Unit 5 Credit What Is Consumer Credit Consumer

• The Fair and Accurate Credit Transaction")

• Ensures consumers are fully informed about the cost")

• Protects the privacy and accuracy of information in")

• Prohibits discrimination in giving credit on the basis of")

• Established a procedure for the quick correction of")

• Prevents abuse by professional debt collectors, and")

")

- Slides: 81

Unit 5 Credit

What Is Consumer Credit? • “Consumer” credit is generally defined as credit granted to a consumer, permitting the use or ownership of goods or services during a term of payment. In other words, credit allows you to take delivery of something and use it “while” you are paying for it. • Over the years, a wide variety of methods such as installment loan plans and credit cards have evolved to make the process of securing and using goods and services before we fully pay for them easier and more convenient.

Types of Credit • Credit generally takes three general forms; non-installment credit, regular installment credit and revolving credit.

Non-installment Credit • Non-installment credit refers to regular credit accounts requiring that the balance be paid off within 30 days. Travel and entertainment cards often fall into this category. Users can avoid interest charges if they are able to pay the balance in a single payment.

Regular Installment Credit • Manufacturers sometimes make installment credit available to allow consumers to purchase things like cars, furniture and major appliances. Interest is added to the purchase amount and the buyer agrees to pay the total amount in two or more regularly scheduled payments.

Revolving Credit • This category represents a large percentage of consumer credit cards and allows many items to be bought using the plan as long as the total amount does not go over the credit user’s assigned dollar limit. Interest is charged on the unpaid balance.

Why Organizations Issue Credit • “Before the introduction of credit cards people who were short of funds could borrow a “few bucks” from family and friends. Depending on where they lived and their relationship with the bankers and retailers in their community, they might also ask the bank or the local grocer to extend credit “until things get better”. Credit cards streamlined that process, making it more convenient and, at the same time, less personal. Banks and other organizations typically issue credit for two important reasons: • To offer a service to their customers. • To Make Money

Next 8 Slides • Advantage or Limitation? • Limitation is a disadvantage Answer on the ipad If squad talks to squad 10 pt penalty Close Ipad when finished

Buy needed/wanted services using anticipated future income • Advantage. Credit allows you to enjoy something now and pay for it later.

If the balance is not paid in full, interest adds to the overall cost • Limitation. The additional cost of the interest on credit card purchases is a limitation that many consumers fail to consider.

Convenience. Do not have to carry cash. • Advantage. The flexibility and convenience of readily available funds for purchases is a definite advantage of credit.

Provides a record of purchases • Advantage. It is much easier to track credit purchases because a record of your spending and purchases is automatically generated.

Impulse spending may be too tempting for some • Limitation. Because you have the flexibility to enjoy purchases now and delay payment, it is easier to overspend. This is a definite limitation of credit purchases.

Flexibility to buy needed items now • Advantage. Because you can purchase essential items even if the funds are not available, credit can be indispensable in emergency situations.

Consolidates bills into one payment • Advantage. The ability to consolidate payments and manage cash flow effectively is a major advantage of credit.

Other fees--membership, late payment--add to the overall cost • Limitation. The miscellaneous fees associated with credit can have a real impact on the purchase price of an item and can be a limitation of credit purchases. .

What is Credit Worthiness? • Just like the local bank or retailer who may have extended credit to your grandfather, banks and other creditors base their decision to extend credit on an individual’s credit worthiness. Organizations consider three factors when assessing a consumer’s overall credit worthiness. • Character • Capital • Capacity

What is Meant by Character? • From your credit history, the lender attempts to determine if you possess the honesty and reliability to repay the debt. They ask the following questions in their evaluation: • Have you used credit before? • Do you pay your bills on time? • Do you have a good credit report? • Can you provide character references? • How long have you lived at your present address? • How long have you been at your present job?

Capital • Lenders also want to know if you have any valuable assets such as real estate or personal property like an automobile or savings or investment account. Owning assets like these is important because they could be used to repay credit debts if income is unavailable. Common questions lenders ask to assess the capital available include: • What property do you own that can secure the loan? • Do you have a savings account? • Do you have investments to use as collateral?

