The Origins of the Federal Reserve System Origins

All national banks must join, state-chartered banks")

: The Fed on Supervision • Key function of examination to provide information")

- Slides: 26

The Origins of the Federal Reserve System

Origins of the Federal Reserve System • Panic and Crash 1907, Severe Recession 1907 -1908 • Aldrich-Vreeland Act 1908 • National Monetary Commission 1908 -1911 • …………. . legislative battle begins over the creation of a “central bank”…. how to convince suspicious public and banks? ? • Remember Andrew Jackson and William Jennings Bryan.

Reform after the Panic of 1907? • Fathers of the Federal Reserve found themselves in very similar position to today – Growth of new, riskier financial intermediaries outside of federal regulation – Panics that destabilize the economy • How to reform the National Banking System 1864 -1913? – Monetary Policy – Financial Stability Policy: Regulation & Supervision

Reform of the National Banking System • National Bank Act of 1864 – A Federal “Free Banking” System = Free Entry & Bond-Back Banknotes – High standards for reserve requirements, minimum capital, lending, prohibit branching – Office of the Comptroller of the Currency – Objective: create a nationwide federal system, absorbing state banks. – After 1865 10% on state banknotes, most join.

Reform of the National Banking System • Initial Success – Federal regulation coverage almost universal – Uniform, safe currency [Most of bank liabilities are guaranteed as banknotes are backed by U. S. government bonds] • 1880 s States Revise Banking Codes – Weaker regulations State-Chartered Banks grow rapidly in rural areas – Weaker regulations Trust Companies grow rapidly in major cities – Uninsured Deposit-based banking

The Number of Bank by Charter Type

Shares of Banking Assets

Regulatory Incentives Increased Fragility • Fragmented Banking Structure – – Easy Entry, Low Minimum Capital, Branching Prohibited Thousands of Single Office Banks 1907: 17, 869 NBs, SBs, & TCs Many are small, undiversified, higher failure frequency. • “Pyramiding of Reserves” – High Reserve Requirements & No Central Bank – Reserves held at City Correspondent banks, “Pyramiding of Deposits” in NYC, Chicago – Increases potential for incipient panic to become nationwide, country bank reserves quickly withdrawn – Bankers panics follow public panics • Frequent Panics: 1873, 1884, 1890, 1893, 1907: These are LIQUIDITY EVENTS NOT SOLVENCY EVENTS

Percentage of Bank Insolvencies, 1864 -1913

Assessment of 1864 -1914 • Panics occur beause: • Key Problem 1: Fragmented Banking System—small, undiversified banks with reserves at correspondents, pyramiding • Key Problem 2: Absence of a Central Bank to act as LOLR • [Problem 1 greater? Canada, no central bank, branching no frequent panics]

Federal Reserve Act of 1913 • Problem 2 “solved”: Fed to prevent panics by providing liquidity through the discount window and reduce seasonality of interest rates. • Problem 1 remains—no change in branching prohibition, system with thousands of small, undiversified unit banks.

Origins of the Federal Reserve System • Jekyll Island, 1910 secret meeting Aldrich Plan • Republican controlled Congress produces the Aldrich Bill of 1911 to create a National Reserve Association with $100 million paid-in capital, wholly owned by subscribing banks. • Fifteen regional districts, member banks elect the board of directors. Head office in Washington, but government not represented. • Membership required of national banks but voluntary for state banks. A giant Aldrich. Vreeland plan. • Elections of 1912 ---Republicans defeated, Woodrow Wilson President and Congress is controlled by Democrats

Federal Reserve Act of 1913 • Chairman of House Banking and Currency Committee is Rep. Carter Glass advised by H. Parker Willis----modify Aldrich plan into Federal Reserve Act of 1913. • 12 regional banks and a board---appointed by the President as Wilson insisted: mixed banker & government control.

The Federal Reserve Act of 1913 • Title: “An Act to provide for the establishment of Federal reserve banks, to furnish an elastic currency, to afford means of rediscounting commercial paper, to establish a more effective supervision of banking in the United States, and for other purposes” • High Powered Money before: gold, national bank notes, subsidiary silver and minor coins. • High Powered Money after: gold, subsidiary silver coins AND Federal Reserve notes, and deposits held by banks on the books of the Federal Reserve banks to satisfy reserve requirements.

