This presentation has been rated NDT Some material

This presentation has been rated N-DT – Some material may be unsuitable for Super Trump fans By the PPAA – The Power. Point Association of America

And the adventure begins National Credit Union Collections Association – March 2017

The Dwight Side From 2016 • Market conditions will calm and encourage businesses to hire • Growth in service sector jobs (over 70% of all jobs) will far exceed losses in other sectors such as energy • Wages will rise by 3% or more as competition for workers heat up • Payrolls will average 150 -175 k as job market tightens – erratic pattern • Unemployment rate will hit 4. 50%

The Dwight Side From 2016 • Auto sales will plateau but at a healthy rate • Consumers have binged on big ticket items and will shift more toward discretionary consumer goods • Services will remain strong • Higher wages and steady job growth will encourage spending

The Dwight Side From 2016 • Home price gains in high-priced areas will be limited due to mortgage rate rise • Overall activity will improve on continued rise in household formation • Demand for rentals a sign that households are “reforming”; a good omen for housing prospects longterm • Construction on single-family homes and apartments will move steadily higher • Housing Starts will hit 1. 3 million units annualized

The Dwight Side From 2016 • The lower price of oil will result in more spending on goods, big ticket and others – this will allow businesses to raise prices • Inflation of services running almost 3% • Wage growth will foster more spending and inflation expectations will rise • Core CPI will rise to 2. 5%; Fed’s preferred measure will hit 2. 00%

The Dwight Side From 2016 • Fed funds will end 2016 at 1. 50% (Yes, I know I’m out there on this one) • Remember, at 1. 50% “real” rate will still be negative • Bond market will be under pressure, especially in second half of 2016 as leveraged accounts exit positions • Inflation will not rise sharply, but rising inflation expectations will cause bond investors to demand higher risk premium

Super President!

A third – Let’s get this party started!

A third – Why, God, why!!

A third – Let’s just hope this goes okay

The Trump Factor Trump plus Trump minus O u r

Retail Sales & Confidence — Confidence highest since 2001

Total Vehicle Sales Auto sales confirm plateau Units in millions annualized

Signs still pointing up • Year-over-year Retail Sales surge to 5. 6% as Consumer Confidence remains above historical norms • Auto sales hold steady at strong levels • ISM manufacturing and Non-manufacturing ISM post much better than expected gains • Trump plus – Progress on tax reform and regulatory reform boost consumer and business confidence • Trump minus – Lack of progress on reform drains confidence; trade war slams stocks and drives prices higher

Nonfarm Payrolls

Payroll Growth Job market remains healthy • Another very good report with a gain of 235 in NFP – average for past twelve months 200 k • Biggest jump in ten years in construction jobs – 58 k • Year-over-year wage gain up to 2. 8%. • Jobs outlook still positive for 2017 — I expect average monthly gains of 125 -150 k by end of year on tight labor market; wages will move higher • Trump plus – infrastructure job growth; business hiring on higher confidence • Trump minus – loss of jobs for producers of exports; harsh immigration policy limits job gains

(Apartment starts cause volatility) Units (thousands)")

Housing Starts — (January) (Apartment starts cause volatility) Units (thousands)

Home sales off to good start New Homes (thousands) Existing")

Home Sales — (January) Home sales off to good start New Homes (thousands) Existing Homes (millions)

Volatile but trending higher New Homes (thousands)")

New Home Sales — (January) Volatile but trending higher New Homes (thousands)

Existing Homes (millions)")

Home Inventories — Single Family New Homes (thousands) Existing Homes (millions)

Housing — current state • Beware median home prices – Almost all areas are up on year-over-year basis but at or below 2016 high • Lack of supply still a major factor in most markets • Biggest risk is rising rates in higher priced areas • Not a bubble, but price inflation coming to an end • Housing looks solid longer-term with big rental pool • Trump plus – Confidence • Trump negative – Tax reform phases out mortgage deduction; policy actions cause rising rates

What will happen to mortgage business? • Mortgage Bankers Association forecast • Based on mortgage rates slowly rising to 4. 50% by last quarter of 2017 (Billions) 2016 2017 Change Refis 990 484 -506 Purchase 901 1100 +199 Total 1891 1584 -397

CPI & Core CPI Year-over-year Headline CPI exceeds core rate

General outlook improves into 2017 but risks loom • Job growth should remain steady • Wage gains likely to become a big story in 2017 • Trump corporate tax cuts could boost business spending – but delays could drain optimism • Some regulatory relief also possible • Europe represents biggest non-Trump risk but conditions are improving

Too much debt? In billions 2003 2010 2016 Autos $625 $650 $1010 Credit cards $675 $750 $1071 Student loans $220 $650 $1190 Total $1, 520 $2, 050 $3, 271 Source: Federal Reserve Bank

Too much debt? In billions 2003 2008 2012 2016 Home mortgages $7, 600 $12, 100 $10, 800 $11, 800 Home equity $675 $895 $300 $575 Total $8, 275 $12, 995 $11, 100 $12, 375 Source: Federal Reserve Bank