Capacity - Can You Repay Your Debt? • The final “C” evaluated by lenders is your “capacity” to repay your debt. The lender will look to see if you have been working regularly in an occupation that is likely to provide enough income to support your credit use. Potential lenders ask a variety of questions to determine your capacity to repay. • Some questions a lender might ask: • Do you have a steady job? • What is your salary? • How many other loan payments do you have? • What are your living expenses? • What are current debts? • How many dependents do you have? • These questions help a potential lender determine your capacity to repay a debt and also how much credit could safely be extended to you.

Your Responsibilities • When you apply for and accept credit from a lender your actions indicate that you are aware of and agree to accept certain responsibilities. Some of your responsibilities as a borrower include: • Borrowing only what you can repay. • Not exceeding the credit limit established by your creditor(s). • Paying debts promptly. Notifying creditors immediately if you cannot meet payment schedules. • Not selling or disposing of merchandise before you have completely paid the creditor (if the seller has retained title to the item or has a lien against it). • Reporting lost or stolen credit cards promptly and not giving out card number information over the phone unless you initiated the call or are certain of the caller’s identity.

Your Rights • In addition to your responsibilities, you also have certain legal rights ensured by several important items of consumer protection legislation.

Fair and Accurate Credit Transaction Act (2003) • The Fair and Accurate Credit Transaction Act (FACTA) added new sections to the Fair Credit Reporting Act. FACTA helps consumers combat identity theft by giving them the right to request a free credit report from each of the three major credit agencies every year. Information on how to order your free credit report is available at the Federal Trade Commission’s website at www. ftc. org.

Truth in Lending Act (1968) • Ensures consumers are fully informed about the cost and conditions of borrowing.

Fair Credit Reporting Act (1970) • Protects the privacy and accuracy of information in a credit check.

Equal Opportunity Act (1974) • Prohibits discrimination in giving credit on the basis of sex, race, color, religion, national origin, marital status, age, or receipt of public assistance.

Fair Credit Billing Act (1974) • Established a procedure for the quick correction of mistakes that appear on consumer credit accounts.

Fair Debt Collection Practices Act (1977) • Prevents abuse by professional debt collectors, and applies to anyone employed to collect debts owed to others; does not apply to banks or other businesses collecting their own accounts.

• Other Protections • In addition to the laws just discussed, creditors are required to provide some other protections for consumers. • Credit for Payment • A card issuer must credit your account on the day payment is received unless the payment is not made in accordance with the creditor’s requirements. • Refunds • When you return merchandise or pay more than you owe, you have the option of keeping the credit balance in your account or receiving a refund. • Unauthorized Charges • If you report your consumer credit or debit card lost, you are not liable for unauthorized charges. • $50 Limit • If your card is used before you report it lost, you are liable for $0 if reported within two business days. After that, you are liable for no more than $50. • Disputes • In some cases you have the right to withhold payment for unsatisfactory merchandise or services.

Credit Card Costs Section!

Card Options - Credit vs. Debit • Besides using a credit card, consumers today can take advantage of other, equally convenient ways to pay with “plastic”. They can, for example, choose the convenience of a debit card instead of a check or cash. Consumers use a debit card like a credit card; however, the purchase is deducted from the cardholder’s checking account.

Introduction and Lesson Objectives In addition to debit cards, consumers can choose among several different types of credit card accounts. • Bank Cards • Refers to credit cards like Visa and Master. Card; issued by a bank or financial institution. Affinity cards are a form of bank-issued credit card that carry a photo or the name of a non-profit or other nonfinancial organization instead of the name or logo of the institution that issued it. • Store Cards • Store cards operate much like bank cards, but are issued by a particular retail store or manufacturer. Many store cards can only be used for purchases at the store that issued the card. • Travel and Entertainment Cards • Cards such as American Express, Carte Blanche and Diner’s Club differ from revolving credit cards in that they typically require that the balance be paid in full at the end of every month.

Premium Cards • Gold and platinum cards are high end credit cards that offer a blend of high credit limits and exclusive benefits. Issuing banks usually require gold and platinum cardholders to meet higher standards of income and credit worthiness. • The higher credit limit and other perks offered to users of these cards are especially attractive to frequent business and/or leisure travelers. Typical value-added services include rewards, rental car damage coverage, travel accident insurance and an extended warranty on items purchased with the card. Some charge an annual fee. It is important to consider a card's terms and determine which perks are really valuable before accepting a premium card.

