Types of Loan Pricing Costplus loan pricing Price

������������ Fair Pricing (2) ����������� Economic")

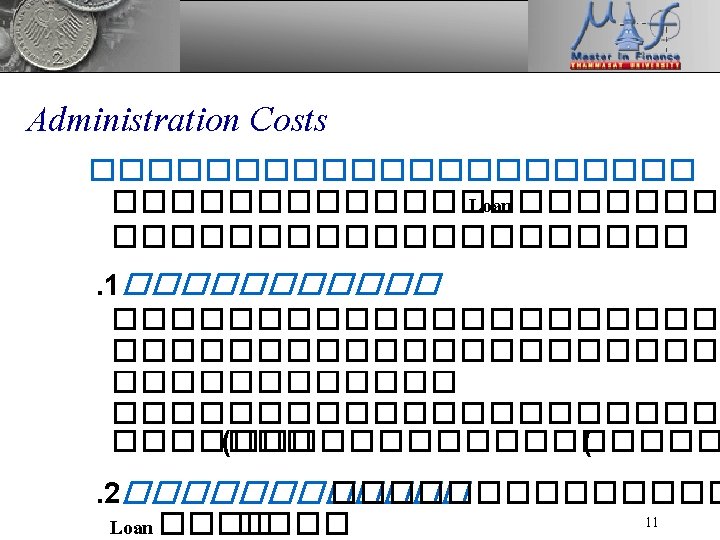

= Administration Costs + Risk-Based Spread 10")

Expected Loss Charges (2) Hurdle Rate ��� Quoted Rate (����������� (")

Expected Loss Charges ����� (1)Exposure at Default (EAD) (2) Recovery")

Exposure at")

������������ Loan ��� Counter-party ���� (2)")

Funding Costs Uses of Fund ��� Loan = Credit Asset")

���� Kd = Cost of Debt T = Tax")

")

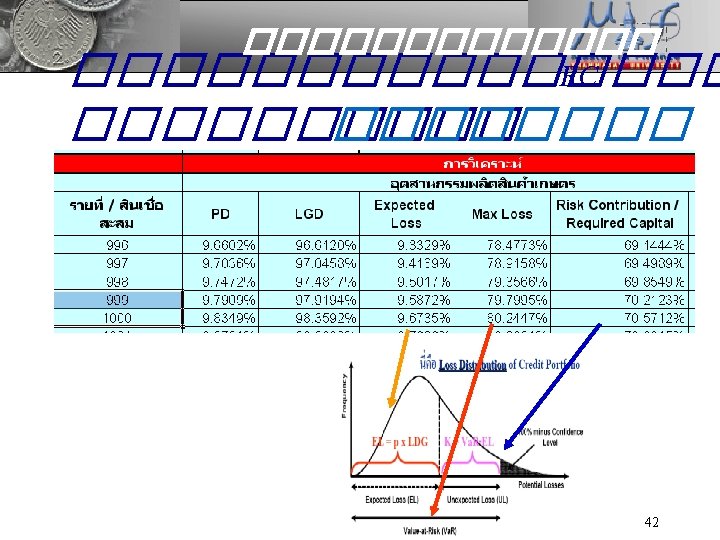

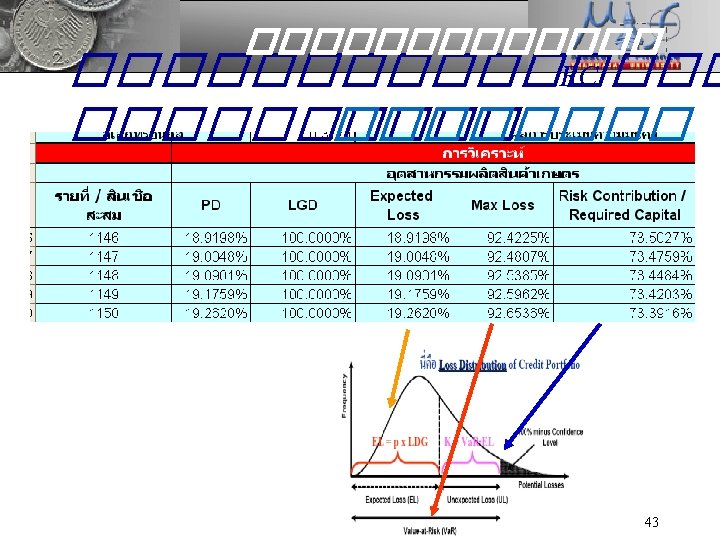

IVa. R ������ Credit Va. R ���������������� Credit")

