TRIPS pharmaceutical strategies Global local pharmaceutical markets Pharmaceutical

TRIPS • & pharmaceutical strategies

Global & local pharmaceutical markets § Pharmaceutical industry is one of the largest industries in the world and lies in second place after the weapons trade. § The estimated volume of Pharmaceutical sales worldwide in 2012 at about 1. 02 tr. dollars § The Middle East sales is representing 3%

Global Market Size USD billion +7% +8% 1016 732 418 2000 2007 2012

The Global & Regional trends to 2016 Significant differences in per capita spending will remain 2016 Pharmaceutical Spend Per Capita and Population ANNUAL PER CAPITA DRUG SPEND US$ U. S. $892 Pop. 326 Mn 900 800 700 600 500 400 300 200 Japan $644 Pop. 124 Mn Canada $420 Pop. 36 Mn EU 5 $375 Pop. 320 Mn South Korea $323 Pop. 50 Mn Rest of Europe $321 Pop. 105 Mn Brazil $180 Pop. 201 Mn Russia $179 Pop. 140 Mn China $121 Pop. 1, 349 Mn Pharmerging Tier 3 $96 Pop. 1, 012 Mn India $33 Pop. 1, 292 Mn 100 0 POPULATION The pharmerging definition : Rank markets on the basis of anticipated added value to the total pharma market Source: IMS Market Prognosis, (audited and unaudited data) May 2012; Economic Intelligence Unit, Jan 2012

Exp. Per capita- Egypt 2012 Value: by L. E 295 150 72 0. 22 1953 12. 8 1984 2002 2009 2012

• Tier 1: China Expected to add $40 bn. & to become")

Pharmerging markets(#21) • Tier 1: China Expected to add $40 bn. & to become the world’s third-largest pharmaceutical market on 2013. • Tier 2: Brazil, Russia and India. Expected to add $5 -15 bn. on 2013. • Tier 3: Fast Followers(13 countries) Expected to add $1 -5 bn. On 2013 They are: Venezuela, Poland, Argentina, Turkey, Mexico, Vietnam, South Africa, Thailand, Indonesia, Romania, Egypt, Pakistan and Ukraine. While each market is unique, they are all complex, dynamic and subject to rapid change • 4 more new markets added to Tier 3 which are Algeria, Colombia, Nigeria and Saudi Arabia (#17)

Pharmerging markets IMS increases Pharmerging countries to 21 as healthcare improvement becomes global priority Tier 1&2 China Brazil Russia India Tier 3 Algeria (new) Argentina Colombia (new) Egypt Indonesia Mexico Nigeria (new) Pakistan Poland Romania Saudi Arabia (new) South Africa Thailand Turkey Ukraine Venezuela Vietnam Pharmerging countries Tier 1 & 2 Countries Tier 3 Countries New Tier 4 Countries Source. : IMS Market prognosis 2012 -2016 September update, LC $

GLOBAL SPENDING US$BN Global Spending and Estimated Net Spending 60 -65 55 -65 530540 55 -65 175185 Brands 555580 Generics 2011 300320 10 -20 100110 Other Estimated Net Spending Adjustment 100110 Brands Generics 2016 15 -20 115140 Other Estimated Net Spending • Discounts and rebates are expected to increase for branded products through 2016. • Off-invoice discounts for generics will continue to grow as companies compete with each other with increasing intensity. • Off-invoice discounts and rebates in 2011 are estimated to be $130 -140 Bn, rising to $180190 Bn by 2016. • The U. S. , France and Germany have recently increased government-mandated rebates, while other countries, including Italy and Canada, have banned some rebates, joining many other countries around the world with more transparent pricing systems. Source: IMS Institute for Healthcare Informatics, IMS Market Prognosis, May 2012