Calculating the Cost of Credit • Perhaps one of the most important things to consider when choosing and then using a credit card is the additional cost attached to purchases made with a credit card. Most consumers are familiar with the APR or Annual Percentage Rate; the amount of interest a creditor adds, each month, to your unpaid balance. While the interest rate is the most obvious expense, it is not the only expense associated with using a credit card. Other, less apparent costs of credit card use are discussed in the following pages.

Pull Up Credit Card Calculator • http: //www. practicalmoneyskills. com/webc ourse/lesson 5/18. php

Interest and Finance Charges • When you use your credit card, the creditor or issuing bank is giving you a loan for the amount of your purchases. Creditors charge a fee, called interest, for the use of their money. The credit card company pays the dress shop or the furniture store within a few days of the transaction, and you must begin repaying the loan when your monthly statement arrives in the mail. • Interest charges can be avoided by paying the balance in full within the time limit specified on the statement. The quicker the balance is paid in full, the less interest is paid. Be sure to learn about the terms and policies of your credit card before running up a balance.

Calculating Finance Charges

Average Daily Balance • You pay interest on the average balance owed during the billing cycle. The creditor figures the balance in your account on each day of the billing cycle; adds these totals together and divides by the number of days in the billing cycle. Example: ($400 x 15) + ($100 x 15) = $250 x 30 days

Adjusted Balance • You pay interest on the opening balance after subtracting the payment or returns made during the month.

Previous Balance • You pay interest on the opening balance, regardless of payments made during the month.

Past Due Balance • No finance charge is added if the full payment is received within the grace period. If it is not received, a finance charge for the unpaid amount is added to your next bill.

Other Costs of Credit • In addition to the interest or finance charges applied to credit card purchases, consumers should be aware of other costs that may affect the true or actual cost of their credit purchases. Some less apparent credit costs include: • Miscellaneous or Annual Fees • Transaction and Cash Advance Fees

Annual and Miscellaneous Fees • Some credit card issuers require an annual fee - the amount you must pay to get a card or to renew it every year. In addition, consumers should be very familiar with their credit card company’s policy regarding fees for: • Submitting an application. • Being late with a payment. • Taking out a cash advance. • Exceeding your credit limit. • Maintaining a zero balance. • Read your statement carefully so that you know all of the terms and conditions that may affect the total cost of your credit card purchase.

Transaction Fees and Cash Advances • Financial institutions that issue credit cards typically treat cash advances like loans, not like purchases of merchandise. • When you take a cash advance, interest begins to accrue differently - sometimes without a grace period (the period of time between the date of the purchase and the date the interest charges apply) and at a higher rate. • Check with the institution that issued your card for the cash advance details associated with your credit card.

How Much Can You Afford? The 20/10 Rule • The 20 -10 rule makes a good "rule of thumb" for understanding how much credit you can afford. • Never borrow more than 20% of your yearly net income (not including your housing or mortgage debt). – Example: If your net income (after taxes) is $3, 000 per month, your annual income is $36, 000. Calculate 20% of your annual net income ($36, 000) to find your safe debt load-$7, 200. You should never have a total outstanding debt load (car payment, credit card balance, other debts) of more than $7, 200. • Monthly payments should not exceed 10% of your monthly net income. – Example: If your take-home pay is $3, 000 a month -- $3, 000 x 10% = $300. Your total monthly debt payment shouldn’t total more than $300 per month. You can practice your skill with the 20/10 rule by completing the 20/10 worksheet.

20/10 Worksheet

Credit Card Convenience • Credit cards provide an exceptionally high level of convenience. If you pay your balance each month, this convenience need not come at an additional price and you don’t pay anything extra for the flexibility and convenience of tracking your spending and making purchases without using cash or checks. • If you pay your balance in full every month, the interest rate on a credit card may matter less than the size of the annual fee or the option to earn a rebate when you use a particular card. • Cardholders who pay the balance in full each month might want to consider a co-branded card. These cards may have relatively high interest rates, but these rates won’t affect you if you pay your bill in full. • Some cards provide such extras as rebates, cash rewards, and free or discounted merchandise. If you pay your balance each month you may realize real value from these “extras”. Be aware that the extras may not last for the lifetime of the card.