Federal Reserve Act of 1913 • (1) All national banks must join, state-chartered banks may join if meet requirements of national banks. “Member” and “non-member” banks • (2) All members subscribe to stock in their Federal Reserve Bank = 6% of their capital and surplus. • (3) Reserve requirements for demand deposits, 18% for CRC, 15% for RC banks and 12% for country banks with 5% on all time deposits • (4) Examination by OCC or for state banks by FR Bank • (5) Members may discount short-term qualified paper with their FR Bank—”lender of last resort” • (6) FR Banks to act as clearinghouses for members • (7) Retirement of national banknotes

The Federal Reserve System • A clearing house association writ large. • Idea is that bankers will have local control and they will serve as clearing houses and provide temporary credit. • The Federal Reserve Banks have gold reserve requirements but have a discount window. • Initially----Federal Reserve banks set own discount rates! Finally realize there is arbitrage and centralize open market sales in New York • Learning how to be a central bank……but it does have open market operations and a discount window • SOLVES THE LIQUIDITY PROBLEM (but not fragmentation of banking system) Did it make a difference?

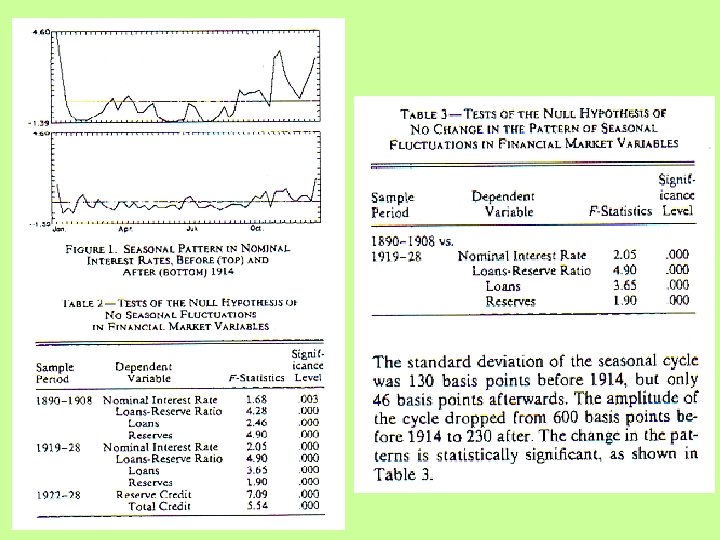

Yes! • Panics tended to occur at times when interest rates were high • Interest rates tended to be high in seasons when loan demand was high or deposit demand was low. • These conditions were acute during the peak agricultural seasons of planting and harvest, spring and fall. • Once in operation, the Federal Reserve intervened in smooth out seasonal interest rate fluctuations

Seasonality in Interest Rates

How bad were things before the Fed? Bernoulli distribution would imply that probability of a panic in a given year is 0. 316 --probability of 14 years with no panic (1915 -1929) is 0. 005

Shorter recessions!

Monetary Policy? • Initial Idea in 1913 was for Fed to be a passive Clearing House, discounting and offering credit to banks only when they asked for it. • It was to follow the “Real Bills Doctrine” and only lend on collateral of short term commercial paper (loans) for purposes of trade and manufacturers--transporting or making real goods. The founders believed thus need of credit balanced with no inflation. • But, it did not happen.

Burgess (1927): The Fed on Supervision • Key function of examination to provide information to Fed on members to “prevent too constant or too large use of borrowing facilities. ” • “Take as an example the perplexing problem of lending to a bank in the farming area of the Middle West in recent years. The First National Bank of Crestland is loaded with doubtful farm paper, much of it representing sometime equities in real estate. ” • “They bring all their good paper to the Federal Reserve Bank to rediscount. Shall the Reserve Bank take it and lend them the money? If the Reserve Bank refuses, failure may follow. If it makes the loan, it assumes the responsibilities of continuing in operation a bank probably insolvent. If failure should then come the depositors might find much of the good assets re-discounted at the Reserve Bank and unavailable to pay depositors. ” • “The Reserve Bank must consider not only the safety of its loan, but the interests of the depositors. Can the bank be saved by a loan? If not, will the depositors be better off under an immediate liquidation, a later liquidation, when the may have dissipated many of its best assets? These are some of the questions the Reserve Bank has to face. The answer depends on a careful scrutiny of each bank, in constant cooperation with state and national supervisory authorities. ”

Incentives to Take More Risk Discount window: Some banks rapidly become dependent on discount window—voluntary liquidations decline In 1925, 593 banks borrowing for more than one year 239 borrowing continuously since 1920 Fed est. 259 of failed banks since 1920 were “habitual borrowers. ”

Monetary Policy? • In its first annual report the Fed rejected a passive clearinghouse role: “the great weight of the Federal Reserve banks influence should be exerted to secure a freer extension of credit and an easing of rates…There will just as certainly, however, be other times when prudence and a proper regard for the common good should be pursued and accommodations curtailed. ” • Countercyclical policy in addition to counterseasonal policy • BUT first HUGE CHALLENGE WORLD WAR I