Pharmerging markets Large pharma sales grew by 50% in 4 years while local companies more than doubled * Large pharma MS of 32% compared to 71% in top 9 mature markets Value Market share in Pharmerging markets 2007 $232 Bn Value Market share in Pharmerging markets 2011 $220 Bn $356 Bn $508 Bn CAGR Growth 2008 -2011 5% 18% 14% 10% 9% Small companies * Large pharma includes 18 companies Local companies Reg&Small Multinationals Midsize Multinationals Large global pharma Local companies are growing faster and now have a greater market share than Large pharma Source: IMS MIDAS MAT 06 -2012, IMS corporation segmentation analysis

Pharmerging markets Local players are very present across pharmerging countries, particularly in China, Indonesia and Egypt Total market share by type of corporation Algeria Argentina Brazil China Colombia Egypt India Indonesia Mexico Pakistan Poland Romania Russia S. Africa Saudi Arabia Thailand Turkey Venezuela Vietnam Germany USA Small companies Local companies Regional &Small Multinational Mid-size Multinational Top Global Pharma China has the most fragmented market with more than 3, 000 small and local companies 100% Source: IMS Midas MAT 06’ 2012, IMS internal analysis on company categorisation, market segmentation & LIC

Prospects for MENA Region & Egypt Local companies benefit from more than half of the MENA market being generic Segment Value by Country 12% 2% 1% 6% 16% 2% 18% 3% 8% 10% 17% 2% 3% 29% 8% 1% 8% 2% 10% 52% 48% 38% 40% 2% 34% 2% 57% 61% 60% 54% 61% 52% Value Market Share Volume Market Share Segment Volume by Country 49% 55% 59% 42% 30% UAE 27% Saudi Arabia 22% Egypt Others 32% 27% 18% 56% 34% 18% Jordan Morocco Tunisia Unbranded Generics UAE Branded Generics Saudi Arabia Egypt Jordan Morocco Tunisia Original Brands Source: IMS MIDAS June 2012, Licensing Data, Rx bound

MENA region most important markets USD billion UAE 1. 05 KSA 4. 1 Egypt 3. 7 Pharmaceutical Market Size , 2012 Morocco 1. 3 Algeria 2. 6 Source : IMS Prognosis

Growth Forecast CAGR 2012 – 2016 Percent Source: IMS Prognosis UAE 10. 9% Egypt 13. 8% Algeria 8. 2% Morocco 7. 4% KSA 6. 2%

")

Billions Egypt Pharmaceutical Market Growth Value - Private Sector (IMS ® 2006 : 2012) 25 Gr. 18. 3% 20 17. 1 18. 9 14. 9 15 10 22. 4 9. 3 11. 0 12. 6 5 0 2006 2007 2008 * Average Growth Rate about 18. 3% 2009 2010 2011 2012

LE Sales Year 2012")