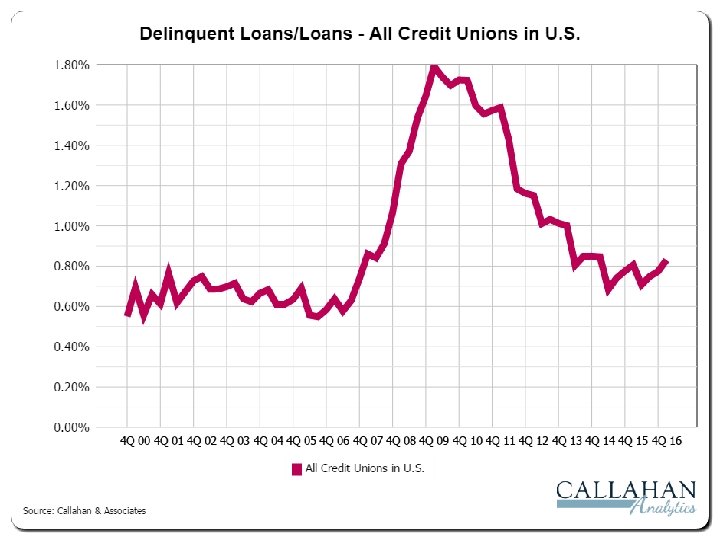

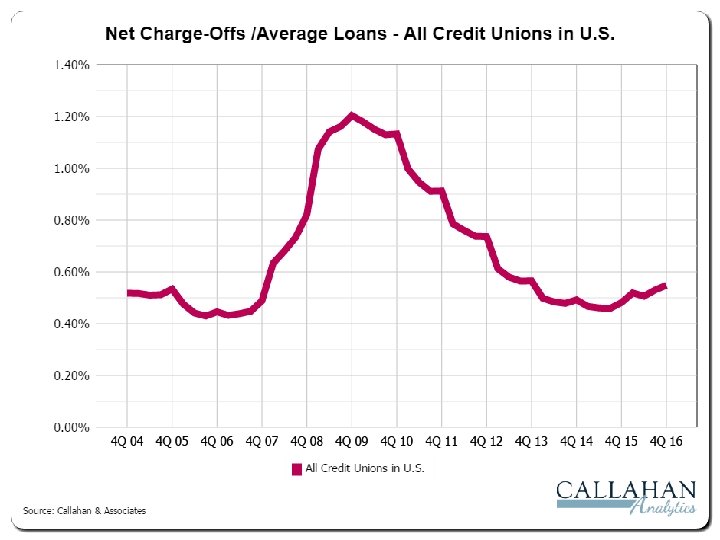

Is it too much? • Delinquencies and charge-offs in normal ranges especially for credit unions • Non-mortgage consumer debt not large enough to threaten financial system • Mortgage defaults and foreclosures low • Missing element for mortgage crisis repeat is securitization • Any debt is too much if you lose your job • Snap poll

")

Yields not drastically different (Dow up 3500 points)

As Roseanne Rosannadanna said, It’s always something

Always something • • • 2013 – EU on the brink with crisis in Crete and Greece – U. S. budget crisis 2014 – Ukraine – Ebola – Plunge in Oil 2015 – Severe winter – Another Greek crisis – August Chinese stock market meltdown 2016 – Chinese meltdown Part II – Brexit – Election 2017 ? ? ?

Potential sources of fear • China pokes back – Possible sharp devaluation, setting off tailspin in markets • Trump escalates trade war • Businesses sour on Trump and optimism fades • Core supporters turn against Trump and White House/Congress relationship crumbles • Or…. None of that, but European elections roil the markets

Interest Rate Forecast — Trump minus version

What could go right might actually go right • Corporate tax cut and regulatory relief boost business spending • Wages rise as jobs hard to fill • Trump makes only small trade changes – enough to declare victory before war starts • Individual tax cuts disappoint but not a dealbreaker • Inflation expectations rise but contained • Europe keeps it together one more year

Interest Rate Forecast — D. J. ’s Trump plus view

GDP UR")

Range of Expectations for 3/31/2018 (February 2017 Bloomberg poll — 82 economists) GDP UR CPI Fed Funds 2 -Year 10 -Year Low 1. 10% 3. 10% 1. 20% 0. 500. 75%. 90% 1. 35% Median 2. 40% 4. 50% 2. 30% 1. 251. 50% 1. 85% 2. 90% High 4. 60% 5. 80% 4. 00% 1. 752. 00% 2. 50% 3. 75%

Three Scenarios • Low rate view — Trump optimism fades; China threatens backlash; series of negative outcomes in European votes • Consensus — Optimism drives business growth; wages higher but contained; EU crisis avoided; moderate rise in rates; no global slowdown • Inflation Case — Monetarist case; wages rise more than expected; inflation expectations turn sharply higher; series of liquidations of major bond positions roil bond market

")

Fed Funds Scenarios (Rate is high end of Fed range)

Ten-year Note Scenarios

Things to remember • Economy will not turn on a dime – the stock market is not the economy • This Fed remains slave to the markets; decisions will be market risk based • The transition from the world we knew to the Trump world will not be easy • Bond volatility will accelerate as some risks come and go

More things to remember • We don’t know what Trump will be like as President, but assume what he Tweets is what you get • Risk/reward ratio is very high • Best approach for 2017 is to be optimistic but wary • Perhaps biggest surprise ahead will be a quiet and boring presidency

League Resources • Daily comment • Monthly packages on DJs Economix – Longer-term commentary – Economic data updates – Interest rate forecast – Usually available the second week of the month • Quarter CU Performance report • Ask us

- Slides: 46