (D)

VED METHOD OF CONTROL • Vital: § Items without which treatment comes to standstill: § Non-availability cannot be tolerated. (shortage) § The vital items are stocked in abundance, essential items and very strict control.

Essential: �Items whose non availability can be tolerated for 2 -3 days. �Essential items are stocked in medium amounts �Purchase is based on rigid requirements and reasonably strict watch. �Shortage can be tolerated for a short period.

Desirable: �Items whose non availability can be tolerated for a long period. Desirable items are stocked in small amounts and purchase is based on usage estimate. �Shortage will not adversely affect, but may be using more resources. These must be strictly Scrutinized

• Although the proportion of vital, essential and desirable items varies from hospital to hospital depending on the type and quantity of workload, on an average • Vital items are 10%, • Essential items are 40% • Desirable items make 50% of total items available.

FSN • Fast • Slow • Nonmoving

• Fast moving consumed in a short span of time �Slow moving -which are not issued at frequent intervals & are expected to be exhausted over a period. • Non moving which are exhausted over a period of a year or so.

• H - Unit value > 1000 (Sanctioned by higher officials) • M - Unit value 100 to 1000 • L - Unit value < 100

SDE (Scarce, Difficult, Easy)

• S-Scarce Material i. e. hardly available (government approvals ) • D-Difficult material i. e. difficult in sourcing • E-Easy materials i. e. materials available easily

Other Inventory Control Methods • Intuitive method • Perpetual inventory method • Two bin method • Periodic/ cyclic system

1)Intuitive method • This is the want book method’. Here the items are recorded in the want book when the number of units in stock reaches close to zero.

2)Perpetual inventory method • Keeping book inventory continuously in agreement with stockon hand within specified time periods.

Components • Bin cards (quantitative Perpetual inventory) • Stores ledger (quantitative cum valued Perpetual inventory) • Continuous stock taking (physical Perpetual inventory) or Continuous physical stock verification

Bin cards (quantitative Perpetual inventory) • This is containing only quantity details of stock. • suitable entry of the quantity is made in the ‘receipts ’column • ‘issue’ column. • ‘balance’ column with the date.

Stores ledger (quantitative cum valued Perpetual inventory) • In the Store Ledger the quantities and values both are entered in the receipt, issue, and balance columns. • The sheets are numbered serially and initialed by a responsible official so as to avoid the risk of removal or loss

Inventory tags It should be hanged along the sides of material or medicine boxes. Whenever verification is made, an entry should be made with remarks in it.

Bin cards

Stock verification sheets (Inventory records) • Record the result of stock verification in a separate record or sheet and should be arranged in date-wise order.

Adv. ANTAGES OF PERPETUAL INVENTORY SYSTEM • On the stores, a complete & reliable check is obtained. • For the purpose of stock taking, the normal working of the company is not needed to be kept suspended. • Detection & adjustment of discrepancies can be readily made. Where ever possible, measures to avoid such discrepancies should be taken

• Assurance is given of timely stock replenishment because store audit also looks into the fact whether as soon as the stock reached the ordering level, initiative for purchase was taken or not. • Upon the stores personnel, it creates a moral check. • Reliable stock figures can be obtained for fire insurance etc.

• Detection of obsolete & slow moving materials can be achieved by systematic review of perpetual inventory.

DISADVANTAGES • It is costly. • The work shall be hampered unless the bin cards & stores ledgers are kept up to date. • The bin card balance & the stores ledge balance must be reconciled first if the two balances does not agree & then only physical verification of stock shall be feasible. This will require time.

3)Two bin method • Stock of each item is held in two bins. • When the first bin is empty, the order for replenishment is placed and the stock in the second bin is utilized till the ordered material is received.

Periodic/ cyclic system Periodic stock verification • Under this system, the entire stock is verified all at a time, at periodic intervals , at the end of each accounting period (e. g. , monthly, quarterly) • The ordering interval is thus fixed but the quantity to be ordered varies each time.

