TOPIC LESSON TITLE Topic 5 Operations Management Breakeven

TOPIC: LESSON TITLE: Topic 5: Operations Management Break-even Analysis COMPETENCY FOCUS: Key Skills (L 5): you will be able to develop your numeracy skills to calculate financial transactions of a business and to interpret financial data. Learning Objectives By the end of the lesson, you should be able to… To calculate break even using the correct formulae (Gui-Reg) To calculate break-even using the graphical method.

Introduction to Break Even • To make a profit, revenue must be higher than costs. • It is where Costs = Revenue within a business. • New businesses should always conduct a breakeven analysis to find the break-even point. This tells them how much they need to sell to break even.

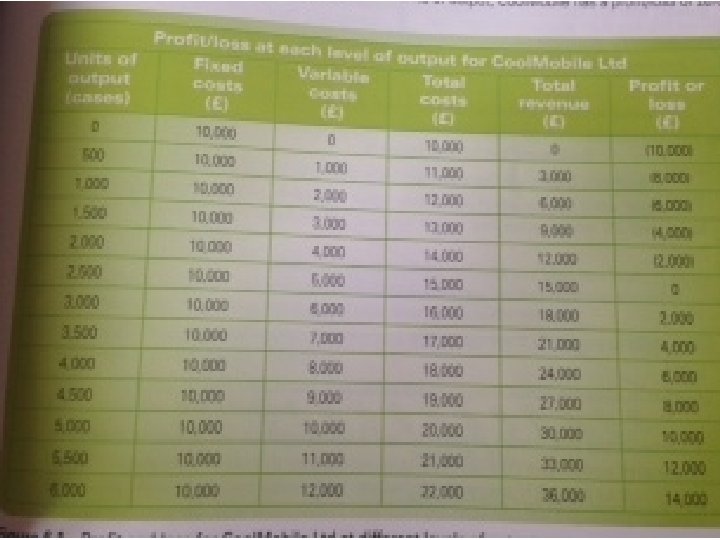

Is the business breaking even? Cool. Mobile Ltd makes fun cases for mobile phones. Each case sells for £ 6. Fixed costs per year are £ 10, 000 and variable costs are £ 2 per case (unit). The maximum cases that the company can make in 1 year is 6000. Use this data to construct a clear table.

0 500 1, 000 1,")

Is the business breaking even? Units of Output (Cases) 0 500 1, 000 1, 500 2, 000 6, 000 Fixed Costs (£) Variable Costs (£) Total Revenue (£) Profit or loss?

![Test your knowledge… 1) What does the term break-even mean? [2] 2) Why is](http://slidetodoc.com/presentation_image_h/2c4ac7761552b20553da3a718b6461d3/image-6.jpg "Test your knowledge… 1) What does the term break-even mean? [2] 2) Why is")

Test your knowledge… 1) What does the term break-even mean? [2] 2) Why is it important for a business to calculate their break-even? [2] 3) What does break-even analysis show a business? [1] [Max 5 marks]

?")

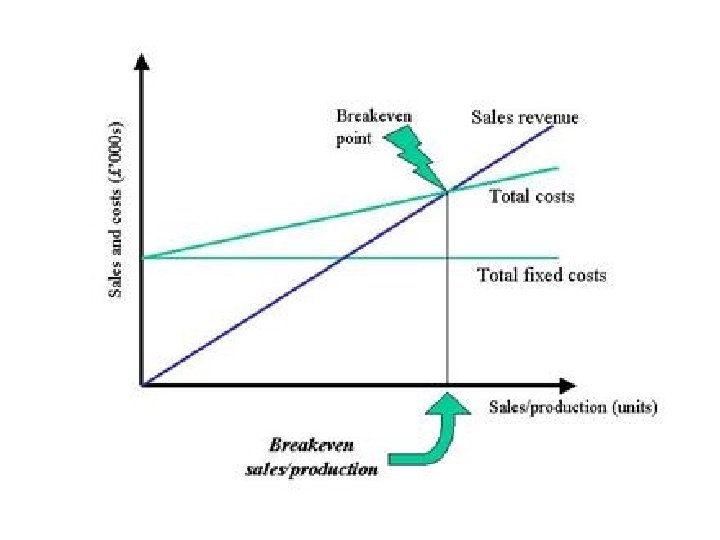

Where is the Breakeven Point (BEP)?

