The New Basel Accord Basel II Three pillars

Three pillars: The first Pillar-Minimum Capital Requirements")

四、新《巴塞尔协议》核心内容简介 The New Basel Accord (Basel II) Three pillars: The first Pillar-Minimum Capital Requirements The second pillar-Supervisory Review Process The third pillar-Market discipline

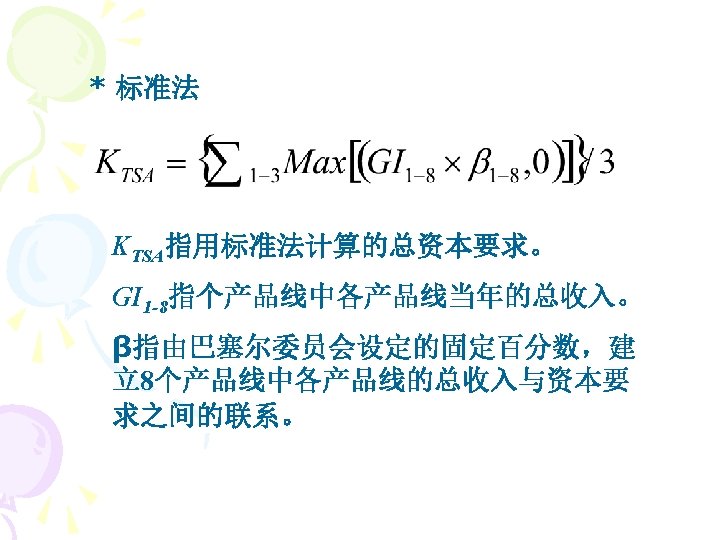

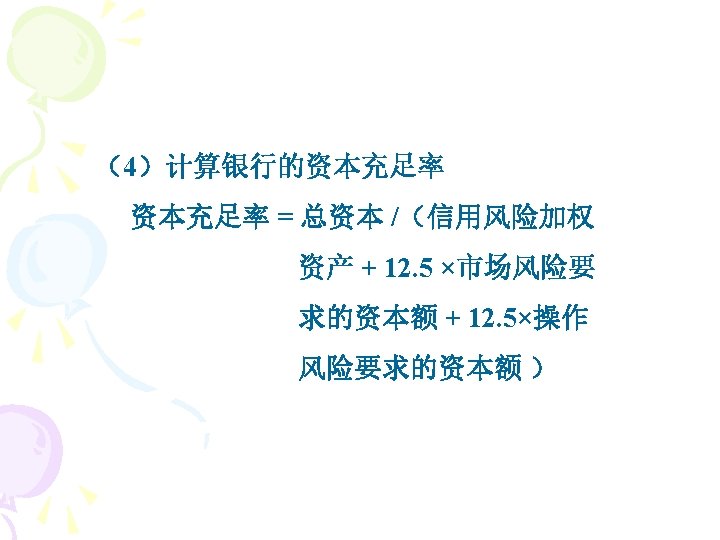

Pillar 1 - Minimum Capital Requirements The Basel Committee discuses the calculation of the total minimum capital requirements for credit, market and operational risk. The minimum capital requirements are composed of three fundamental elements: a definition of regulatory capital, risk weighted assets and the minimum ratio of capital to risk weighted assets. In calculating the capital ratio, the denominator or total risk weighted assets will be determined by multiplying the capital requirements for market risk and operational risk by 12. 5 (i. e. the reciprocal of the minimum capital ratio of 8%) and adding the resulting figures to the sum of risk-weighted assets compiled for credit risk. The ratio will be calculated in relation to the denominator, using regulatory capital as the numerator.

Pillar 2 - Supervisory Review Process Four Key Principles of Supervisory Review: Principle 1: Banks should have a process for assessing their overall capital adequacy in relation to their risk profile and a strategy for maintaining their capital levels. Principle 2: Supervisors should review and evaluate banks’ internal capital adequacy assessments and strategies, as well as their ability to monitor and ensure their compliance with regulatory capital ratios. Supervisors should take appropriate supervisory action if they are not satisfied with the result of this process.

Principle 3: Supervisors should expect banks to operate above the minimum regulatory capital ratios and should have the ability to require banks to hold capital in excess of the minimum. Principle 4: Supervisors should seek to intervene at an early stage to prevent capital from falling below the minimum levels required to support the risk characteristics of a particular bank and should require rapid remedial action if capital is not maintained or restored.

Pillar 3 - Market Discipline The purpose of this pillar is to complement the above two. The Committee aims to encourage market discipline by developing a set of disclosure requirements which will allow market participants to assess key pieces of information on the scope of application, capital, risk exposures, risk assessment processes, and hence the capital adequacy of the institution. The Committee believes that such disclosures have particular relevance under the New Accord, where reliance on internal methodologies gives banks more discretion in assessing capital requirements. The Committee believes that providing disclosures that are based on this common framework is an effective means of informing the market about a bank’s exposure to those risks and provides a consistent and understandable disclosure framework that enhances comparability.

Internal Risk Assessment The new agreement represents a revolutionary change in government regulatory philosophy. Banks will be permitted to measure their own risk exposure and determine how much capital they will need to meet that exposure, subject to review by the regulators to make sure those measurements and calculations are “reasonable”. The banks are required to carry out their own repeated stress testing over the course of the business cycle, using a so-called internal-rating-based (IRB) approach, to ensure they are prepared for the possibly damaging impacts of ever-changing market conditions.

Operational Risk One of the key innovations proposed for Basel II is requiring banks to hold capital to deal with operational risk in addition to credit and market risks. This type of risk exposure includes such things as losses from employee fraud, product flows, accounting errors, computer breakdowns, and natural disasters that may damage a bank’s physical assets and reduce its ability to communicate with its customers.

Set of Rules Basel II is expected to adopt one")

A Dual (Large-Bank, Small-Bank) Set of Rules Basel II is expected to adopt one set of capital rules for the largest multinational banks and another set for smaller banking firms. Regulators are especially concerned that small banks could be overwhelmed by the heavy burdens of gathering risk-exposure information and performing complicated risk calculations. The system may lower the capital requirements of many of the largest banks while it could create a competitive disadvantage for small banks. It is expected that smaller banks will be able to continue to use simpler and more standardized approached in determining their capital requirements and risk exposures.

Remaining Problems of Basel II First, the technology of risk measurement has a long way to go before Basel II is fully implemented. Second, there is complex issue of risk aggregation. Third, it is difficult to deal with the business cycle. Forth, it is a problem to improve regulator competence.

- Slides: 54