Your Buying Habits • These days many credit cards offer rebates, frequent traveler miles and other special features. • Like the convenience aspect of a credit card, the value of these features is highly dependent on both your buying and repayment habits. • If you pay your balance in full every month, you might think a card that offers a rebate is right for you. • Read the offers thoroughly to find out how much you have to charge to earn rebates. If you don't think you will charge enough within the specified time to collect rewards, the higher interest rate and annual fee might not be worth it. • Check to see if the company charges interest from the date of the transaction. This method for calculating finance charges could cause you to pay interest even if you usually pay your balance in full every month. • If you occasionally carry a balance, the interest rate charged by the creditor might offset the value of the rebate or reward.

Do You Plan Ahead? • The convenience and value of various credit card features is also influenced by the extent to which you plan your purchases. Perhaps you are planning to redecorate, and you spot exactly the furniture you want on sale for hundreds of dollars less than you thought you'd have to pay. You've been having a good year, and you'll be getting your annual performance bonus in a few months. Your plan—charge the furniture to your credit card—pay what you can afford each month until bonus time and then pay off the entire amount. • It's a good plan if you: • Are sure the bonus will come. • Limit your spending to the amount of the bonus (don't treat it like an endless supply of money). • Have found a card with a credit limit high enough to accommodate the purchase and with a reasonable interest rate over the period of time you'll need to pay off the balance. • Using a card offering a low introductory rate can be one choice for financing large purchases over a short time. You must be certain you will pay off the balance and be comfortable with the terms.

Repayment Habits • Many credit card users regularly carry a balance. Most card users: • Pay more than the minimum payment required. • Shop for the card with the lowest rate in order to minimize the amount of interest to be paid every month. • Shopping for the lowest interest rate is a good strategy for users who expect to carry a balance from month to month. The exception: if your average balance is less than $1, 000, a hefty annual fee on a low-interest-rate card could negate the low interest rate. If you plan to keep your balance small, look for a no-annual -fee card with the lowest interest rate you can find.

Do’s and Dont’s • You can realize a great deal of value and convenience by making purchases using credit if you follow a few simple dos and don’ts. • Do: • Shop around for the best deal • Read the contract carefully • Keep a copy of the signed contract • Know the penalties for missed payments • Figure the total price when paying with credit • Buy on installment credit only after evaluating all other possibilities • Don't: • Rush to sign the application or contract • Be misled into thinking it will be easy to pay the debt off quickly, even if you make only small payments each month

Using Credit Wisely • In order to use credit wisely, you must have the information necessary to: • Identify all the available options. • Evaluate all the available options. • Select the best option for you. • Assess your ability to use credit wisely by completing the Wise Use of Credit Consumer Quiz.

Email Address • You need a steady email address. When you set up accounts online they are often identified by email address. • You are an adult now, have an adult email address. funkypants 18@hotmail. com is not a good one. How about your name or part of your name. • Keep it for ever so pick it carefully. Like a tattoo.

When Applying for Credit • Credit can be useful in times of emergencies and can be more convenient than cash. In order to manage your money wisely, however, ask yourself the following questions before applying for a credit card. • Do I need this? Do I need it now? • Can I wait to make my purchase until I have cash to pay for it? • How much more will am I likely to buy and how much more will I pay for what I buy if I buy it on credit? • Just to bring home the full cost of credit it’s a good idea to think about the following before you make a major credit card purchase. • Consumers with a credit card spend up to 33% more than if they shopped with cash. • If you purchase a $500 stereo with a credit card with a 20% APR, it will cost $1, 084 and take 9 years to pay off if you only pay the $10 minimum monthly payment.

Credit Questions When you apply for credit, be prepared to answer questions such as: How long have you been in your job? How much money do you make each month? What are your monthly expenses? Do you own a house? Do you have investments or other assets (e. g. a car)? How much do you owe? Do you have outstanding loans; e. g. school or student loans? Have you had credit in the past? How many credit accounts do you have? Have you ever been denied credit? Have you ever filed for bankruptcy? Have you ever had any property repossessed or foreclosed upon? Have you ever made late payments?

If Credit is Denied • Creditors consider the 3 C’s (as discussed earlier in this course) of Character, Capital and Capacity when making a determination of credit worthiness. There are some things you can do if you apply for credit and are turned down.

Valid Reasons for Denial • • If you think the reasons you were denied credit may be valid: • Ask the creditor if you can provide additional information or arrange alternate credit terms. • Apply to another creditor whose standards may be different. • Do the things you need to improve your credit worthiness.