BREAK-EVEN POINT • There are two ways to calculate the")

Calculating Break-Even Point (BEP) BREAK-EVEN POINT • There are two ways to calculate the break(BEP)= the point at even point (BEP): which revenue equals expenditure! – USING A FORMULA (CONTRIBUTION METHOD) – PRODUCING A BREAK EVEN CHART.

This involves a two part calculation: • Selling Price per unit")

CONTRIBUTION METHOD (FORMULA) This involves a two part calculation: • Selling Price per unit – Variable Cost Per Unit = Contribution (Towards Fixed Costs). AND • Fixed Costs / Contribution = Break-even Point.

BREAK-EVEN POINT • There are two ways to calculate the")

Calculating Break-Even Point (BEP) BREAK-EVEN POINT • There are two ways to calculate the break(BEP)= the point at even point (BEP): which revenue equals expenditure! – USING A FORMULA (CONTRIBUTION METHOD) – PRODUCING A BREAK EVEN CHART.

CALUCULATING BREAKEVEN POINT USING GRAPH Break-even graphs show costs and revenue plotted against output Output goes on the horizontal axis (starting from 0) Costs and revenue both go on the vertical axis STEP 1: draw you axis, label ‘y’ axis ‘costs/revenue’ & label ‘x’ axis with ‘No of units sold’ STEP 2: Draw your fixed costs line STEP 3: Add your total costs line (calculate the total costs for two points on graph & draw best-fit line)

CALUCULATING BREAKEVEN POINT USING GRAPH STEP 4: Draw your sales revenue line (again calculate this for two points on graph and draw in best-fit line) STEP 5: Draw & label your BE point where your total costs and sales revenue lines cross over.

Key Words Margin of Safety: The amount by which demand can fall before a business makes a loss.

Fixed costs 1,")

Task - Evans Cricket Bats Ltd Output (No of cricket bats) Fixed costs 1, 000 £ 40, 000 2, 000 3, 000 Variable costs Total costs Sales revenue £ 40, 000 £ 100, 000 4, 000 Fixed costs = £ 40, 000 Variable costs £ 2 per cricket bat Total costs = Fixed + variable costs Sales revenue = Selling price x output Cricket bats sold for £ 35 each £ 140, 000

Stage 1: calculating costs & revenue Output (No of Fixed Variable Total costs Sales revenue cricket bats) costs 1, 000 £ 40, 000 £ 20, 000 £ 60, 000 £ 35, 000 2, 000 £ 40, 000 £ 80, 000 £ 70, 000 3, 000 £ 40, 000 £ 60, 000 £ 105, 000 4, 000 £ 40, 000 £ 80, 000 £ 120, 000 £ 140, 000 Fixed costs = £ 40, 000 Variable costs £ 2 per cricket bat Total costs = Fixed + variable costs Sales revenue = Selling price x output Cricket bats sold for £ 35 each

Turn your paper so it is LANDSCAPE")

Stage 2: DRAW the graph Costs (£) Turn your paper so it is LANDSCAPE and copy this. 1000 2000 3000 Output (No of cricket bats) 4000

Stage 3: Showing costs on a graph. Insert fixed costs. 1000 2000")

Costs (£) Stage 3: Showing costs on a graph. Insert fixed costs. 1000 2000 3000 Output (No of cricket bats) 4000

")

Stage 3: Showing costs on a graph. Calculate total costs. Fixed costs Costs (£) Variable costs Total costs 1000 2000 3000 Output (No of cricket bats) 4000

