Unit 3 4 Final Accounts Source Business Management

Unit 3. 4 Final Accounts Source: Business Management Textbook by Paul Hoang

• Financial reporting is a way to account for")

Purpose of Final Accounts (FA) • Financial reporting is a way to account for the money of the business, whether it belongs to the owners, investors or lenders. • Financial accounts ensure that all payments and receipts of a business have to be officially accounted for. • All companies (businesses owned by shareholders) must provide a set of final accounts • Accounts consist of 2 statements: • Profit and Loss Account • Balance Sheet

• FA are legal requirements in most countries for")

Purpose of Final Accounts (FA) • FA are legal requirements in most countries for companies to have their final accounts audited by independent and chartered accountants who certify the financial statement to be accurate and truthful. • Incorporated businesses are legally obliged to produce FA, which act to ensure transparency in their use of funds. • There is no universal method to present the FA, there is some degree of flexibility in reporting the ‘actual’ financial position of a company; much of this comes down to the auditor’s professional judgment.

Purpose of FA for different stakeholders: • Shareholders • Owners of the company are interested to see where their money was spent and the return on their investments. • Owners use FA to decide whether to hold, sell or buy more of the company’s shares.

Purpose of FA for different stakeholders: • Employees • Staff are interested in their organization’s FA to assess the likelihood of pay increments and the degree of job security. • Salary increments are often expressed as a percentage of an employee's overall base pay. An increment usually represents a portion of what the employee earns per year. Employers use increments to increase or decrease base salaries or to award bonuses. (http: //work. chron. com/)

Purpose of FA for different stakeholders: • Managers • FA are used to judge the operational efficiency of the organization. • Financial analysis can also be useful for target setting and strategic planning.

Purpose of FA for different stakeholders: • Competitors • Rivals are interested in the FA of a business to make comparisons of their financial performance (more on Unit 3. 5).

Purpose of FA for different stakeholders: • Government • The tax authority examines the accounts of business, especially large MNCs to ensure that they pay the correct amount of tax.

Purpose of FA for different stakeholders: • Financiers • Financial lenders such as banks or business angels scrutinize the accounts of a firm before approving any funds. • Business angels are wealthy entrepreneurs who risk their own money by investing in small to medium-sized businesses that have high growth potential.

Purpose of FA for different stakeholders: • Suppliers • They examine the firm’s FA to decide the extent to which trade credit should be given. • Trade credit allows a business to ‘buy now and pay later’. The credit provide doe not receive any cash from the buyer until a later date (usually allow between 30 -60 days).

Purpose of FA for different stakeholders: • Potential investors • Private and institutional investors use FA and Ratio Analysis (unit 3. 5) to assess whether an investment would be financially worthwhile.

The principles and ethics of accounting practice • The Association of Chartered Certified Accountants (ACCA) is a global regulatory body for professional accountants, assuring that its members are appropriately regulated. • Accountants and Financial Professionals must abide by the principles and ethics of accounting practice to maintain a positive reputation for the businesses and to prevent fraudulent practices.

ACCA’s Code of Ethics & Conduct: 5 guiding principles for accounting practice • Integrity - practice must be straightforward and honest; fair and truthful behavior • Objectivity - practice should be free from bias and any conflict of interest • Professional competence and due care - Accountants to maintain professional knowledge and skills and must act diligently when providing professional accounting services • Confidentiality - Accountants must respect the confidentiality of information they acquire in their professional duties • Professional behavior – Accounting practices must comply with relevant laws and regulations. Accountants to behave with courtesy and consideration toward others.

• Also known as Income Statement • P&L is")

Profit and Loss Account (P&L) • Also known as Income Statement • P&L is a financial statement of a firm’s trading activities over a period of time, usually one year. • Main purpose is to show the profit or loss of a business during a particular trading period. • There are 3 sections of an income statement: • The trading account • The profit and loss account • The appropriation account

TRADING ACCOUNT

Ways to improve gross profit • Using cheaper suppliers • This reduces the COGS although finding cheaper suppliers without hindering quality can be problematic • Increase selling price • This raises the value of each item sold, but is likely to cause a fall in the volume of sales • Enhanced marketing strategies • Promotion, packaging to make the product appealing but will raise the firm’s expenses