Storage Conditions • Drugs like sera, vaccines and regular products need to be stored at temperature range of 210 degree Celsius. • A large variety of drugs need to be stored at temperature of 15 -20 degree Celsius. • Cool and cold rooms should be available in all medical stores and strict monitoring of temperature done by the store keeper and supervisors.

Relationship between assets and expenses • Materials and supplies continue to have a market value until it is consumed in the daily operations of the hospital and if not used, it could be sold and turned into money again. There should be a proper recording of consumed and unconsumed materials at the end of every year.

Maintaining balance between costs and risks • Ordering costs • Carrying cost

Inventory ordering costs • The costs of placing an order and receiving the merchandise or the costs incurred to get the materials. • These costs comprise of salaries and wages of involved personnel, postal, fax or telephone bills, advertisements, stationaries, entertaining the vendors/suppliers and travel of stores personnel.

Inventory ordering costs Ordering cost = S/Q x P, where S = total usage Q = quantity per order P = cost of placing an order

Inventory carrying costs • Carrying cost is the cost associated with keeping/maintaining the materials in the stores. • This includes warehousing costs, financial costs and inventory costs related to perishability, shrinkage and insurance.

Inventory carrying costs Carrying cost = Q/2 x C , where Q/2 represents average quantity C is the carrying cost per unit.

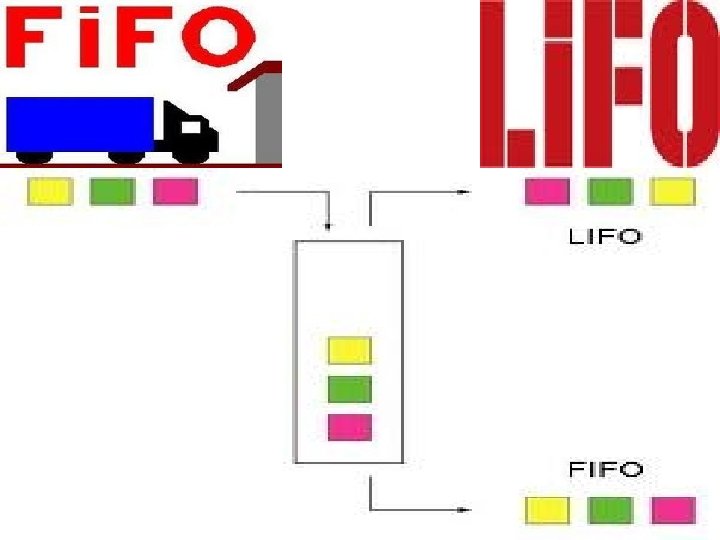

Methods of valuation of inventory • • First in first out method Last in first out method Average unit price method Fixed last price method

FIFO AND LIFO • FIFO-Assumes that goods are used in the order in which they are purchased. • LIFO- The oldest stock will be issued first

average cost method • Under the average cost method, it is assumed that the cost of inventory is based on the average cost of the goods available for sale during the period. • The average cost is computed by dividing the total cost of goods available for sale by the total units available for sale.

Fixed last price method • In this method, the issues and the inventory at stock-taking time are priced at the price of the last receipt of the item.

Nurses Role :

Nurses Role • Recognizing and decreasing supplies, procedures for obtaining equipment and supplies should be carefully examined. • Remove the expensive equipments not used for emergencies and encourage the nurse to make effective choices.

• Encourage nurses and other clinical staffs to obtain necessary supplies from CSSD rather than borrowing from near by units. • There should be proper specification of quantity , payment terms, delivery period, and guarantee of each item.

Nurse manager should see that : • Inventory are of latest technology , upgradability and from reputed manufacturer. • Availability of maintenance and repair facility. • Materials must be stored in an appropriate place in a correct way. • Group wise and alphabetical arrangement helps in identification and retrieval.

• First-in, first-out principle to be followed. • Monitor expiry date. • Follow two bin or double shelf system, to avoid stock outs. • Reserve bin should contain stock that will cover lead time and a small safety stock.