The term royalty refers to the periodical payment

Ltd. Madras, entered into a collaboration agreement with Agro (U. K) Ltd.")

Ltd. : Quarter Sales 30 -9")

![• [1]. When the Royalties received is less than the minimum rent and](https://slidetodoc.com/presentation_image_h/fb5b0beae68d03ec981d6788b9356472/image-19.jpg "• [1]. When the Royalties received is less than the minimum rent and")

- Slides: 44

The term royalty refers to the periodical payment based on output or sale for the use of a specific asset or right like mine, copyright or patent to its owner. The person who make the payment to the owner of the asset in exchange for the right to use his asset is known as lessee and the owner of the asset to whom payment is made is known as landlord.

There are three types of royalties: l Mining royalty l Patent royalty l Copyright royalty

l Mining royalty: It is a periodical payment generally based on output , made by lessee of a mine or quarry to the lessor or the landlord (i. e, owner of the mine or quarry) l. Patent royalty: It is the periodical payment based on output , made by the lessee of a patent or patent right to be lessor or the patentee (i. e, the holder of the patent right) l. Copyright royalty: It is also the periodical payment based on sales , made by the lessee of a copyright (i. e the publisher) to the lessor (i. e. the author)

There are some special terms which generally are used in royalty agreements. The meaning of such terms must be clear to the reader. The special terms are: Landlord: -The persons who gives out his some special rights over something say mining rights or patent rights or copyrights, on lease to another person for a consideration is called the landlord, or lessor or patentee or an author. Lessee: -The person who takes out the special rights from its owner on lease for consideration is called lessee or patentor or publisher. Minimum rent or Dead rent: -It was been stipulated that in case of low output or low sales, a certain sum of money will be payable in any case-even if the royalties based on output or sales are lower. Implying thereby that the sum payable is the minimum amount or actual royalties whichever is higher. The minimum sum is known as minimum rent or deeds rent. E. g. if a the patentee, allows B to use his patent on a royalty of Rs. 2/unit. Produced subject to minimum of Rs. 10000 then incase the output is 7000 units; it will be Rs. 14000.

SHORTWORKING- The excess of minimum rent over actual royalty calculated on the basis of output or sales is termed as shortworking. Normally shortworking are during gestation period or due to abnormal working condition during the early periods of lease as the activity level is low in that period. RECOUPING SHORTWORKING- Most of times, along with the stipulated for a minimum rent, there is a condition that if actual royalties are less than the minimum rent, the excess paid will be recoverable out of any surplus that there may be over the minimum rent in subsequent years. The right of getting back the excess made by the lessee in earlier years is called the right of recoupment of shortworking. The right of recoupment of shortworking can be: Restricted (i. e. fixed): -Recoupment only in the first few years of the agreement. Unrestricted (i. e. floating): -Recoupment in the year/few years following the year in which the shortworking occur GROUND OR SYRFACE RENT- It is the fixed yearly or half yearly rent payable by the lessee to the landlord in addition to the minimum rent.

