Understanding Business Drivers Taking the mystery out of

Understanding Business Drivers – Taking the mystery out of Accounting. . . And much more to come …. Presented by John Petty, FCPA, FCA Client Director, Pitcher Partners 0417 367 951 john@pettypresentations. com. au And Yvette Pietsch, FCA Partner, Taxation & Business Advisory Pitcher Partners (02) 9221 2099 ypietsch@pitcher-nsw. com. au

P&L Statement Balance Sheet

Session outcomes • List the three key financial reports • Detail what the key financial reports do and do not tell you, limitations and when to use • Latest Information reporting trends

[Statement")

The Key Financial Reports • The Profit and Loss Statement (P & L) [Statement of Financial Performance] • The Balance Sheet (BS) [Statement of Financial Position] • The Cash Flow Statement (CFS) [Statement of Cash Flow]

‘Statement of Financial Performance’ Displays: • Profit")

Profit and Loss Statement (P & L) ‘Statement of Financial Performance’ Displays: • Profit or Loss for period (one or other) Does not display: • Cash flow for period • Cash position • Funds available for distribution Monthly does not record reality or performance

Profit & Loss Statement Sales xxx Less: Cost Of Goods Sold Opening Stock Add: Purchases Less: Closing Stock xx xxx = Gross Profit (GP) xxx Less: Business Expenses NET PROFIT before Tax xxx

Balance Sheet ‘Statement of Financial Position’ Displays: • Assets and liabilities & net worth • Short term and long term indebtedness Does not display: • Market value of assets or business as total • Intangible assets • Off Balance Sheet financing of assets Monthly does not record reality or performance

Balance Sheet – Narrative Format Assets Current xxx Non-Current xxx Total Assets xxx Less: Liabilities Current xxx Non-Current xxx Total Liabilities xxx Net Assets

Balance Sheet --- ‘T’ Account format What the Funds have been invested in Current Assets Cash on Hand Accounts Receivable Stock Prepaid Expenses Non Current Assets Plant and Equipment Motor Vehicle Goodwill How the Business is financed Current Liabilities Bank Overdraft Accounts Payable Accrued Expenses Non Current Liabilities Loans Proprietorship Share Capital Retained Profits

Cash Flow statement Displays: • Cash flow from operations generated in period • Cash flow from borrowings • Cash flow from sale of assets (selling the farm) {HISTORICAL} Does not display: • Future cash flow position

Cash flow statement Cash Flows from Operating Activities Receipts from customers Payments to suppliers xxx Income taxes paid xxx xxx Cash Flows from Investing Activities Payments for Property, Plant & Equipment Proceeds from sale of PPE xxx Cash Flows from Financing Activities Proceeds from borrowings xxx Repayments of borrowings xxx

RATIO ANALYSIS q Profitability q Liquidity q Efficiency q Financial q Shareholder value q Other non financial

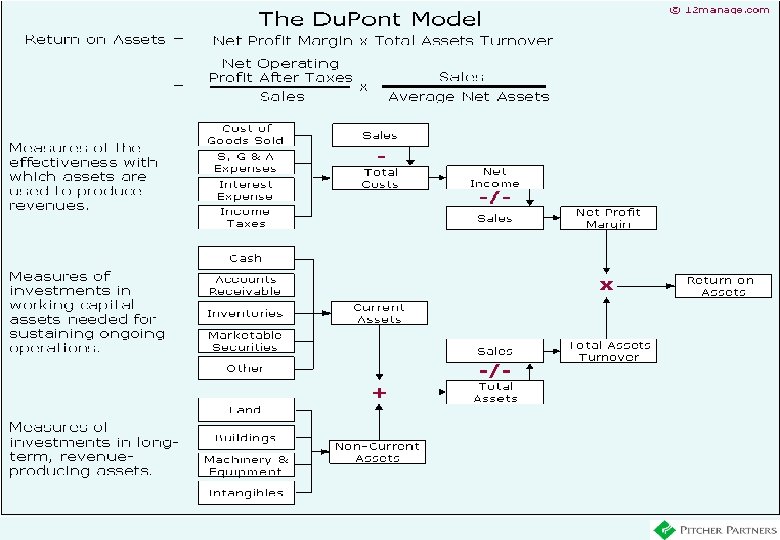

PROFITABILITY RATIOS Gross Profit Ratio % Gross Profit Sales X 100 Return on Investment Pre Tax Profit Net Profit Ratio % Owners Equity X 100 Net Profit Sales X 100 Operating Expense Ratio % Expense Item Sales X 100

