THE MISSING TRADER VAT FRAUD SCHEMEA CASE FOR

- Slides: 28

THE MISSING TRADER VAT FRAUD SCHEME-A CASE FOR UGANDA By Shine Gava; Financial Crime Investigations

PRESENTATION OUTLINE Introduction The Missing Trader VAT Fraud Schemes Characteristics - VAT Fraud Schemes Challenges Conclusion

INTRODUCTION - THE VAT REGIME • Illustration 1 § § § Genuine actual transaction Sale Output VAT Purchase Input VAT Output VAT > Input VAT = Pay Output VAT < Input VAT = Claim § § Legal provisions VAT Registration Proper Tax Invoices Taxable goods/services

THE MISSING TRADER VAT FRAUD SCHEMES • Fictitious Companies • Fictitious invoices (Buy or sale of invoices)

MISSING TRADER VAT FRAUD SCHEME • FICTITIOUS COMPANIES § § Fictitious purchases Fictitious Tax Invoices Fictitious Registration Goods from Non Registered customers Case scenario

MISSING TRADER VAT FRAUD SCHEME CONT. …. • Fictitious Invoices (Buy or sale of Invoices) Genuine Companies involved Service companies for supply of goods Fraudsters/Company auditors selling fictitious invoices Several companies involved in buying input tax credit invoices § Construction companies claiming input on raw materials bought by clients § §

CHARACTERISTICS OF VAT FRAUD TRANSACTIONS • Huge cash payments • Orders made over the phone • Invoices generalized e. g. building materials, assorted items, radio equipment • Use of agents /brokers • Delivery on site • Emphasis is issue of invoices

Cash economy Loopholes in the law Illiteracy of some traders Large Informal sector (approx. 50%) Political instability in neighbouring countries e. g. South Sudan and DRC • Limited collaboration between the revenue agencies • • •

CONCLUSION • Different VAT fraud schemes keep emerging; taking different forms in different sectors. • We need to be ahead of the fraudsters by; üTightening our administrative measures, üPolicies üSystems • Use full force of law to deal with fraudsters. The cases discussed are in court at different stages in the prosecution process

ILLUSTRATION 1: VAT REGIME B sells to C Output VAT B & Input VAT C Co. A Co. B A sells to B Output VAT A & Input VAT B Co. C Final consumer pay the VAT C sells to final consumer Output VAT C NB: 1. A, B & C are all VAT registered. 2. Co. B’s VAT payable = Output VAT B - Input VAT B, 3. Co. C’s VAT payable = Output VAT C - Input VAT C 4. If B or C disappears , VAT is lost

ILLUSTRATION 2 TRANSACTIONS FLOW

18% VAT Charged

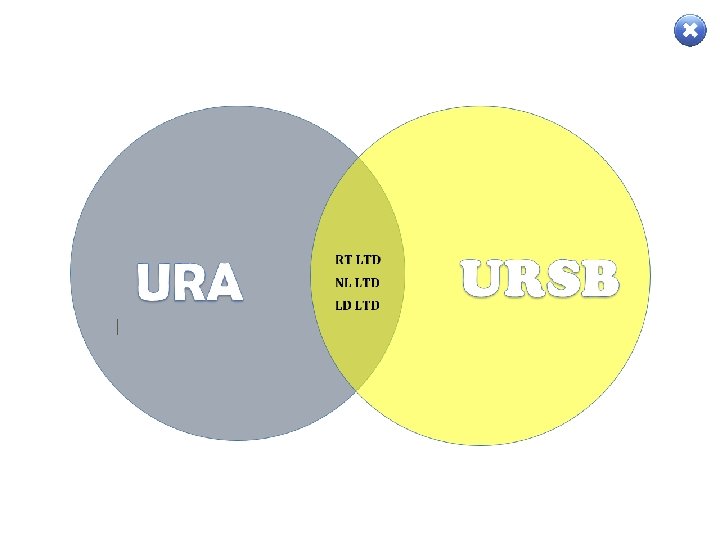

NON VAT REGISTERED CUSTOMERS Individual X, Y VAT REGISTERED COMPANIES RT Ltd NL Ltd Individual V Individual W LD Ltd

BROKER R COMPANY Z BROKER M Companies Z and H are created. RT Ltd, NL Ltd and LD Ltd allegedly hire trucks from Z and H RT Ltd NL Ltd LD Ltd COMPANY H

BROKER R BROKER M • Use a broker M who issues tax invoices and receives cash payments • Broker M also has no knowledge of Z and H and uses Broker R • Broker R is unknown (Nonexistent)

FACTS ABOUT Z AND H • Z and H are registered with URA • Z and H are not registered with URSB • Z and H used forged URSB registration details to register with URA • Directors are non-existent. Have Chinese names • Companies nonexistent at registered addresses • Z and H trade with each other. File returns online. Both in a VAT claimable position

ILLUSTRATION 3 USE OF FICTITIOUS INVOICES

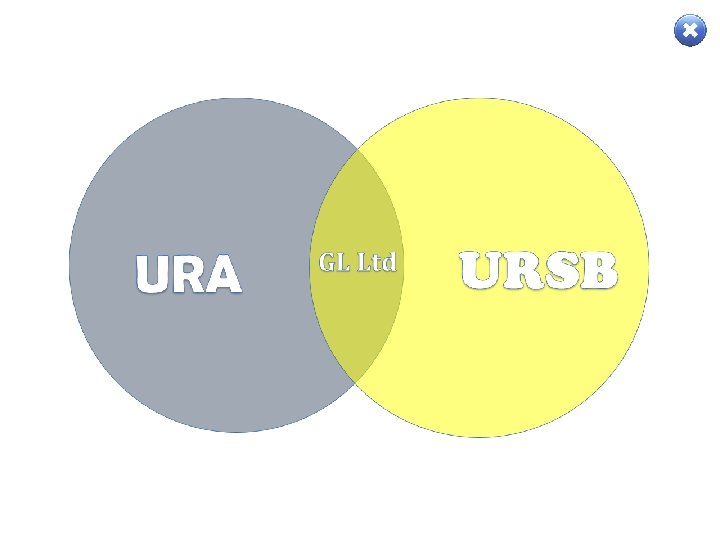

GL LTD GL Ltd is a construction company GL Ltd is well registered with URA and

AN NON VAT REGISTERED CUSTOMERS X, Y, Z • AN is the procurement officer of GL Ltd • Procures construction materials from X, Y and Z; non VAT registered customers • AN needs to claim input VAT credit on the purchases from NR customers

EK HK H LTD B LTD • AN connives with HK and EK, accountants of H Ltd and B Ltd respectively • Tax invoices are created allegedly from H ltd and B Ltd as the suppliers • HK and EK file returns and include the tax invoices created from a fictitious sale

B LTD H LTD • The owners of companies H and B are not aware of the fictitious transaction • Directors of GL Ltd are convinced the purchases were made from H Ltd and B Ltd

GL LTD

Facts • GL Ltd is a construction company • GL Ltd is well registered with URA and URSB • AN is the procurement officer of GL Ltd • Procures construction materials from X, Y and Z; non VAT registered customers • AN needs to claim input VAT credit on the purchases from NR customers • AN connives with HK and EK, accountants of H Ltd and B Ltd respectively • Tax invoices are created allegedly from H ltd and B Ltd as the suppliers • HK and EK file returns and include the tax invoices created from a fictitious sale • The owners of companies H and B are not aware of the fictitious transaction • Directors of GL Ltd are convinced the purchases were made from H Ltd and B Ltd • GL Ltd claims input VAT credit