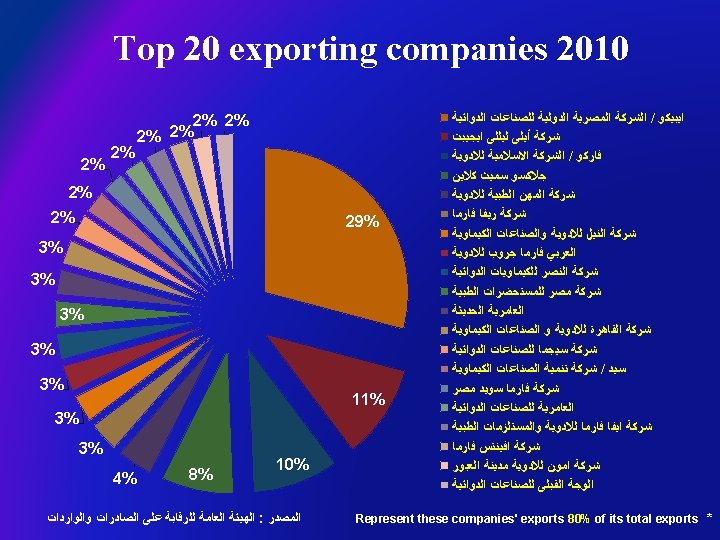

Prospects for Egypt Top 20 Corporations – Year 2012 (Value) LE Sales Year 2012 Egypt Pharmacy market 22, 359, 583, 473 GLAXOSMITHKLINE* NOVARTIS PHARCO* SANOFI AVENTIS* EIPICO* AMOUN PHARM. CO. * PFIZER* EVA PHARMA SIGMA* M. S. D. * MEDICAL UNION PHA* SERVIER* MERCK SERONO ABBOTT* MULTIAPEX PHARM. HIKMA PLC* ASTRAZENECA* JOHNSON E JOHNSON* MARCYRL* SEDICO* Total Displayed (20) Total Others (742) 2, 036, 023, 287 1, 923, 484, 870 1, 332, 408, 110 1, 236, 934, 086 1, 110, 336, 574 925, 874, 544 812, 088, 648 619, 160, 882 563, 266, 955 490, 422, 653 471, 767, 343 431, 822, 281 397, 493, 812 372, 265, 257 327, 472, 099 322, 462, 959 317, 059, 063 295, 079, 100 293, 372, 443 288, 196, 956 14, 566, 991, 922 7, 792, 591, 551 % Growth on Previous period 18. 3% 21. 6% 17. 4% 17. 1% 15. 7% 17. 2% 10. 1% 22. 9% 12. 9% 20. 6% 32. 8% 15. 6% 3. 9% 19. 3% 30. 7% 13. 2% 30. 8% 17. 4% 28. 3% 41. 6% 12. 3% 18. 5% 17. 9% % share 100. 0% 9. 1% 8. 6% 6. 0% 5. 5% 5. 0% 4. 1% 3. 6% 2. 8% 2. 5% 2. 2% 2. 1% 1. 9% 1. 8% 1. 7% 1. 5% 1. 4% 1. 3% 65. 1% 34. 9%

")

Egypt Market facts. . 2012 • Actively selling product trade names (Over 100 units/year) are 4, 877 • Imported & locally manufactured drugs Units Value Imported drugs 8% 18% Locally produced drugs 92% 82% • Market structure Multinational Units Value 42% 56% PRIVATE 48% 40% Public state 10% 4% 38% value If we consider the imported by MN Co's

prices: Public Price < EGP 50")

Egypt Market facts. . 2012 • Packs (presentations) prices: Public Price < EGP 50 Public Price EGP 50 – 100 No. of packs MKT share 9, 739 81% 632 10% ü No. of packs including all product forms regardless of sales • Average prices: Public state Private Multinational Av. Public Price EGP 4. 5 9. 4 15. 5

Pharmaceutical Industry in Egypt • No. of pharmaceutical factories in Egypt about 124 factories licensed of MOH. The private sector 106 plants, the public sector 10 factories and the multinational sector 8 factories • No. of pharmaceutical factories under construction about 84 factories arise according to GMP (export)