Stage 4: Showing revenue on a graph Now add revenue to your graph. Fixed costs Costs (£) Variable costs Total costs 1000 2000 3000 Output (No of cricket bats) 4000

Stage 4: Showing revenue on a graph Now add revenue to your graph. . Costs and sales revenue (£) Fixed costs Variable costs Total costs 1000 2000 3000 Output (No of cricket bats) 4000 Sales revenue

Stage 5: revealing the break-even pointline Break-even is point is where revenue crosses the total costs line. Costs and sales revenue (£) Fixed costs Variable costs Total costs 1000 2000 3000 Output (No of cricket bats) 4000 Sales revenue

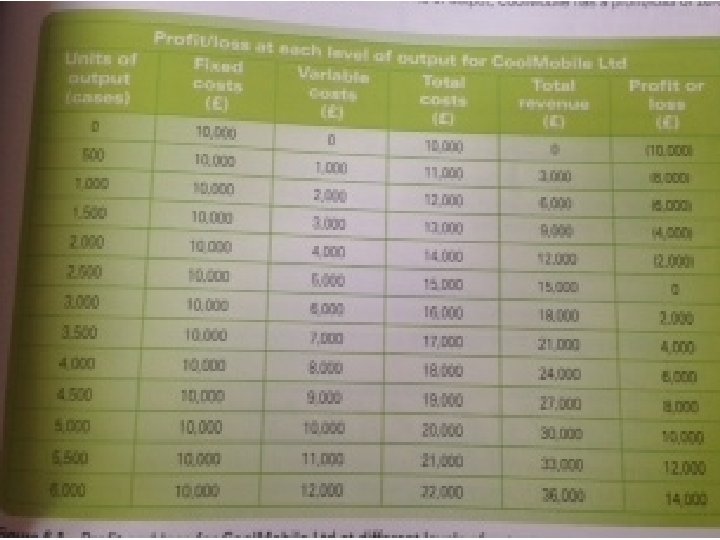

Is the business breaking even? Cool. Mobile Ltd makes fun cases for mobile phones. Each case sells for £ 6. Fixed costs per year are £ 10, 000 and variable costs are £ 2 per case (unit). The maximum cases that the company can make in 1 year is 6000. Use this data to construct a clear table.

0 500 1, 000 1,")

Is the business breaking even? Units of Output (Cases) 0 500 1, 000 1, 500 2, 000 6, 000 Fixed Costs (£) Variable Costs (£) Total Revenue (£) Profit or loss?

Is the business breaking even? Use your table to construct a break-even graph. This can be done using graph paper.

TASK 1 Complete task on pg. 68/69.

![TASK 2 Complete activities in the break-even workbook. [40 mins]](http://slidetodoc.com/presentation_image_h/2c4ac7761552b20553da3a718b6461d3/image-28.jpg "TASK 2 Complete activities in the break-even workbook. [40 mins]")

TASK 2 Complete activities in the break-even workbook. [40 mins]

The Importance of Break-even - Helps a business make decisions about the business - Calculate the effect of a change in price - Calculates the effect of a change in costs - Estimates the level of output needed to cover costs - Provides evidence to the bank when applying for a loan.

The Limitations of Break-even It assumes that the firm can sell any quantity of the product at the current price. In practice the firm may need to reduce prices to sell at high levels of output. It assumes fixed costs never change - but as output increases the firm may need to buy more machines, get bigger premises, take on extra sales and administration staff. It assumes that all products are sold. This doesn’t always happen; some products may only be sold at lower prices or need to be thrown away.

Impact of changing cost or price on BEP What is the impact on the BEP if Cool. Mobile Ltd increase their selling price from £ 6 to £ 7 per unit? What is the impact on the BEP if Cool. Mobile reduced their variable costs from £ 2 to £ 1 per unit.

- Slides: 31