Turning Resistance into Compliance Evidence from a longitudinal

, Resisters: Ø Actively resist the")

suggest that the perception of fairness is important for")

- Slides: 34

Turning Resistance into Compliance: Evidence from a longitudinal study of tax scheme investors Tina Murphy Centre for Tax System Integrity 6 th June 2005

Today’s talk Ø The dispute between the ATO and tax scheme investors Ø Can apply the lessons learned here to taxpayers caught or prosecuted for serious non-compliance Ø 2002 and 2004 survey: tracked changes in attitudes over time

Case Study: Mass marketed schemes Ø In 1996, ATO noticed increase in number of taxpayers involved in schemes Ø Increase in $ being claimed: Ø $54 m in 93/94 to $1 b + in 97/98

Problem with schemes Ø When ATO analysed the arrangements: Ø Commercial nature may have been OK Ø But were concerned with the way they were structured and financed Ø Investments largely funded through tax deductions Ø Little private capital at risk Ø In 1998, took action against 42000 investors Ø Saw it as a way of discouraging future marketing and investment in schemes Ø ATO went back 6 years and penalised those who invested as early as 1992

Investor reaction Ø Investors argued their accountants / financial planners sold schemes as legitimate investments Ø Resented the implication they were ‘tax cheats’ Ø Disappointed with the lack of consultation Ø In 1998/99 thousands of complaints made to the Ombudsman Ø Fighting funds set up Ø Majority refused to pay up – more than 50% still had not paid in 2002 (despite interest accumulating on debts) Ø Matter referred to a Parliamentary Senate Committee in 2000

Ø Without a doubt some of the investors would have been sophisticated taxpayers who knew what they were doing (but majority blindly followed advice of the marketers) Ø More than likely a lot of myths and propaganda about the ATO were being developed by the power players involved in schemes Ø This led to the ATO being put on the defensive about the approach they took

Our past research Ø Conducted Interviews and 2002 Survey: Ø Investors more resistant than general population Ø Measured through Val Braithwaite’s Motivational Posture of ‘Resistance’ Ø 55% of taxpayers in general population score high on measure of resistance Ø 87% of investors in 2002 survey were found to be resisters (coupled with refusal to pay their tax debts makes them a difficult group to manage)

What characterises a Resister? Ø According to Braithwaite (2003), Resisters: Ø Actively resist the self-regulatory system Ø Likely to view ATO with antagonism Ø See ATO as trying to catch taxpayers out rather than trying to help them Ø Believe people should take a stand against the ATO (may involve avoiding their tax obligations or being uncooperative) Ø So in some respects, this posture highlights taxpayers who may be a challenge for the ATO to manage (but good news is that this group can be turned around—unlike those who disengage from the system)

Why were so many Resistant? Ø Was it just the fact that they had tax debts they didn’t want to pay? Ø Was it more than just the money? Ø Was it something about the type of person they were? Ø Was it to do with the ATO’s approach to handling the matter?

2001 Interview Study Ø In initial exploratory interviews: Ø 30 investors interviewed Ø Kept referring to how they felt they had been treated by the ATO Ø Felt poorly treated by ATO Ø Letters rude and legalistic Ø Felt the ATO’s handling of schemes was unfair Ø Felt the ATO initially saw them all as tax cheats Ø Upset they hadn’t been consulted Ø Disliked the idea that interest was charged going back 6 years Ø Felt the wealthy got away with investing in these schemes earlier Ø Led me to procedural justice literature

Procedural Justice Ø “Concerns the perceived fairness of the procedures involved in decision-making and the perceived treatment one receives from the decision maker” (Tyler, 1990) Ø People’s reactions to experiences with authorities have been found to be rooted in their evaluations of the fairness of procedures used Ø If procedures seen to be fair, will be more likely to trust that authority, will see authority status as more legitimate, and be more inclined to accept decisions (even if outcomes are unfavourable) Ø People found to challenge authority if they believe the procedures are unfair Ø This pattern of results found in many different regulatory contexts (policing, workplaces, court system, tax, environment, etc)

Important point to note Ø Procedural justice theory does NOT suggest that punishment should not be used! Ø In fact, it suggests that punishment should be used if appropriate Ø Some people have also misinterpreted CTSI’s work in saying that we don’t believe in punishment. This is NOT true Ø It is the way in which this punishment is implemented that is important to consider

2002 National Survey Study Ø 2001 interview study suggested that procedural justice was an important element in investors’ reactions to ATO (Murphy, 2003). Ø But study conducted on investors in Kalgoorlie – perhaps a particularly resistant group? ? Ø In 2002, conducted a national survey on 6, 000 scheme investors (2, 292 responded) Ø Those who were more resistant were more likely to feel they were treated in a procedurally unfair way Ø Also less likely to trust the ATO and more likely to question ATO’s legitimacy (Murphy, 2004)

Present Study Ø Shortly after collecting survey data in 2002, ATO announced settlement offer to scheme investors Ø I had attitudinal measures from before settlement offer (gave me opportunity to study changes in attitudes after offer made) Ø Conducted follow-up survey in 2004 (contacted 1250 investors, 659 participated)

Findings Ø Interested in: Ø Investors who were resisters in 2002 and 2004 (resister group) – N=289 – 44% continued to resist Ø Investors who were resisters in 2002 but NOT in 2004 (non-resister group) – N=125 – 19% had change of heart Ø Why was it that some people continued to hold resistant views while others became less resistant over time? Ø Compared the 2 groups on a number of measures

Demographics Measure Group Mean SD Difference Age Non-resister Resister 49. 91 50. 97 8. 75 8. 66 No Income Non-resister Resister 55. 03 55. 93 1. 67 49, 717 65, 296 0. 43 0. 40 No Education Tax debt Eligible for offer 83. 42 78. 36 Non-resister 5. 94 Resister 5. 74 Non-resister 47, 286 Resister 56, 829 Non-resister 1. 13 Resister 1. 12 No No No

