Unit 4 Market Structures Prof Prasanna Shembekar Determinants

Unit 4 : Market Structures Prof Prasanna Shembekar

")

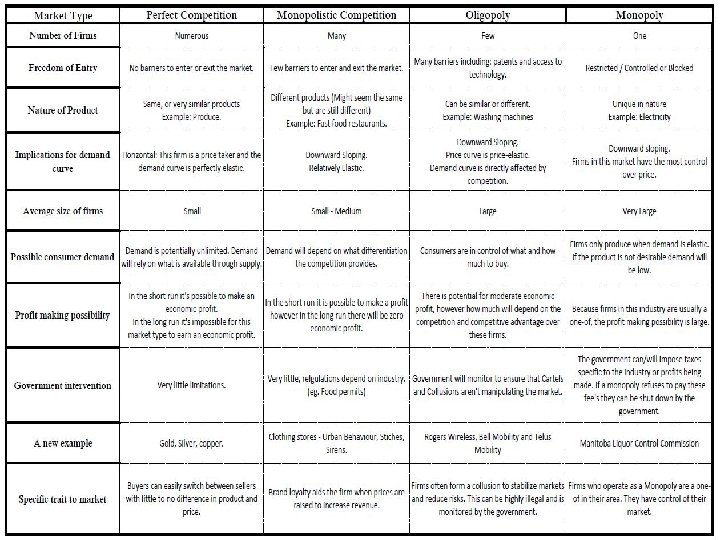

Determinants of Market Structure • • • Number and nature of sellers ( Competition) Number and nature of buyers Nature of product Entry and exit conditions Economies of scale • Perfect competition is where there is absence of rivalry. So markets are basically classified as perfect and imperfect competition markets.

Classification of Markets based on competition • Perfect Competition • Imperfect competition – Monopoly – Oligopoly – Monopolistic Competition

Perfect Competition: Characteristics • Large number of buyers and sellers • Homogeneous product • Free Entry and exit from the market ( no barriers to entry or exit) • Perfect Knowledge of market to both buyers and sellers (specifically prices) • Cost of transportation is nil or same for all • Absence of selling costs( marketing costs)

Price determination in perfect competition • Price of a product is determined at a point at which the demand supply curve intersect each other. • This point is known as equilibrium point as well as the price is known as equilibrium price. • In addition, at this point, the quantity demanded and supplied is called equilibrium quantity.

Price determination in Short run • Under perfect competition, a firm will not have any independence to fix the price of its own product. The industry is the price –maker and the firm is the price-taker. • In case of a firm, the price line which is equal to AR and MR, will be horizontal and parallel to OX axis. It shows that the same price has to be charged by the firm for all units supplied, irrespective of changes in demand. • Equilibrium or market price = AR =MR • In the short run, an industry reaches the equilibrium position when: • 1 There is no scope for the new firms to enter or exit the industry. • 2 Short run demand should be equal to the short term supply. Hence, short-term price is not a stable price. • 3 There is no scope for expansion or contraction of the output in the entire industry. The total output remains constant in the short run at the equilibrium point where MR=MC.

Figure A shows price determination for the Industry and Figure B shows for the firm (in short run)

Short run price determination for the firm : Super normal profits when Price >AC

Short run price determination for the firm : normal profits when Price = AC

Short run price determination for the firm : Losses when Price < AC

Conclusion for Short run price determination • In short run, a firm can either incur losses or earn supernormal profit or normal profit. • The main reason for this is that the firm does not get adequate time to make all kinds of adjustments to avoid losses in the short run.

Long Run • In long run, a firm will attain only normal profit where P=AR=AC=MR=MC. • If AR is greater than AC, then the firm will earn supernatural profit and it will lead to the entry of new firms, as a result, increase in the total number of the firms and finally increase in supply and fall in price and ratio of profits. • This process will continue till supernatural profits are reduced to zero. On the other hand, if AR is less than AC, loss will occur and this will lead to the exit of old firms, decrease in the number of the firms, decrease in supply and rise in price and finally the rise in the ratio of profits. Such process will continue until the firm reaches to the equilibrium position where AC =AR.

• In the long run, industry has the sufficient time to make all kinds of changes, adjustments and readjustments in the production process. • All the inputs becomes variable in the long run and the production can be either increased or decreased according to the demand as a whole. • In the long-run, an industry will reach to the position of equilibrium under the following conditions • 1 The long run demand supply of the products of the industry must be equal to each other and it will determine the long run normal price. • 2 All the firms in the industry should also be in the equilibrium position where MC=MR and AC=AR. All the firms should earn only normal profits and this will help the industry to attain a stable equilibrium in the long run. • 3 The total number of firms in the industry should remain constant.