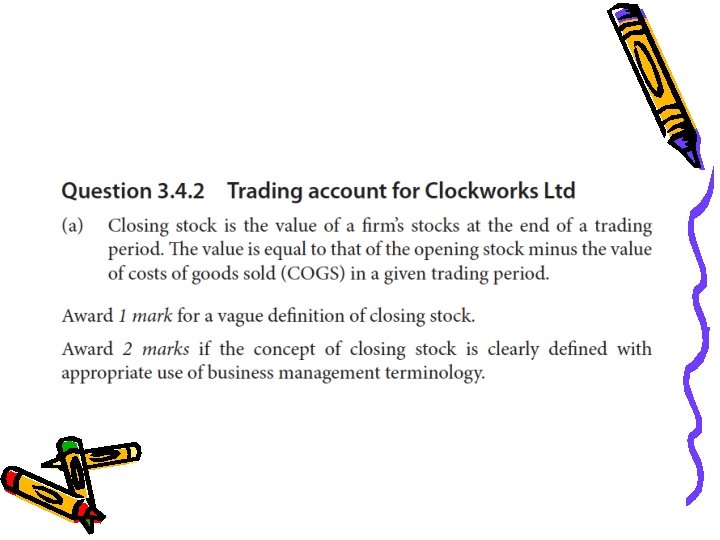

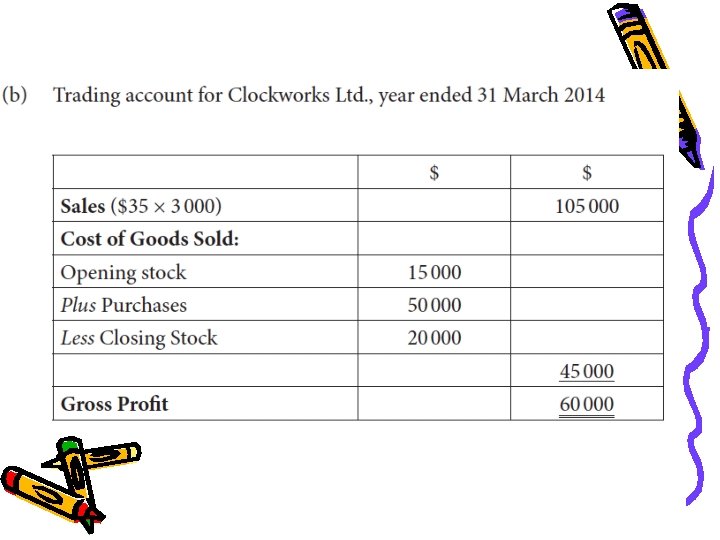

Exercise Question 3. 4. 2 Trading account for Clockworks Ltd.

The information below represents data for Clockworks Ltd. • • 3, 000 clocks sold at $35 each Closing stock valued at $20, 000 Purchases totaled $50, 000 Stock at April 1, 2013 was valued at $15, 000 (a) Define the term closing stock (b) Construct a trading account for Clockworks Ltd. for the year ended March 31, 2014.

Account")

Profit and Loss (P&L) Account

Account • Also known as ‘Profit Statement’ shows the net")

Profit and Loss (P&L) Account • Also known as ‘Profit Statement’ shows the net profit (or loss) of a business at the end of the trading period. • Net profit = Gross profit – Expenses • Expenses are the indirect or fixed costs of production

Ways to increase net profit • Rent charges could be negotiated • Fuel consumption such as heating and lighting could be targeted • Administration costs could be examined by reviewing the work of clerical staff to reduce costs • Combine jobs or employ fewer people to carry out certain tasks