Reasons May or May Not Be Valid If you are not sure whether or not the reasons you were denied credit are valid: Ask the creditor to explain why you were denied. Review your credit history If you find your credit history contains errors, take steps to correct the errors.

Reasons are Clearly Not Valid • If you believe the reasons you were denied credit are clearly not valid or that the creditor has discriminated against you: • Notify the federal enforcement agency whose name you were given by the creditor. The agency will investigate and report back to you. • If you can afford it, hire an attorney to file suit against the creditor. If the court determines the creditor did discriminate, the creditor will be required to pay you both actual and punitive damages

Managing Your Credit • Once you are granted credit: • If possible, pay off your entire credit card bill each month. If you can’t pay in full, try to pay more than the minimum balance. This will reduce finance charges and total interest paid. • Pay on time to avoid late fees and protect your credit. If you cannot pay on time, call your creditor immediately to explain the situation. • Always check your monthly statements to verify transactions. Call your creditor right away if you suspect errors on your statement. • Ignore creditor offers that allow you to “reduce” or “skip” payments. You will still be charged finance charges during this period. • Think about the cost difference if you purchase your item with cash versus using a credit card.

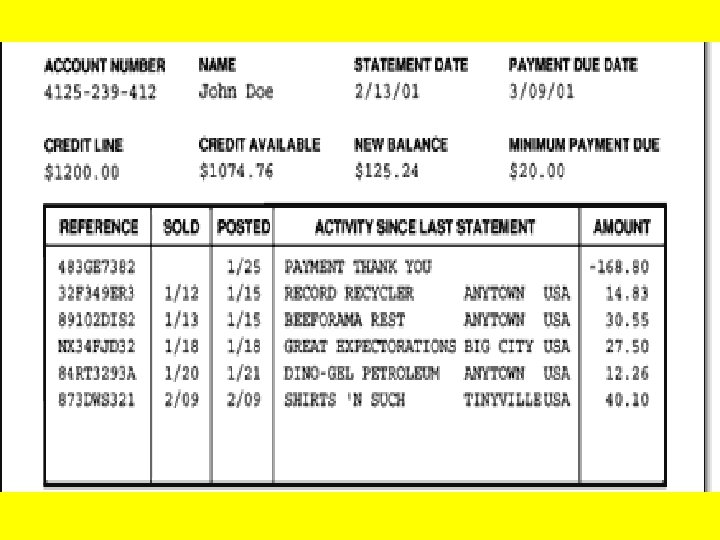

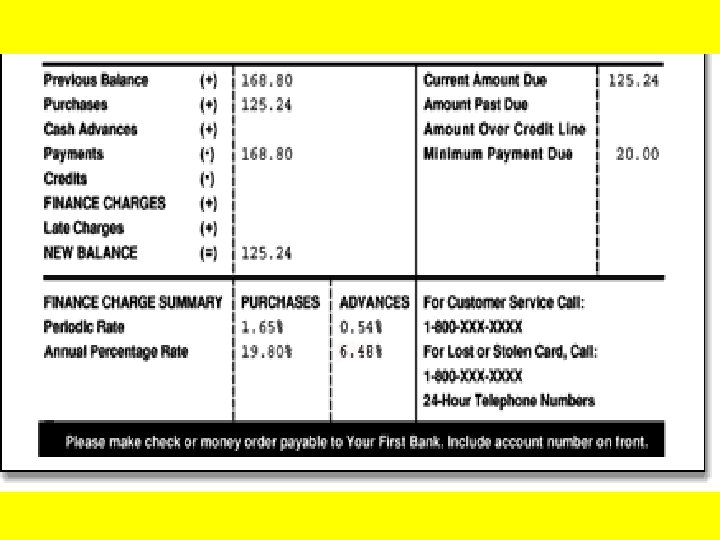

Reading your credit card statement • Go to next page (blow up)

Dealing With Billing Errors • You can challenge billing statement errors such as unauthorized purchases, charges for items that were never delivered, failure to credit a payment etc. • Notification • You must notify the creditor of a disputed item within 60 days. The creditor must investigate and, within two billing periods, either correct the mistake or explain why the charge is not an error. • Payment • You cannot be billed for or forced to pay a disputed amount until the creditor has finished the investigation. If it is determined that you are responsible for the bill, you must be given the usual amount of time to pay it. • Credit History • Your credit history is protected during the dispute process. • Statement of Rights • Creditors must supply customers with a statement of their rights at the time the account is opened and at least twice a year thereafter.