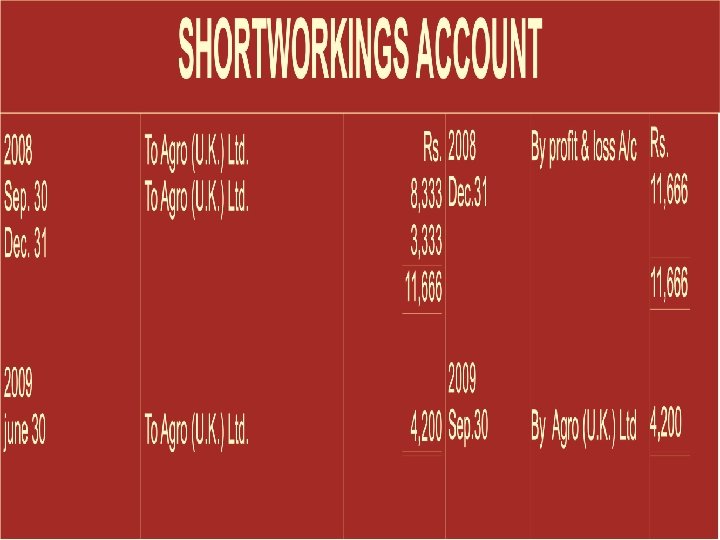

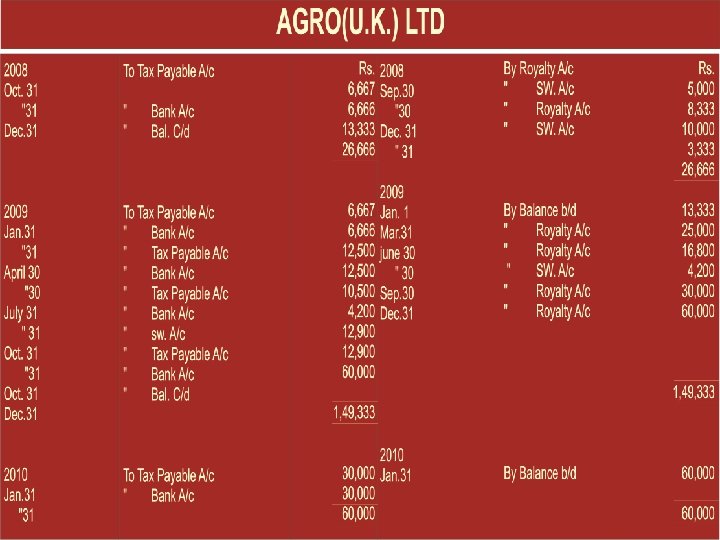

Agro (India) Ltd. Madras, entered into a collaboration agreement with Agro (U. K) Ltd. Birmingham, under which the former were to pay the latter, commencing with the date on which they started production , a royalty @ 5% of sales during each quarter of the calendar year, subject to deduction of tax in India (which may be assumed @ 50%) so however that the remittance in any such quarter should not be less than 500, the shortworking being recoupable from out of royalty payable in subsequent quarters during the same calendar year but not beyond.

Following are the sales figures of agro (India) Ltd. : Quarter Sales 30 -9 -2008 31 -12 -2008 31 -3 -2009 30 -6 -2009 30 -9 -2009 31 -12 -2009 Rs. 1, 000 2, 000 5, 000 3, 36, 000 12, 000 The production had begun on 1 -7 -2008, the rate of exchange may be taken at $1=13 -1/3 for remittance up to 6 -6 -2009 and thereafter at $=Rs 21. The remittance has been made in each case within one month from the end of the relevant quarters.

2008 Rs. 2008 5, 000 10, 000 Dec 31 2009 15, 000 2009 Mar 31 June 30 Sep 30 Dec 31 25, 000 16, 800 30, 000 60, 000 1, 31, 80 0 Dec 31 Sep 30 Dec 31 To Agro (U. K) Ltd To Agro (U. K) Rs By Profit & 15, 00 loss a/c 0 15, 00 By Profit & 0 loss a/c 1, 31, 800 1, 31,

GENERALLY MINIMUM RENT IS FIXED TAKING CONSIDERATION THE MINIMUM EXPECTED OUTPUT UNDER NORMAL CONDITIONS. NON- APPLICATION OF THE CONDITION OF MINIMUM RENT – In such a case the clause of minimum rent is not applied. Actual royalties will discharge all rental obligations. REDUCTION IN THE AMOUNT OF MINIMUM RENT – IF there is any clause in the agreement , regarding reduction in the amount of minimum rent , it can take the following form: Minimum rent is reduced proportionately to the length of the stoppage of work during the relevant year. Minimum rent can be reduced by a fixed percentage or by a fixed amount in the year of stoppage.

• On 1 st july, 2005, A obtained from B a lease of sum coal bearing land , terms buying a royalty of Rs. 2 per ton raised subject to a minimum rent of Rs. 9000 per annum with a right to recoup the shortworking over the first four years (up to 2008) of the lease. From the following details, prepare 1)royalty account 2)shortworking account 3)B’s account in the books of A year 2005 2006 2007 2008 2009 2010 sales (tons) 1500 2300 5000 6000 3600 4500 closing stock (tons) 500 400 700 800 600 500 in the event of strike the minimum rent would be taken prorata on the basis of actual period of working but in the event of lockout, the lessee would enjoy a concession in respect of minimum rent for 40% of the period of lockout.