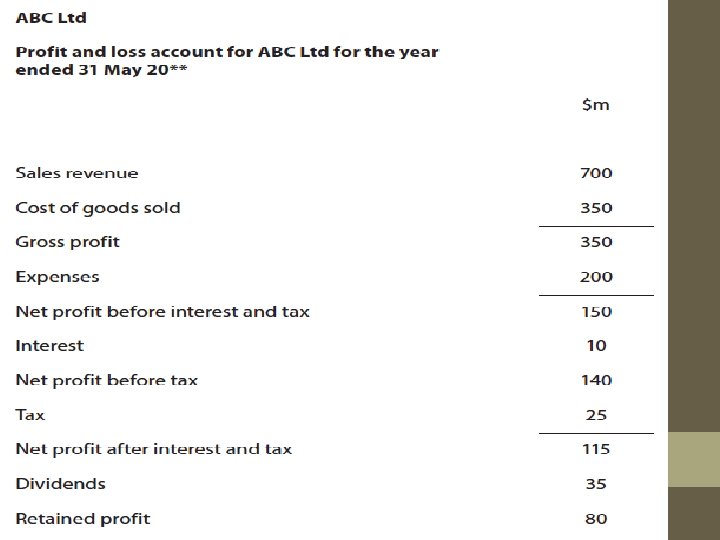

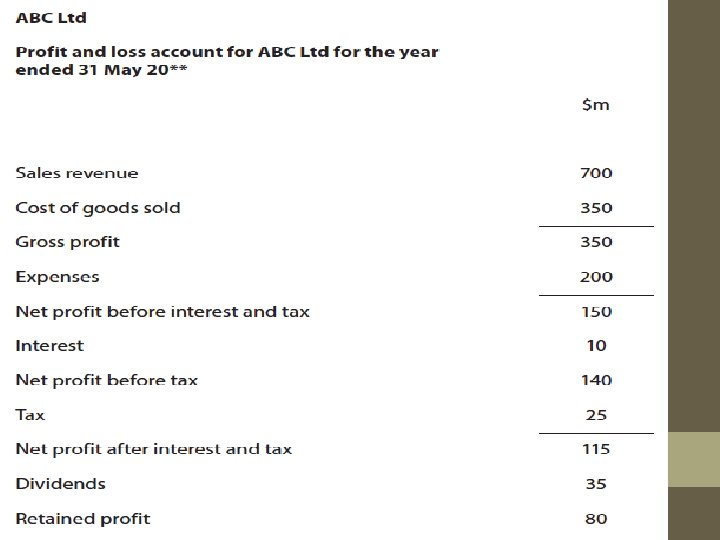

EXAM TIP! n What’s the correct format? Different firms in different countries use slightly different methods to present their P&L accounts. For your IB exams, use the format shown in Figure 3. 4. c. Remember to place an appropriate title at the top.

EXAM TIP! n Corporate tax is the compulsory levy imposed by governments on company profits. This figure is transferred to the balance sheet and shown as a current liability.

Exercise Question 3. 4. 3 Masks-R-Us Ltd.

Appropriation Account • Final section of the P&L account • 2 parts: • Dividends • Retained profit

Appropriation Account: DIVIDENDS • This shows the amount of net profit after interest and tax that is distributed to the owners (shareholders) of the company. • The share of net profit (after interest and tax) allocated to shareholders is based on the decision of the Bo. D and is approved at the company’s Annual General Meeting. • Usually paid biannually. An interim dividend is paid approximately half way through the year and then the final dividend is declared and paid at the end of the firm’s fiscal year. • The figures are transferred to the Balance Sheet and shown under CURRENT LIABILITIES.

Appropriation Account: RETAINED PROFIT • This shows how much of the net profit after interest and tax is kept by the business for its own use, such as investing it in the company or to expand the business. • This figure is transferred to the “Financed by” section of the firm’s balance sheet.

Limitations to the P&L account • P&L shows historical performance of a business. There is no guarantee that future performance is linked to past performance or success. • Window dressing can occur (the legal manipulation of FA to make them look financially more attractive. This disguises the underlying financial position of the company. • As there is no internationally standardized format for producing a P&L account

EXAM TIP! n It is common practice for firms to report their P&L account for two consecutive years to allow historical comparisons. n See Question 3. 4. 4

Exercise Question 3. 4. 4 Ahmed Educational Books Ltd.

The Balance Sheet • Companies are required to produce for auditing purposes • Contains information on the value of an organization’s assets, liabilities and the capital invested by the owners • As it shows the financial position of a business on one day only (usually the last day of the accounting year), it is often described as a ‘snapshot’ of a firm’s financial situation. • Helps ensure that all monies within the organization are properly accounted for

3 Parts of the Balance Sheet: • Assets • Items of monetary value that are owned by a business • Liabilities • Legal obligation of a business to repay its lenders or suppliers at a later date (amount of money owed by the business) • Equity (capital and reserves) • Shows the value of the business belonging to the owners Formula: Total Assets – Total Liabilities = Owner’s Equity

ASSETS • Fixed Asset • Any asset used for business operations (rather than for selling) and is likely to last for more than 12 months from the B/S date • Current Asset • Refers to cash or any other liquid asset that is likely to be turned into cash within 12 months of the B/S date • Types: Cash, Debtors, Stocks

EXAM TIP! n An asset belongs to a business but this does not mean that it has been paid for. A building (asset) could be worth millions of dollars, but is funded mainly by debt with the remaining amount being the equity.