LIQUIDITY RATIOS Current Ratio Current Assets Current Liabilities Interest Cover Net Profit + Interest Expense Quick Asset Ratio Interest Expense Current Assets - Stock Current Liabilities - Bank O/Draft Gearing / Debt to Equity Ratio Total Liabilities Owners Equity

Average Stock x 365 Cost of Sales Days to")

EFFICIENCY RATIOS Stock Turnover (days) Average Stock x 365 Cost of Sales Days to Collect Debtors Average Debtors x 365 Total Credit Sales Average Days to convert stock to cash Stock Turnover + Days to collect debtors

SHAREHOLDER VALUE RATIOS ROSF Ratio EPS Net profit Shareholder funds Per share NTA Net tangible assets PE Ratio Share selling price Earnings per Share Dividend per share Dividend earned per share

OTHER NON FINANCIAL RATIOS Sales per employee Total Sales No of employees R & D Per $ of sales Assets per employee

COGS Average stock Days/debtors ratio Trade debtors")

WORKING CAPITAL RATIOS Average stock turnover (days) COGS Average stock Days/debtors ratio Trade debtors Working capital ratio Average Daily sales Current assets Current liabilities Liquid ratio Quick assets Quick liabilities

Value has shifted from Tangible to Intangible Assets Percentage of market value related to … Intangible Assets 38% 62% 85% Tangible Assets 62% 1982 38% 1992 15% 2000

Value has shifted from Tangible to Intangible Assets Percentage of market value related to … Intangible Assets 85% The Intellectual Capital Model: Human Capital (the skills & knowledge, culture and loyalty of our people) Structural Capital (patents, processes, databases, networks, recipes, formulas, etc) Tangible Assets 15% 2000 Customer Capital (relationships with customers and suppliers)