Analytical table Year Production Royalty Minimum Rent Short Surplus Recouped working 2005 2000 4000 9000 5000 _ _ _ 9000 2006 2200 4400 9000 4600 _ _ _ 9000 2007 5300 10600 9000 _ 1600 _ 9000 2008 6100 12200 9000 _ 3200 2009 3400 6800 7500 2010 4400 8800 8400 700 _ _ 400 Not Recouped 1600 3200 _ _ Paid to Landlord 4800 9000 7500 _ 8800

2005 2006 2007 2008 2009 2010 To landlord a/c To landlord a/c 4000 2005 By P/L a/c 4000 4400 2006 By P/L a/c 4400 10600 2007 By P/L a/c 10600 12200 2008 BY P/L a/c 12200 6800 2009 BY P/L a/c 6800 To landlord a/c 8800 2010 BY P/L a/c 8800

2005 To Bank a/c 9000 2005 By Royalties a/c By Shortworking a/c 4000 5000 2006 To Bank a/c 9000 2006 By Royalties a/c By Shortworking a/c 4400 4600 2007 To Shortworking a/c To Bank a/c 1600 2007 By Royalties a/c 10600 To Bank a/c To Shortworking a/c 9000 2008 By Royalties a/c 12200 2009 To Bank a/c 7500 2009 By Royalties a/c By Shortworking a/c 6800 700 2010 To Bank a/c 8800 2010 By Royalties a/c 8800 2008 9000 3200

• [1]. When the Royalties received is less than the minimum rent and shortworkings are recoverable out of future years, the following entries will be made: [A] Lessee’s Account Dr. (with minimum rent) To Royalties Receivable Account (with actual royalties) To Shortworkings Suspense Account (with the difference) [B] Bank Account Dr. To Lessee’s Account [C] Royalties Receivable Account To P& L Account (with the amount received) Dr. (with the amt of royalties earned transferred)

• 2. When the royalties earned exceed the minimum rent and shortworkings are recovered, the entries are as follows : [A] Lessee’s Account Dr. ( with the amt of royalties earned) To Royalties Receivable Account [B] Shortworking suspense Account Dr. (with the amt of shortworking recovered) To Lessee’s Account [C] Bank Account Dr. (with the amt due received) To Lessee’s Account [D] Royalties Receivable Account Dr. ( with the amt of actual royalties earned) To P&L Account But if the shortworking is irrecoverable it should be transferred to P&L Account

• ILLUSTRATION Srikant had patented a new type of pocket transistor. On 1 -1 -2007, he granted Parker a license for 20 years to manufacture and sell the transistor on the following terms: (a) Parker to pay a royalty of Rs. 5 for each transistor manufactured and a further royalty of Rs. 3 for each transistor sold with a minimum rent of Rs. 8000 p. a. (b) If, in any year the royalties calculated on the transistors manufactured and sold be less than the minimum rent, Parker to have the right to recoup shortworkings out of the royalties in excess of the minimum rent during the two years immediately following, subject to a maximum amt of Rs. 2000 p. a. The no. of transistors manufactured for the first four years were as follows:

Year Manufactured Sold 2007 800 500 2008 1000 700 2009 2500 1500 2010 500 2000 All the payments were made by Parker on the due dates, Prepare

ANALYTICAL TABLE Year Royalty Minimum Short Surplus Short Workings Rent Workings not Recouped Paid to Landlord 2007 5500 8000 2500 _ _ 8000 2008 7100 8000 900 _ _ 8000 2009 17000 8000 _ 2000 9000 500 15000 2010 8500 8000 _ 500 400 8000 _ _

2007 To Royalties Receivable a/c To Shortworking Suspense a/c 5500 To Royalties Receivable a/c To Shortworking Suspense a/c 7100 2009 To Royalties Receivable a/c 2010 To Royalties Receivable a/c 2008 2007 By Bank a/c 8000 2008 By Bank a/c 8000 17000 2009 By Bank a/c By Shortworking Suspense a/c 2000 8500 2010 By Bank a/c By Shortworking Suspense a/c 8000 2500 900

2007 To P&L A/C 5500 2007 By Parker a/c 5500 2008 To P&L A/C 7100 2008 By Parker a/c 7100 2009 To P&L A/C 1700 2009 By Parker 0 a/c 17000 2010 To P&L A/C 8500 2010 By Parker a/c 8500