Long run equilibrium will be where LMC=LMR=LAC=LAR=P

Monopolistic Competition • Monopolistic Competition refers to a market situation in which there are large numbers of firms which sell closely related but differentiated products. Markets of products like soap, toothpaste, clothes, etc. are examples of monopolistic competition. • Under monopolistic competition, each firm is the sole producer of a particular brand or “product”. • Every firm strives to create its own small monopoly • However, since the various brands are close substitutes, its monopoly position is influenced due to stiff ‘competition’ from other firms.

Features or characteristics of Monopolistic Competition • 1. Fairly good Number of Sellers: • There are good numbers of firms selling closely related, but not homogeneous products. Each firm acts independently and has a limited share of the market. So, an individual firm has limited control over the market price. Large number of firms leads to competition in the market. • 2. Product Differentiation: • Each firm is in a position to exercise some degree of monopoly (in spite of large number of sellers) through product differentiation. Product differentiation refers to differentiating the products on the basis of brand, size, colour, shape, etc. The product of a firm is close, but not perfect substitute of other firm.

Features / Characteristics • 3. Selling costs: • Under monopolistic competition, products are differentiated and these differences are made known to the buyers through selling costs. Selling costs refer to the expenses incurred on marketing, sales promotion and advertisement of the product. Such costs are incurred to persuade the buyers to buy a particular brand of the product in preference to competitor’s brand. Due to this reason, selling costs constitute a substantial part of the total cost under monopolistic competition. • It must be noted that there are no selling costs in perfect competition as there is perfect knowledge among buyers and sellers. Similarly, under monopoly, selling costs are of small amount (only for informative purpose) as the firm does not face competition from any other firm.

Features / Characteristics • • • 4. Freedom of Entry and Exit: Under monopolistic competition, firms are moderately free to enter into or exit from the industry at any time they wish. It ensures that there are neither abnormal profits nor any abnormal losses to a firm in the long run. However, it must be noted that entry under monopolistic competition is not as easy and free as under perfect competition. 5. Lack of Perfect Knowledge: Buyers and sellers do not have perfect knowledge about the market conditions. Selling costs create artificial superiority in the minds of the consumers and it becomes very difficult for a consumer to evaluate different products available in the market. As a result, a particular product (although highly priced) is preferred by the consumers even if other less priced products are of same quality. 6. Pricing Decision: A firm under monopolistic competition is neither a price- taker nor a price-maker. However, by producing a unique product or establishing a particular reputation, each firm has partial control over the price. The extent of power to control price depends upon how strongly the buyers are attached to his brand.

Features / Characteristics • 7. Non-Price Competition: • In addition to price competition, non-price competition also exists under monopolistic competition. Non-Price Competition refers to competing with other firms by offering free gifts, making favourable credit terms, etc. , without changing prices of their own products. • Firms under monopolistic competition compete in a number of ways to attract customers. They use both Price Competition (competing with other firms by reducing price of the product) and Non-Price Competition to promote their sales.

Price Determination in shot run: Supernormal profits • At profit maximization, MC = MR, and output is Q and price P. Given that price (AR) is above ATC at Q, supernormal profits are possible (area PABC). • As new firms enter the market, demand for the existing firm’s products becomes more elastic and the demand curve shifts to the left, driving down price. Eventually, all super-normal profits are eroded away.

Price determination in long run : Normal profits • Super-normal profits attract in new entrants, which shifts the demand curve for existing firm to the left. New entrants continue until only normal profit is available. At this point, firms have reached their long run equilibrium. • Clearly, the firm benefits most when it is in its short run and will try to stay in the short run by innovating, and further product differentiation.

Monopoly • A monopoly is an economic market structure where a specific person or enterprise is the only supplier of a particular good. • Monopoly has a downward sloping demand instead of the “perceived” perfectly elastic curve of the perfectly competitive market. • There is no difference between organization and industry under monopoly. Accordingly, the demand curve of the organization constitutes the demand curve of the entire industry. • The demand curve of the monopolist is Average Revenue (AR), which slopes downward.

Characteristics of a Monopoly Profit maximizer: a monopoly maximizes profits. Due to the lack of competition a firm can charge a set price above what would be charged in a competitive market, thereby maximizing its revenue. Price maker: the monopoly decides the price of the good or product being sold. The price is set by determining the quantity in order to demand the price desired by the firm (maximizes revenue). High barriers to entry: other sellers are unable to enter the market of the monopoly. Single seller: in a monopoly one seller produces all of the output for a good or service. The entire market is served by a single firm. For practical purposes the firm is the same as the industry. Price discrimination: in a monopoly the firm can change the price and quantity of the good or service. In an elastic market the firm will sell a high quantity of the good if the price is less. If the price is high, the firm will sell a reduced quantity in an elastic market.