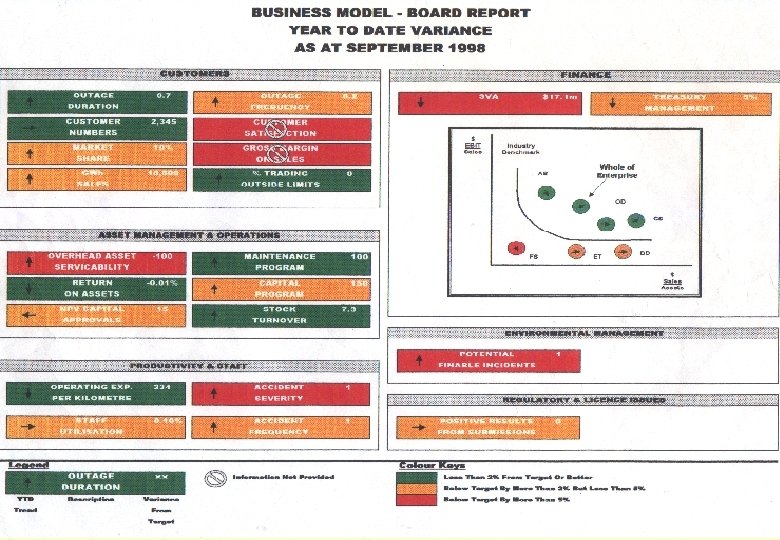

Strategic Business Management 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 STRATEGIC BUDGETING – ROLLING FORECASTS BALANCED SCORECARD / CORPORATE METRICS SCORECARD TRIPLE BOTTOM LINE REPORTING AT OR Moving TOWARDS ONE DAY REPORTING REPORT ON A PAGE (ROAP) ENHANCED CAPITAL AND REDUCED OPERATING SPEND FOCUS STRATEGIC REVENUE MANAGEMENT & PRICING TARGET PRICING & TARGET COSTING: Manufacturing to a Price TOTAL LIFE CYCLE COSTING / STEWARDSHIP FULL PRODUCT/SERVICE COSTS TOTAL WORKING CAPITAL MANAGEMENT PROCESS MAPPING / BUSINESS PROCESS REENGINEERING BENCHMARKING – Internal and External CUSTOMER PROFITABILITY ANALYSIS ) CUBE MANAGEMENT ) CHANNEL MANAGEMENT ) ACTIVITY BASED COSTING / MANAGEMENT ) NEW TRANSFER PRICING MODELS eg. PURCHASER - PROVIDER ROLE SERVICE LEVEL AGREEMENTS / EXPENSE REDUCTION ANALYSIS MANAGING & ACCOUNTING FOR QUALITY EVA / SVA / MVA / VBM KNOWLEDGE MANAGEMENT REAL OPTIONS ANALYSIS : STRATEGIC PREDICTIVE ANALYSIS Score: … / 23 SLAM DUNK!

NEW BUDGET FOCUS/APPROACH: ‘ROLLING FORECASTS’ 2 1 Jan 4 1 July 30 June 6 X Quarterly Rests The 90 day Deliverables 6 X Quarterly Rests Bye Budgeting… “The annual budget is dead. Long live the rolling forecast. ” Annie Gurton, International Management Magazine

ODR focuses on condensing the monthly management reporting cycle so")

ONE DAY REPORTING (ODR) ODR focuses on condensing the monthly management reporting cycle so that it can be completed within one working day with the appropriate reports disseminated to management [UPSTREAM & DOWNSTREAM]. It challenges existing practices that have taken anywhere between a couple of days and a few weeks to one that effectively completes the reporting process within an eight hour timeframe. DAY 50 THE 8 Hour REPORT THE 4 PM REPORT Then days 2 and 3 are used for management action.

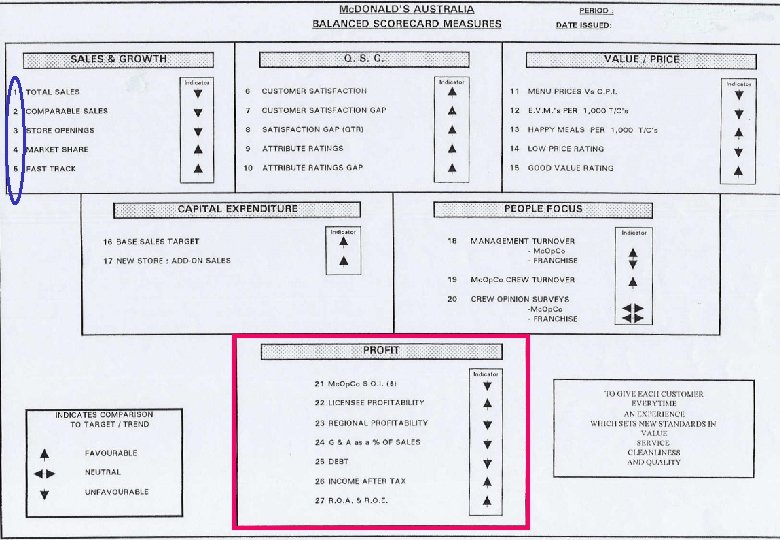

THE BALANCED SCORECARD FINANCIAL INTERNAL BUSINESS PROCESSES CUSTOMER LEARNING & GROWTH

SOMETHINGS MISSING: THE MOST VALUABLE ASSET FINANCIAL CUSTOMER LEARNING & GROWTH INTERNAL BUSINESS PROCESSES HRM/ PEOPLE

TRIPLE BOTTOM LINE REPORTING: Looking for balance FINANCIAL SOCIAL / COMMUNITY ENVIRONMENTAL

TOWARDS THE SEVEN SCORES OF SUCCESS: THE FULL PICTURE CUSTOMER LEARNING & GROWTH SOCIAL / COMMUNITY FINANCIAL HRM/ PEOPLE INTERNAL BUSINESS PROCESSES ENVIRONMENTAL

TOWARDS THE SEVEN SCORES OF SUCCESS: THE FULL PICTURE CUSTOMER LEARNING & GROWTH SOCIAL / COMMUNITY FINANCIAL HRM/ PEOPLE INTERNAL BUSINESS PROCESSES ENVIRONMENTAL

- Slides: 31