2007 To Bal c/d 2500 2007 By Parker a/c 2500 2008 To Bal c/d 3400 2008 By Bal b/d By Parker a/c 2500 900 2009 To Parker a/c To P&L a/c To Bal c/d 2000 2009 By Bal b/d 3400 2010 To P&L a/c To Parker a/c 400 500 2010 By Bal b/d 900 500 200

Nazrana or lease premium or goodwill means lump sum payment made by lessee in addition to royalty. In the books of lessee, the whole amt is debited to Nazrana a/c. In the books of lessor, the amt received as nazrana us credited to nazrana a/c.

l In case of lease of copyrights, the royalty agreement may contain a clause that the author should revise the book and give the revised manuscript to the publishers for publication within a stipulated period failing which the author should pay some compensation of damage to the publisher.

Professor Kundan Lal wrote a book and gave Kalyani Publishers the publishing rights on the following terms with effect from 1 -1 -2006: Royalties @ 10% on published price of the copies sold. Minimum payment of Rs. 60, 000 in the first year and Rs. 1, 000 per annum thereafter. Rights to deduct in the following two years any excess of minimum rent paid over actual royalties in any year. Revision of book by the author on request and to pay Rs. 6, 000 per month to Kalyani Publishers for ever month of delay after six months of request made by the publisher.

In the even of delay the condition of minimum amount payable was not to be applied. On 1 -1 -2009 request for revision was made and the revised manuscript was supplied by the author on 1 -11 -2009. Prepare ledger accounts in the books of the publisher based on the following information: - l Year 2006 2007 2008 2009 2010 Copies sold (number) 1500 4900 5000 4000 5000 Printed Price per copy (Rs. ) 200 250 250

Year Sales Royalties Min. Rent 2006 3, 000 30, 000 60, 000 30, 000 2007 9, 80, 000 98, 000 2008 12, 50, 00 0 10, 00 0 12, 50, 00 0 1, 25, 00 0 1, 00, 00 0 1, 00 0 -1, 00 0 2009 2010 Short- Surplus Working Recou ped Writ ten Off Carrie d Paymen t -- -- -- 60, 000 2, 000 -- -- 25, 00 0 -- -- 25, 000 -- 5, 00 0 2, 00 0 -- 30, 00 0 32, 00 0 2, 000 --- 1, 00, 0 00 76, 000 1, 25, 0 00

Notes : In the year 2009 as per agreement – l Condition of minimum rent is not applicable. l Royalty payable works out to be Rs. 1, 000. l But because of delay of four months in the submission of manuscript by the author, the publisher shall deduct Rs. 24, 000 (i. e. Rs. 6, 000 * 4). Hence, the net royalty payable is Rs. 76, 000.

2006 To Kundan Lal 30, 000 2006 By Profit & Loss A/c 2007 To Kundan Lal 2007 By Profit & Loss 98, 000 A/c 98, 000 2008 To Kundan Lal 1, 25, 000 2008 By Profit & Loss A/c 1, 25, 000 2009 To Kundan Lal 1, 000 2009 By Profit & Loss A/c 1, 000 1, 25, 000 2010 To Kundan Lal 2010 By Profit & Loss A/c 30, 000

2006 To Kundan Lal 30, 000 2006 To Kundan Lal 2007 To Balance b/d To Kundan Lal 2008 To Balance b/d 2009 To Balance b/d 30, 000 2007 2, 000 2008 32000 By Balance b/d 32, 000 By Kundan Lal By Profit & Loss A/c By Balance c/d By Profit & Loss A/c 25000 2000 2009 30, 000

24, 000 To Profit & Loss A/c 2, 40, 000 2009 By Kundan Lal 24, 000

2006 2007 To Bank A/c 60, 000 2006 By Royalties A/c By Shortworkings A/c 60, 000 1, 00 0 98, 000 2007 By Royalties A/c By Shortworkings A/c 1, 00 0 2008 2009 2010 To Bank A/c To Shortworkings A/c To Bank A/c To Damages Receivable A/c 30, 000 1, 00 0 25, 000 1, 25, 00 0 76, 000 24, 000 1, 000 2008 By Royalties A/c 1, 25, 000 2009 By Royalties A/c 1, 00 0 1, 000 000 2010 By Royalties A/c 1, 00,

l Sometimes, the terms of the original lease may empower the lessee to sublet a part of the lease to another person as a sub-lessee. The transfer of a part of the right held by the lessee to another lessee is sublessee. In such a case, the status of the original lessee will be two fold : as lessee paying royalties to the landlord and as sub-lessor receiving royalties from the sub-lessee. As lessee he maintains Royalties Payable Account, Shortworkings Account and Landlord’s Account and as sub-lessor he maintains Royalties Receivable Account, Shortworkings Suspense Account and Sublessee’s Account.