LIABILITIES • Current Liabilities • Debts that must be settled within one year of the balance sheet date • Ex. Taxes owed to the government, dividends to shareholders and bank overdrafts • Long-term liabilities • Debts that are due to be repaid after 12 months • Ex. They are sources of LT borrowing • Debentures, mortgages and bank loans

This section shows the value of the business belonging to")

EQUITY (Capital and Reserves) This section shows the value of the business belonging to the owners. It can appear in 2 ways: • Shareholder’s Equity • For limited liability companies • Owner’s Equity • Businesses other than limited companies

Two main sections: • Share Capital • Refers to the")

EQUITY (Capital and Reserves) Two main sections: • Share Capital • Refers to the amount of money raised through the sale of shares • It shows the value when the shares were first sold, rather than the market value • Retained Profit • Amount of net profit after interest, tax and dividends have been paid • Reinvested in the business for its own use • Money belongs to the owners • The figure comes from the firm’s P&L account

Balance Sheet Formula: • Total assets – Total Liabilities = Equity • Review Page 261

EXAM TIP! What’s the correct format? n Different firms and different countries use slightly different methods to present their balance sheets. n In the IB exams, use the format presented in Figure 3. 4. g. n Remember to place an appropriate title at the top of the balance sheet.

EXAM TIP! n n The main difference between the balance sheet of incorporated and unincorporated businesses is that share capital does not appear as part of their equity because the latter do not have shareholders. The vast majority of examination questions will ask you to interpret the balance sheet of a limited liability company.

Limitations of Balance Sheet • Static documents – financial position of a business may be different in subsequent periods • Figures are only estimates of the values of assets and liabilities • Different businesses will produce accounts in varying formats and include different assets and liabilities which makes difficult to compare financial positions of different firms • Not all assets are included esp. intangible assets and the value of human capital

Exercise Question 3. 4. 5 Marc Brothers Ltd.

Exercise Question 3. 4. 6 Zawada Electronics Ltd.

Exercise Question 3. 4. 7 Senjaya Fabrics Ltd.

Intangible Assets • These are non-physical fixed assets that have the ability to earn revenue for a business • Examples: brand names, goodwill, trademarks, copyrights and patents • Protected by intellectual property rights • Intangible assets can account for a large proportion of a firm’s asset value, although it is usually difficult to place an objective and accurate price on such assets.

Intangible Assets Intangible Asset Video: http: //www. investopedia. com/terms/i/intangibleasset. asp Calculated Intangible Value: http: //www. investopedia. com/terms/c/civ. asp

Intangible Asset: BRAND • Brand recognition and brand value help to drive global sales for companies (ie. Apple, Coca-cola) • According to Forbes, the Apple brand is worth $104 billion. The Microsoft, Coca-Cola and IBM brands are worth more than $50 billion • Branding is an indefinite asset as brand recognition and brand loyalty stay with the company for as long as it operates.

Intangible Asset: PATENTS • Provide legal protection for inventors, preventing others from copying their creation for a fixed number of years • Act as an incentive to stimulate innovation • Allow the inventor to have exclusive rights to commercial production for a specified time period • Other firms must apply and pay a fee to the patent holder if they wish to use or copy the ideas, processes or products created by the inventor

Intangible Asset: COPYRIGHT • Provides legal protection for the original artistic work of the creator (author, photographer, painter or musician) • Ex: newspaper, sound recordings, computer software and movies • Anyone wishing to reproduce or modify the artist’s work must first seek permission from the copyright holder, usually for a fee.

Intangible Asset: GOODWILL • Value of an organization’s image and reputation. • Value of the firm’s customer base and its business connections. • Goodwill is the sum of customer and staff loyalty and can provide a major competitive edge for any business. • “Goodwill is the one and only asset that competition cannot undersell or destroy” – Marshal Field, US entrepreneur.

Intangible Asset: REGISTERED TRADEMARK • Distinctive signs that uniquely identify a brand, a product or a business. • Can be expressed by names, symbols, phrases or an image • It can be sold so ownership can be transferred for appropriate fees and is reflected in the firm’s balance sheet • Example: In 1993 Volkswagen bought the Bentley brand for 430 million pounds ($860 million)

Key Terms Review

Appropriation Account • Refers to the final section of a P&L account and shows how the net profit after interest and tax is distributed, ie. dividends to shareholders and/or retained profit kept by the business.