* 2. Analytical RC")

����� Asset Value Model ��������� Arvanitis")

x Deposit Rate} =")

- Slides: 49

Types of Loan Pricing Cost-plus loan pricing ��������� ��. ������������ Price Leadership Model Below-Prime Market Pricing (The Markup Model) ������������� ��� ��. ������ interbank ����� Risked-based loan pricing 3

������� (2( Risk-Based Pricing �� ���� ��� (1) ������������ Fair Pricing (2) ����������� Economic Capital (EC) (3) ����������� RAROC (Risk-adjusted Return on Capital) (4)����������� Credit Risk Portfolio Management (5) 6

���������� ������ Risk-Based Loan Pricing ����� “Pricing is Based on Counter-party’s Risk Level. ” Level. 9

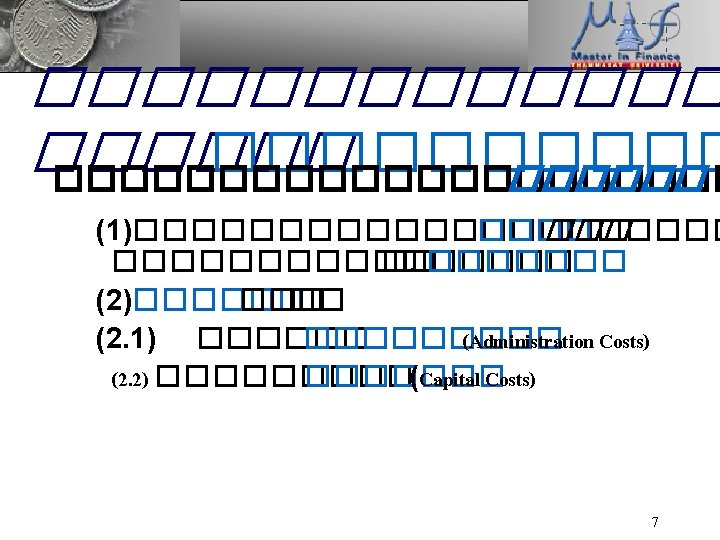

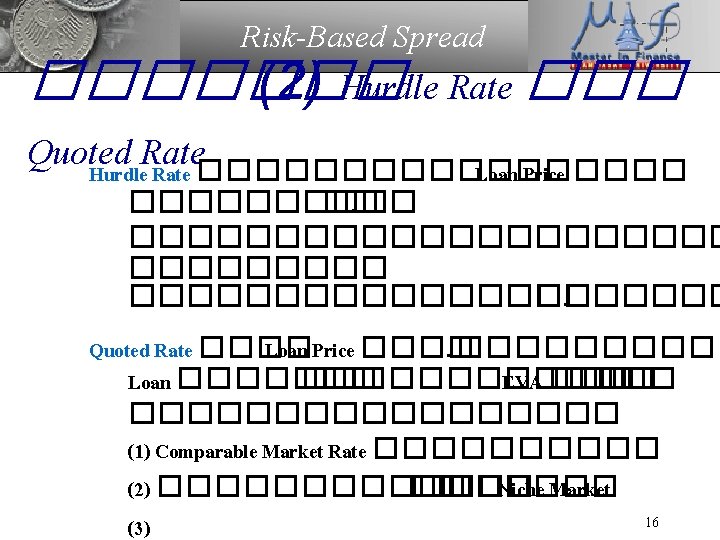

����� Lending Rate (Given Rating) = Administration Costs + Risk-Based Spread 10

Risk-Based Spread ����� (1)Expected Loss Charges (2) Hurdle Rate ��� Quoted Rate (����������� ( (3) Funding Costs 12