What is a Credit History? • A credit history is a record of an individual's or a company's past borrowing and repaying behavior. An individual’s credit history is communicated to potential creditors via a credit report compiled by a credit reporting bureau. • A credit report is a summary of the credit usage of a consumer, including payment histories and current status of all credit accounts. Credit reports play a very large part in the decision to grant credit to a consumer.

Establishing a Credit History? • Since credit is such an integrated part of our daily lives, most consumers need at least one credit card. Getting other types of credit such as a car loan can also be difficult if no credit history is available. • To build a credit history: • Establish a steady work record. • Pay all bills promptly. • Open a checking account and don’t bounce checks. • Open a savings account and make regular deposits. • Apply for a local store credit card and make regular monthly payments. • Apply for a small loan using your savings account as collateral. • Get a co-signer on a loan and pay back the loan as agreed.

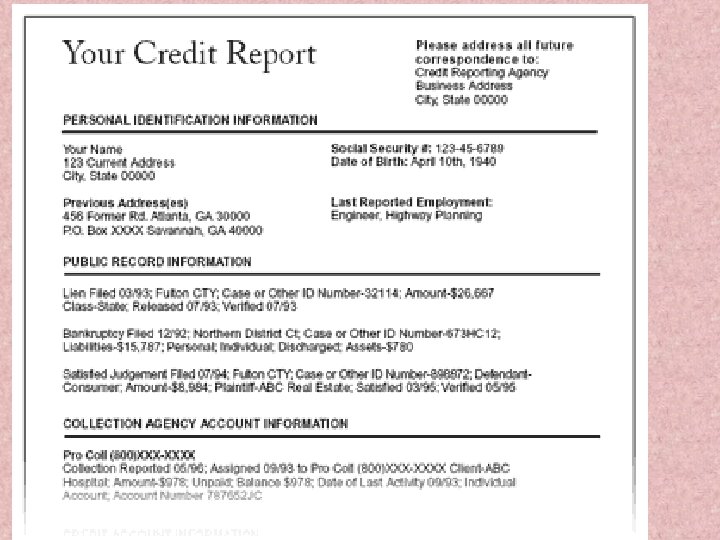

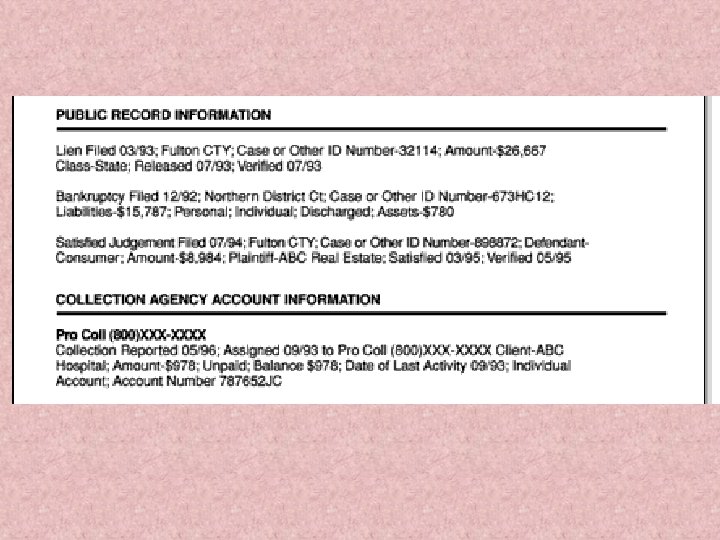

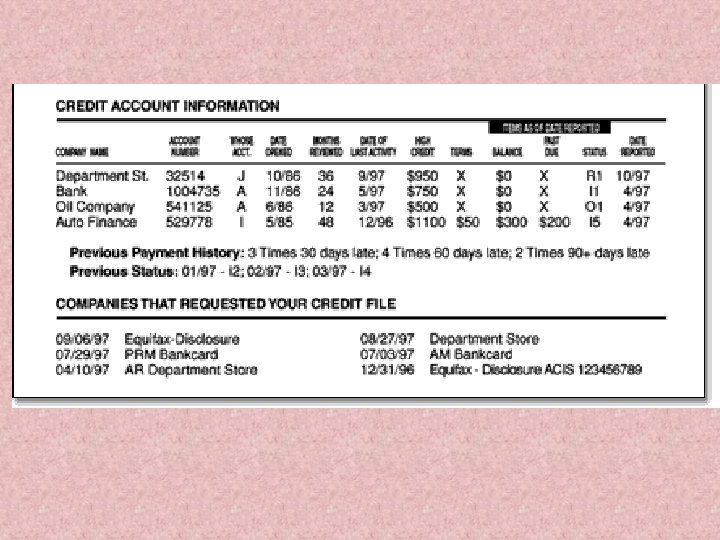

What is a Credit Report? A consumer’s credit history is assembled and communicated to creditors through a credit report. A credit report contains basic identifying information such as name, Social Security number and address etc. It may also include employer information and the consumer’s previous address(es). The historical information that is part of a credit report often includes previous and current types of credit, credit providers, payment habits, outstanding obligations and debts and the extent of the credit granted. The public record information is usually limited to tax liens, judgments, and bankruptcies. The names of those businesses that have requested information on the consumer in the recent past are also listed.

Who Prepares a Credit Report? • Credit reports are created and maintained by credit bureaus. There are three main credit bureaus - Equifax, Experian, and Trans Union. Each of their credit reports looks different. • Some creditors prefer to secure a credit report from a particular credit bureau while others may secure more than one report as part of their review.

What Does a Credit Report Look Like? Your credit report will have many codes on it. The Inquiries category can be especially important. Example – When someone shops for a car, it is possible that several different car dealers may request a bureau report. A creditor may turn down an application on the basis of "excessive inquiries", thinking the person has made an unusually large number of applications and been turned down, when in actuality the inquiries were made while the individual was still in the “shopping” phase. It is important secure and review a copy of your credit report from time to protect yourself from potential identity theft and to detect inaccuracies.