Balance Sheet • Contains financial information on an organization’s assets, liabilities and the capital invested by the owners on one specific day, thus showing a ‘snapshot’ the firm’s financial situation.

Book Value • Is the value of an asset as shown on the balance sheet. • The market value of assets can be higher than its book value because of intangible assets such as the brand value or the goodwill of the business.

or Cost of Sales (COS) • Shown in the")

Cost of goods sold (COGS) or Cost of Sales (COS) • Shown in the trading account and represents the direct costs of producing or purchasing stock that has been sold.

• Is the fall in the value of fixed assets over time,")

Depreciation (HL) • Is the fall in the value of fixed assets over time, from wear and tear (due to the asset being used) or obsolescence (outdated or out of fashion).

Final Accounts • Are the published annual financial statements that all limited liability companies are legally obliged to report, i. e. the balance sheet and the P&L accounts.

Fixed Assets • Are items owned by a business, not intended for sale within the next 12 months, but used repeatedly to generate revenue for the organization, e. g. land, premises and machinery.

Goodwill • Is an intangible asset which exists when the value of a firm exceeds its book value (the value of the firm’s net assets).

Gross Profit • Is the difference between the sales revenue of a business and its direct costs incurred in making or purchasing the products that have been sold to its customers.

Historical Cost • Refers to the purchase cost of a particular fixed asset.

Intangible Assets • Are fixed assets that do not exist in a physical form, e. g. goodwill, copyrights, brand names and registered trademarks.

Net Assets • Show the value of a business by calculating the value of its assets minus its liabilities. This figure must match the equity of the business in its balance sheet.

that a business makes after all")

Net Profit • Is the surplus (if any) that a business makes after all expenses have been paid for out of gross profit.

P&L Account or Income Statement • Is a financial record of a firm’s trading activity over the past 12 months, consisting of 3 parts: the trading account, the P&L account and the appropriation account.

Retained Profit • Is the amount of net profit after interest, tax and dividends have been paid. It is then reinvested in the business for its own use.

Share Capital • Refers to the amount of money raised through the sale of shares. It shows the value raised when the shares were first sold, rather than their current market value.

")

DEPRECIATION (HL)

Depreciation • Depreciation is the fall in the value of fixed assets over time due to: ØWear and tear – cause to raise maintenance cost ØObsolescences – out of date assets (old versions)

of fixed assets over their")

Depreciation • Depreciation spreads the historic cost (purchase cost) of fixed assets over their useful lifespan. • The change in the value of fixed assets is shown by reassessing their value on the balance sheet. • It needs to be recorded in order to: • Calculate the value of a business more accurately. • Realistically assess the value of fixed asset over time. • Plan for the replacement of assets in the future.

Methods of calculating depreciation Tangible Assets: • Straight line method • Reducing balance method Intangible Assets: • Amortization

Straight line method of Depn. • Simplest and most commonly used, however depreciating fixed assets by an equal amount each year is not realistic • Variables: ØLife expectancy of the asset (how long it is intended to be used before it needs to be replaced) ØResidual value of the asset (how much it is worth at the end of its useful life) ØPurchase cost of the asset • Annual depreciation = Purchase Cost Lifespan • Annual depreciation = Purchase Cost less Residual Value Lifespan

Reducing Balance Method • Depreciates the value of an asset by a predetermined percentage for the duration of its useful life. • This reduces the value of an asset by a larger amount in the earlier years of its useful life. • This method is more realistic in representing the falling market value of fixed assets over time. However, it is not as straightforward to calculate and deciding on the annual rate of depreciation is somewhat subjective. • Net book value = Historical cost less Accumulated Depreciation • Annual depreciation = Ending Net Book Value x annual rate of depreciation (%)

Lifespan of capital equipment

EXAM TIP! n As always with quantitative techniques, it is vital to look beyond the financial data. You should consider qualitative issues such as organizational objectives, the state of the economy and corporate culture. Final accounts are just one part of the quantitative analysis required to give an accurate appraisal of the firm’s financial position. Budgeting is an important consideration for the daily operation of a business, while investment appraisal assesses the financial gains on growth and expansion plans. So, the importance of any single financial statement in strategic planning and analysis should be handled with prudence.

Exercise Question 3. 4. 9 Satine Enterprise Ltd.

- Slides: 81