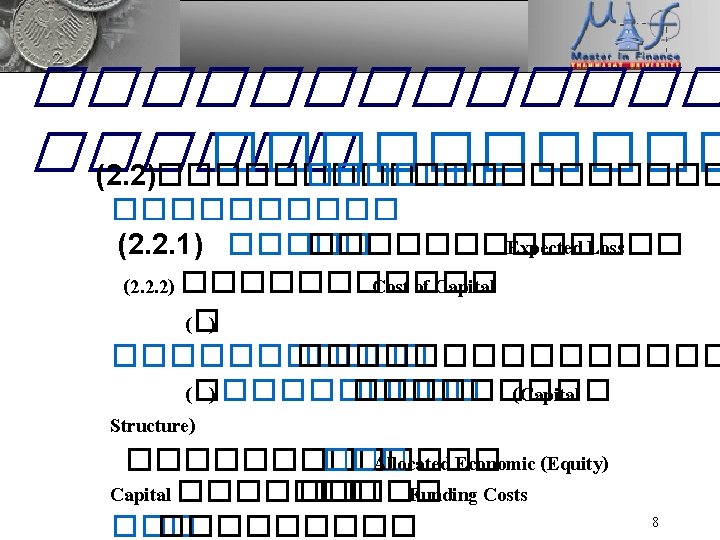

Risk-Based Spread ������� (1) Expected Loss Charges ����� (1)Exposure at Default (EAD) (2) Recovery Rate (RR) (3) Probability of Default (PD) ������ Credit Rating Expected Loss Charges = PD x { EAD x (1 -RR) } Note: LGD = Loss Given Default = PD x { EAD x LGD } 13

Risk-Based Spread ���� Expected Loss Charges ������ SMEs ������ 1 �� (1) Exposure at Default (EAD) = 1 ������� (2) Loss Given Default (LFD) = 1. 1282% (3) Probability of Default (PD) = 0. 1118% Expected Loss Charges = 0. 001118 x { 1 ���� x 0. 011282 } = 12. 62 ��� 14

Risk-Based Spread ����� Expected Loss Charges ������� (1) ������������ Loan ��� Counter-party ���� (2) ������������ Credit Portfolio ����� Default Correlation ���� Concentration 15

Risk-Based Spread ������� (3) Funding Costs Uses of Fund ��� Loan = Credit Asset ������ Funding ��� Sources of Fund = Debt ������� Long-Termed Bonds + Allocated Economic Equity Capital Providers �������� Required Rates of Return ������������ Required Rates of Return ��� Capital Providers ������� Costs of Fund ��� ��. 17

Risk-Based Spread Funding Costs (K) ���� Kd = Cost of Debt T = Tax Rate Ke = Cost of Equity DE = Debt-to-Allocated Equity Ratio ��� Loan ����� 18

Risk-Based Spread Funding Costs �������� �Funding Costs* = {EC x Ke} + {(1 -EC) x Deposit Rate} * ������ WACC ����������� Deposits ��� Equity Capital ����� 1 �������� WACC ��� Ke ����� ��. ���� Unlevered Firm ���� ��. ������ Funding Cost������ Capital Cost ������� Long. Term Debt 19

Credit Risk Portfolio Model ������ Economic Capital ��� Loan Portfolio ��. ����� � ����� Loan ������� 21

����� Economic Capital Allocation 1. Bottom-Up Approach ���� Va. R ���� Loan �������� ��. ����� Allocated EC { Loan j } = Regulatory Capital { Loan j } 2. Top-Down Approach ��. ����� EC ��� Loan Portfolio ����� Internal Credit Risk Portfolio Model ����������� Loan 23

���� Bottom-Up Approach ����� ��. ��� Allocated EC { Loan j } = Regulatory Capital { Loan j } �������� ������ BIS II 24

������ Bottom-Up Approach ����� ��. ������ SMEs ����� Credit Rating ����� 1 ������� Risk Asset = Risk. Weight (Given Rating) x Asset. Size = 100% x 1 ���� = 1 ������� Minimum Capital-to-Risk Asset = 8. 50% ����� Capital = 8. 50% x Risk Asset = 8. 50% x 1 ���� = 85, 000 ������� Loan ���� 1 ������������ EC = 85, 000 ��� Debt = 915, 000 ��� 25

����� Concentration Risk 27

���� Top-Down Approach ��. ����� EC ��� Loan Portfolio ������ Credit Risk Portfolio Model ����������� Loan ������� ��. ����� Internal Model ����� ��. �� Internal Credit Risk Portfolio Model �� ����� 29