Compliance Behaviour Ø Investors asked whether they thought their scheme-related experience had affected their taxpaying behaviour in a negative way Ø Resisters affected significantly more so

Compliance Behaviour cont’d Ø Taxpayers asked to expand how it was affected: Ø I now try to avoid paying tax as much as possible Ø I no longer declare all my income Ø I now use the tax system in a negative way to recoup my losses Ø I am now more defiant towards the ATO Ø I now look for ways to purposefully cheat the tax system Ø I now look for many ways to recoup my losses Ø Resisters Mean = 2. 20 vs Non-resisters Mean = 1. 80 over 6 items (scores out of 5; higher number means more non-compliance)

Compliance Behaviour cont’d Ø 2002 evasion behaviour assessed and 2004 evasion behaviour assessed (eg. a) did they fail to lodge tax return; b) did they not declare cash income; c) did they make illegitimate deductions; d) did they refuse to pay back scheme tax debt) Ø Resisters and Non-resisters did not differ at Time 1 (2002) Ø But did differ at Time 2 (2004) – resisters more non-compliant Ø 99% of cash income was declared by Non-resisters, only 65% declared by Resisters in 2004 (N = 19 and 62, respectively)

Changes in Attitudes Ø Explored changes over time for the following attitudes: ØPerceptions of procedural justice ØTrust in the ATO ØPerceived legitimacy of the ATO ØObligation to obey the ATO

Attitude changes - 2002 to 2004 Ø Proc. justice Ø Trust

Attitude changes - 2002 to 2004 Ø Legitimacy Ø Obligation to obey

Views on Settlement Offer Ø Outcome fairness Ø Procedural fairness

Views on Settlement Offer Ø Satisfaction ratings Ø Alleviated original concerns

Views on Settlement Offer Ø Offer allowed me to put matter behind me Ø Respect for ATO as a result

Summary of Findings Ø Those investors who became less resistant towards ATO after settlement offer: ØWere more likely to be compliant in 2004 (resisters were more non-compliant) ØWere more trusting of the ATO in 2004 ØSaw the ATO as more legitimate in 2004 ØWere more likely to feel settlement offer was handled in a procedurally fair manner

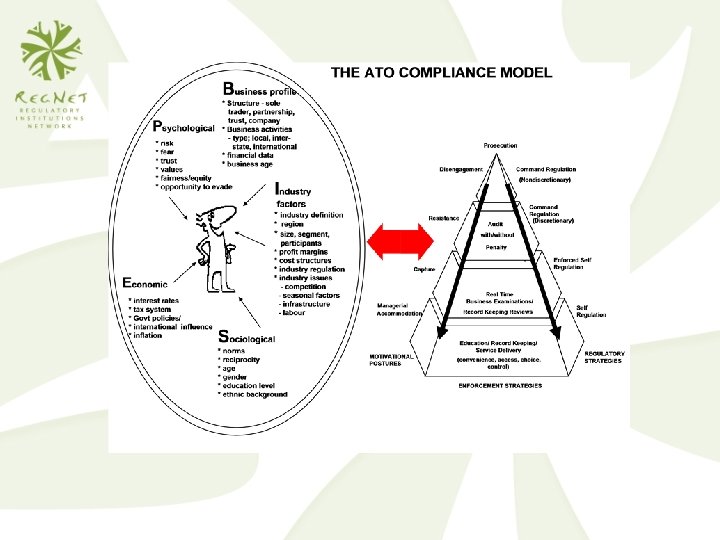

Implications of findings Ø Two points: Ø 1. Findings demonstrate that people’s motivational postures are fluid and changeable over time (one group who continued to be resistant (44%), other group resistant in 2002 but not 2004 (19%)) Ø 2. Way regulator handles a case can have serious ramifications for the way people view the regulator, as well as for their subsequent compliance behaviour. Ø These have implications for how the ATO interprets and uses the Compliance Model

Ø Some tempted to pigeon hole noncompliers as always having resistant or disengaged postures and treat them according to this view (i. e. hit them hard) Ø Reasoning behind this is that it will bring them into compliance and deter them from engaging in noncompliance in the future

Ø True that this strategy may deter Ø However, our research suggests that such a strategy can on occasion produce reactance and widespread resistance. Also, in such situations, an argument can be made for procedural unfairness (eg. Aggressive tone to letters, too long to make decision, no consultation, etc) ØWhich can lead to further non-compliance & defiance towards authorities ØMore costly in the long term

Ø Ayres & Braithwaite (1992) suggest that the perception of fairness is important for nurturing voluntary compliance Ø Start initial encounters with persuasion and explanation (educate them about why what they did was wrong – and keep them informed about decision processes) Ø Tyler’s (1990) work in context of policing and justice systems finds that people can handle negative outcomes if they believe the procedures used were fair and respectful.

Conclusion Ø Deterrence is important and the law is important. ØEg. Important to prosecute people who deserve to be prosecuted. Ø Without deterrence and the possibility of punishment, non-compliance may get out of hand. Ø However, the manner in which the law is administered, and perceived by the public, is just as important.

Conclusion cont’d Ø For a regulatory system to work effectively, regulators need to manage both the application of law and punishment, as well as how the public may react to it. Ø Be proactive beforehand rather than reactive after the event in developing an effective, fair and respectful enforcement strategy; Ø This applies to people who may have made an innocent mistake on their tax returns all the way up to those who have committed a serious form of non-compliance and need to be prosecuted. Ø If regulators do both of these things well, they will be able to turn some resisters into long-term compliers.

Thank you