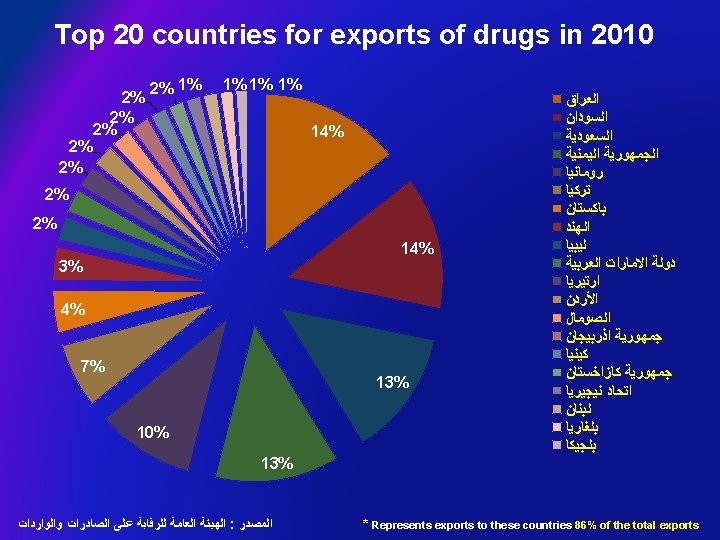

EXPORT!!! § Volume of export of Egyptian pharmaceutical companies in 2011 is very limited compared to other pharmerging countries Egypt Export 0. 25 Import 0. 40 Balance - 0. 15 Jordan Export 0. 64 Import 0. 32 Balance 0. 32 India Export 10. 32 Import 0. 70 Balance 9. 62 US$ billion

Medical sector’s Export Overview Value : Million L. E. 2007 Exports of Medicines Exports of Medical Equipment Exports of Cosmetics Total Exports 2008 2009 2010 2011 GR. Rate % 876. 9 1017. 4 1144. 2 1325. 3 1428 7. 7 883. 6 948. 2 1157. 2 1529. 2 1654 8. 2 1075 1150 1529 15 4611 4. 65 1285 1392 2835. 5 3115. 6 3586. 4 4246. 2 Source : Egyptian Export Council

Scientific Research In Egypt Proactive plans to support the clinical research and drug development What is achieved in research works in drug development (possible and impossible) Statistical probabilities for success (SPS) that help in decision making SPS Achievement 1: 10000 Innovations & breakthrough (NCEs) 1: 1000 1: 100 1: 2 (50%) Me-Too research work parent daughters Developmental research works (New drug delivery system, New indications and new combination) Herbal and natural medicines Off-Patent (Generic medicines)

(General Agreement on Tariffs and Trade) üWTO (1995) (The")

ﻭﺗﺎﺭﻳﺦ ﺗﻌﺮﻳﻔﺎﺕ üGATT (1948) (General Agreement on Tariffs and Trade) üWTO (1995) (The World Trade Organization ) ü TRIPS (1995) (Trade Related Aspects of Intellectual Property Rights )

ﺣﻘﺎﺋﻖ ﺍﻟﺪﻭﺍﺀ ﺳﻮﻕ • Actively selling product trade names (Over 100 units/year)")

( ﻭﺃﺮﻗﺎﻡ ﺍﻟﻤﺼﺮﻱ)ﺣﻘﺎﺋﻖ ﺍﻟﺪﻭﺍﺀ ﺳﻮﻕ • Actively selling product trade names (Over 100 units/year) are 4, 877) • Imported & locally manufactured drugs Units Value Imported drugs 8% 18% Locally produced drugs 92% 82% • Market structure Multinational Units Value 42% 56% PRIVATE 48% 40% Public state 10% 4% Source: IMS 38% value If we consider the imported by MN Co's

Thank You Dr. MOHY HAFEZ Chairman & CEO, DELTA PHARMA Bio Founder, Chairman & (CEO) of DELTA PHARMA (1997 -2010). President of Pharmaceutical & Health committee at Investors Association "TRIA" & Board of Trustees 10 th Ramadan City & General union Egyptian investors. President of Medical industry & Health committee at General union Egyptian investors. Board Member of industrial chamber of pharmaceuticals, cosmetics, & appliances "PCA". Board member of Export Council for Medical Industries. Member of Higher Committee for Health, Sharkia. Board Member of IMC Steering Committee & Pharmaceutical Egypt council Ministry of trade and industry. Vice President of Industrial investors' general syndicate (IIGS) Institutional investors. Lecturer of material of good practices for the pharmaceutical industry (c. GMP) in faculty of pharmacy (Zagazig, 6 October) University. Founder and Board Member of 10 th Ramadan University. Faculty of pharmacy council member at (Ain Shams, Zagazig) University. Faculty of pharmacy council member at Modern University for Science & Technology (MTI), Cairo. Member of Industrial Liaison Committee for British University in Egypt "BUE". Member of International Academy of Engineering, Moscow – Russia. Board member of other civil associations.

- Slides: 45