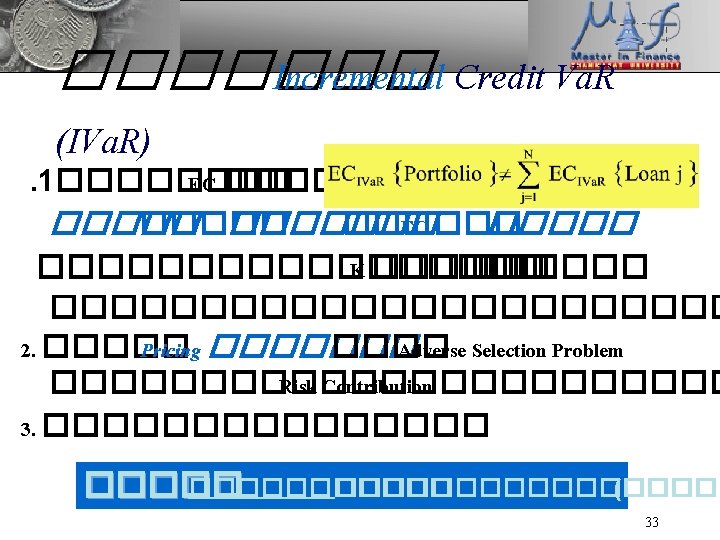

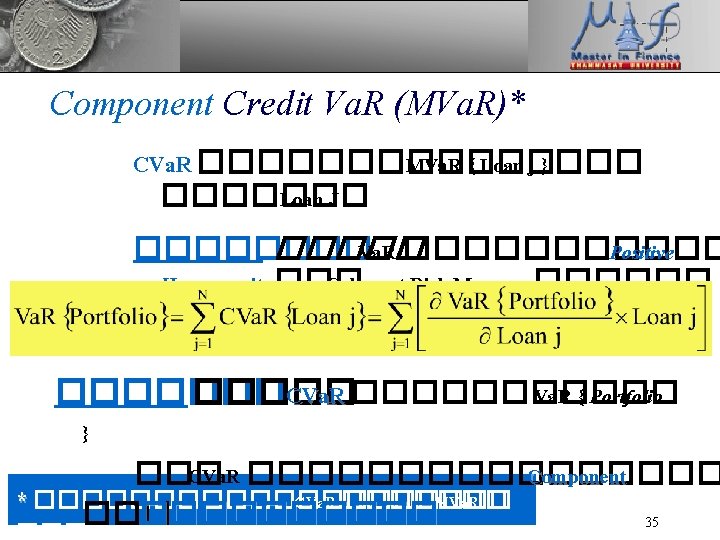

������������� EC { Loan j } ����������� Loan Portfolio �������� ��. �� Loan j ������ (Risk Contribution) Contribution ��������� 2 ���. 1 Incremental Credit Va. R 2. Marginal Credit Va. R ��� Component Credit Va. R 30

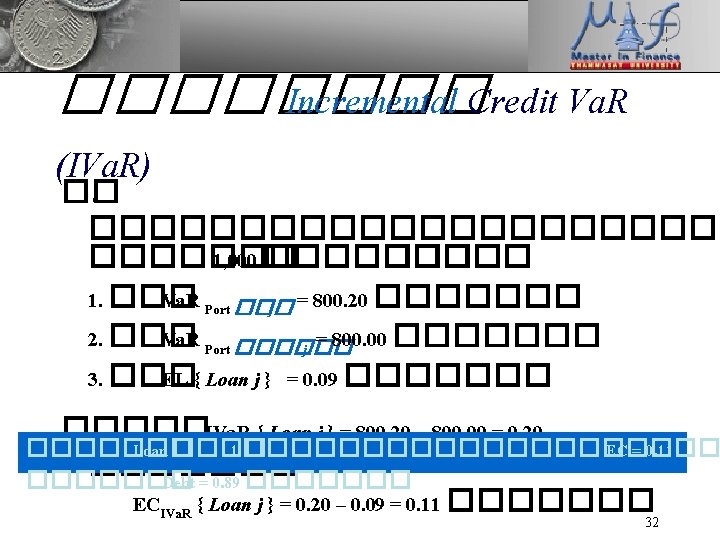

Incremental Credit Va. R (IVa. R) IVa. R ������ Credit Va. R ���������������� Credit Portfolio ���� Loan �������� EC ��� IVa. R { Loan j } = Va. R Port ��� j - Va. R Port ������ j ECIVa. R { Loan j } = IVa. R { Loan j } – EL { Loan j } 31

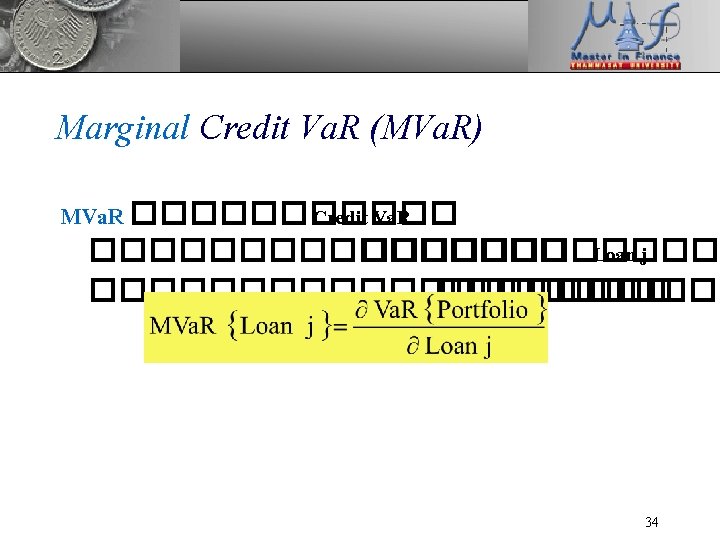

����� MVa. R ��� CVa. R ����� Economic Capital Allocation ����� 36

���������� Capital ������ Assumptions ��� ��. �� Internal Credit Risk Portfolio Model ����� 37