Sources of Monopoly Power / Barriers of entry In a monopoly, specific sources generate the individual control of the market. Sources of power include: • Economies of scale • Capital requirements • Technological superiority • No substitute goods • Control of natural resources • Legal barriers

Short Run Price determination in Monopoly : Three situations may arise as Monopolist may not have control over costs.

Price determination in Long Run In the long period the monopolist introduces changes in his equipment’s and techniques of production. During this period in order to gain excess profit, he will change efficiency and capacity of his resources according to his need. A monopolist can reduce his Long term Average costs considerably in the long run as he has control over technology, scale and other economies of scale.

Oligopoly • Oligopoly is a market structure in which a small number of firms have the large majority of market share. • An oligopoly is similar to a monopoly, except that rather than one firm, two or more firms dominate the market. • There may be smaller firms in the market but their existence is negligible. • Examples of oligopoly are airlines industry, steel industry and telephone services (telecom) industry.

characteristics of an oligopoly • Few sellers. They are interdependent on each other. • Barriers to entry: There are very high barriers to entry. Those barriers can be artificial such as high investment costs, of natural barriers such as limited access to raw materials, etc. • Strategy and strategic game : Firms have to take strategic decisions whether to compete with other firms or to collude with them (join hands with them). • Degree of competition: There is very stiff competition among few competitors. • Price rigidity: Firms stick to the prices and do not change prices often as the firms are interdependent. • Group Behaviour: It is an important characteristic as in oligopolies all major firms may act like rivals, followers of friends. • Less focus on product differentiation than price differentiation. Products are mostly homogeneous in nature

, rather")

Collusive Oligopoly • In oligopolistic markets firms may attempt to collude (unite together), rather than compete. • If colluding, participants act like a monopoly and can enjoy the benefits of higher profits over the long term. • Such association of major firms in oligopoly is called collusive oligopoly.

Figure 1: Price and output determination in collusion Price for every firm and the industry is same. RSEG is profit of firm A and ABEG is profit of firm 2. Total profit of Industry is the addition of all profits which is equal to PFEG in figure 3. Quantity of industry is addition of quantities of all industries.

• Non Collusive monopoly • In this type of monopoly firms compete with each other instead of colluding. • Firms are not dependent on each other directly. • It follows Kinked demand curve model stated by Paul Sweezy • Price remains more stable than the cost due to the price stickiness. If one firm increases price, others will not increase. This way the firm that increases price will face sales loss. But if one firm reduces price others will also reduce in order to minimize the benefit of price reduction to the first firm • Firms aim at individual profits rather than collective profits • Firms do not tend towards monopoly • Consumers are at benefit as they get the benefit of price war between the rival sellers.

Kinked demand curve model: • There are only a few firms in an oligopolistic market. • The firms are producing close-substitute products. • A set of prices of the product has already been determined and these prices prevail in the market at present. • Each firm believes that if it reduces the price of its product, the rival firms would follow suit, but if it increases the price, then the rivals would not follow it, they would simply keep their prices unchanged.

• If the firm prices above P 1, the demand will be highly elastic as other firms will not follow the price rise and there will be direct impact on demand for the firm Below P 1 , demand becomes inelastic as further reduction in price below P 1, other firms will follow the price reduction and there will not be any significant benefit in demand to the firm as everybody has reduced the price. Marginal revenue curve is discontinuous at X and falles steeply after X showing that revenues fall steeply after X Hence there is a kink in demand curve at point X. So actually there are two demand curves in non collusive oligopoly During discontinuity of MR , marginal cost can be changed between MC 1 and MC 2. Above MC 1 , it will change the price point X

Meaning of Pricing • Pricing is a managerial task that involves establishing pricing objectives, identifying factors governing the price, deciding their significance and relevance, determining product value in monetary terms and formulation of pricing policies, strategies, methods to implement and control them. • In involves costing, fixing mark up and schemes to present price in the market.

Objectives of pricing • • • Profit maximization Sales maximization and growth Preventing/ facing competition Market penetration Skimming the market cream Earning a market share Survival Achieving Target Rate of return Positioning

Factors affecting pricing • Internal Factors • Organization’s Objectives • Factor costs • Marketing costs • External Factors • Consumer Psychology and demand • Competition • Government Policies

Pricing Methods

- Slides: 38