Dobson's Ltd. took a license for production of a foreign medicine from Johnson Ltd. at Royalty of Re. 1 per bottle produced. Dobson Ltd. issued a sub-license to Medico Ltd. on the Lasis of a Royalty payment of Rs. 1. 25 per bottle sold. Minimum Royalty payable by Medico Ltd. was fixed at Rs. 15, 000 per annum with a right to recoup shortworkings in the following year. From the given details prepare Royalties Receivable Account, Royalties Payable Account and Shortworkings Account in the books of Dobson's Ltd.

Dobson Ltd. Sales 1 st year 2 nd year 3 rd year Medico Ltd. 50, 000 Closing Production Stock 5, 000 10, 000 Closing Stock 2, 000 70, 000 8, 000 18, 000 4, 000 1, 000 10, 000 25, 000

Royalty receivable is to be calculated on the basis of number of bottles sold, so first number of bottles sold by Medico Ltd. is calculated to find out the amount of Royalties receivable. Number of bottles sold = Bottles produced + Opening Stock – Closing Stock Number of bottles sold in 1 st year = 10, 000 + Nil – 2, 000 = 8, 000 Number of bottles sold in 2 nd year = 18, 000 + 2, 000 – 4, 000 = 16, 000 Number of bottles sold in 3 rd year = 25, 000 + 4, 000 – 5, 000 = 24, 000 Royalties receivable in 1 st year on 8, 000 bottles @ Rs. 1. 25 per bottle = Rs. 10, 000 Royalties receivable in 2 nd year on 16, 000 bottles @ Rs. 1. 25 per bottle = Rs. 20, 000 Royalties receivable in 3 rd year on 24, 000 bottles @ Rs. 1. 25 per bottle =

1 st year To Profit & Loss A/c 2 nd year To Profit & Loss A/c 3 rd year 10, 000 20, 000 1 st year 2 nd year By Medico Ltd. 30, 000 To Profit & Loss A/c 10, 000 20, 000 3 rd year By Medico Ltd.

Royalty payable in case of sub-lease is calculated on the basis of total output : so first total output is calculated by adding the production of Dobson's Ltd. and Medico Ltd. Production of Dobson Ltd. Production of Total (Sales + Closing Stock – Operating Stock) Medico Ltd. Production 1 st year 50, 000 + 5, 000 - Nil = 55, 000 10, 000 65, 000 2 nd year 70, 000 + 8, 000 - 5, 000 = 73, 000 18, 000 91, 000 3 rd year 1, 000 + 10, 000 – 8, 000 = 1, 02, 000 25, 000 1, 27, 000 Royalties payable in 1 st year on 65, 000 bottles @ Re. 1 = Rs. 65, 000 Royalties payable in 2 nd year on 91, 000 bottles @ Re. 1 = Rs. 91, 000 Royalties payable in 3 rd year on 1, 27, 000 bottles @ Re. 1 = Rs. 1, 27, 000

1 st year To Johnson Ltd. 65, 000 1 st year By Profit & Loss A/c 65, 000 2 nd year To Johnson Ltd. 91, 000 3 rd year To Johnson Ltd. 1, 27, 000 2 nd year By Profit & Loss A/c 3 rd year By Profit & Loss A/c 1, 27, 000

1 st year To Balance c/d 5, 000 1 st By Medico Ltd. yea (15, 000 – r 10, 000) 5, 000 2 nd To Medico Ltd. year 5, 000 2 nd By Balance b/d yea r 5, 000 Shortworking Account can be prepared only in case of a sub -license given to Medico Ltd. because a condition of minimum rent of Rs. 15, 000 has been agreed upon. It cannot be prepared in case of original license given to Don sons Ltd. because of no condition of the minimum rent.