�������� Internal Model ������ . 1 Monte-Carlo Based Risk Contribution (RC)* 2. Analytical RC ��������� * ��� RC ��� EC { Loan j } ������������� Contribution ��� 38

������� Distribution ��� Portfolio Loan Loss ������� Smooth Function ���� 1. Va. R { Portfolio } ������� Smooth Function ��� Loan j 2. Derivatives ������� 39

������� � * * Gourieroux et al. , Sensitivity analysis of value at risk, Journal of Empirical Finance 7, 225 -245. 40

������ . 1 Monte-Carlo Based Risk Contribution (RC) ����� Asset Value Model ��������� Arvanitis and Gregory, 2001, Credit: The Complete Guide to Pricing, Hedging and Risk Management, RISK Publication, London, pp. 90 -98. 2. Analytical RC ������ Credit. Risk+ Model ���������� Tasche, Capital Allocation with Credit. Risk+ 41

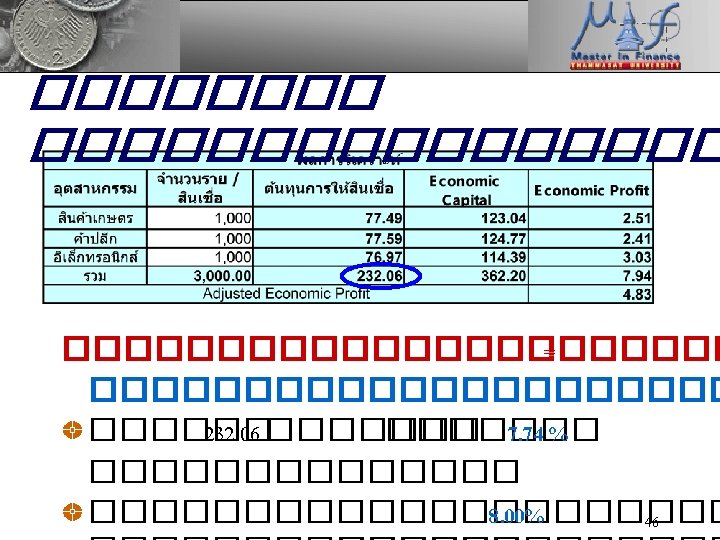

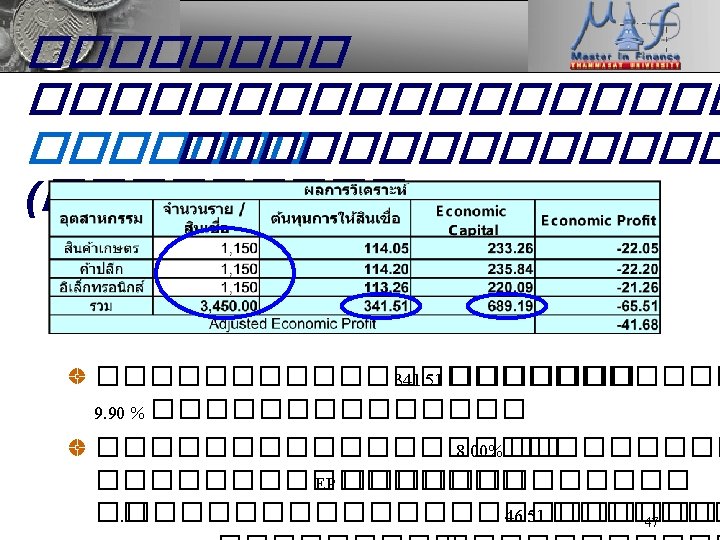

���� Funding Costs = {EC x Ke} + {(1 -EC) x Deposit Rate} = (0. 0896% x 8. 24%) + {(1 -0. 0896%) x 2. 27%} = 2. 2753% (������� 1) 44

�������������� = Expected Loss + Operating Costs + Funding Costs = 0. 0013% + 3. 66% + 2. 2753%} = 5. 9369% 45