Who Gets and Uses a Credit Report? • As a result of the Fair and Accurate Credit Transaction Act of 2003 you can get a free copy of your credit report every year. Financial institutions see it when you apply for loans, mortgages and credit. Landlords can access it when you apply for a lease. Employers may use it when they are considering you for employment and even for promotion.

• Inquiries • If you apply for credit frequently many inquiries may be shown on your report. Creditors are concerned when they see "excessive inquiries". • Shopping Habits • When shopping for a car, furniture or other big ticket item you will be purchasing on credit, control the number of companies you negotiate with. You may not want to take the discussion to the “credit report” stage with more than one or two organizations. • Challenges • The Fair Credit Reporting Act allows only authorized inquiries. You can challenge an inquiry if you feel the company was not authorized by you to make an inquiry.

Assigning a Credit Rating • information in your credit report indicates how well you pay back your bills pay on time, and in full. Late and missed payments • What is sometimes referred to as a "rating" is a credit score or complex calculation that helps the creditor understand the chance of a default. A specific credit score does not translate directly or automatically into a "yes" or "no" to credit. • Creditors decide whether to grant a loan or provide a credit card based on their own criteria and the history they see on the report as well as what products they have to offer.

Credit Ratings • Credit reports do not actually contain a “single” line item called Credit Rating. Each bureau collects information it receives from the credit granting community: banks, finance companies, department stores, taxing authorities, landlords and other credit grantors. • • • A Credit Score may appear or FICO (300 to 850) 35% - payment history 30% - current debt 15% - length of credit history 10% - type of credit used 10% - recent credit requests

Repairing Your Credit Rating • The extent to which you can change or influence the information in your credit report depends on the nature of the problem.

• • • Correcting Errors and Mistakes Correct inaccuracies have the proof • • Managing Negative Information information that is accurate but negative can be reported for seven years. • Exceptions • Bankruptcy information can be reported for 10 years. • Information based on an application for a job with a salary of more than $20, 000 has no time limitation. • Information concerning a lawsuit or judgment can be reported for 7 years or until the statute of limitations runs out, whichever is longer • Using Credit Repair Agencies They are often scams. �You ’tcan legally repair negative info unless false.

Too Many Credit Cards • Different lenders look at credit worthiness in different ways. Some look at the total credit limit on each account that you have. Some look at the total number of cards and the credit limit available to you, rather than your actual debt. 70% is the magic number.

Test Tomorrow