The Jewish Community Foundation of Montreal Welcomes you

Isabelle Nadeau, B. C. L. ,")

• The definition")

• TOSI does not")

• TOSI does not")

The CRA has")

Are typical estate")

Modified structure #1:")

Modified structure #2:")

")

:")

")

Associated corporations")

Ordering on how a dividend refund")

provides that the dividend")

either I. if the amount determined under (a)(I) exceeds the")

51 ► The Canada Business Corporations")

: i) with direct")

- Slides: 98

The Jewish Community Foundation of Montreal Welcomes you to PAC 2019 1

Welcome Update on Tax on Split Income (TOSI) Isabelle Nadeau, B. C. L. , LL. B. , LL. M. Fisc. Crowe BGK LLP June 13, 2019

Today’s Agenda 1. Brief summary of the TOSI rules Recent guidance from the Canada Revenue Agency 2. on the TOSI rules 3. Selected planning opportunities © 2019 Crowe BGK LLP 3

1. Brief summary of the TOSI rules © 2019 Crowe BGK LLP 4

1. Brief summary of the TOSI rules - Fundamentals The following is a simplified and non-exhaustive overview of the TOSI rules found in section 120. 4 of the Income Tax Act. • The new TOSI rules are applicable since January 1, 2018. • TOSI applies when a “specified individual” earns “split income”, unless an exception can be found. o When income is subject to TOSI, it is taxed at the maximum personal tax rate, which effectively eliminates the tax benefits for sprinkling income amongst family members. • A “specified individual” designates any individual who is resident in Canada, except a trust. In the case of minor children, there is an additional requirement to have a parent resident in Canada. © 2019 Crowe BGK LLP 5

1. Brief summary of the TOSI rules – “Split income” • The definition of “Split income” includes different types of income: o Taxable dividends received on shares of private corporations, whether earned directly by the “specified individual” or via a trust or partnership o Income allocated by a partnership or trust, if it is derived from: i. Rental income, on condition that a family member of the “specified individual” has a sufficient connection with the rental activities; or ii. A “related business” is a business with which a family member of the “specified individual” has a sufficient connection due to the family member’s involvement in the activities of the business (activity test) or due to the family member’s financial participation in the business carried on by a corporation or a partnership (ownership test). © 2019 Crowe BGK LLP 6

1. Brief summary of the TOSI rules – “Split income” (cont’d) • The definition of “Split income” includes different types of income: o Interest earned on debt obligation issued by private corporations o Taxable capital gains realized personally or via a trust on the disposition of: i. Shares of private corporations, and ii. In certain circumstances: Ø an interest in a partnership or trust Ø a debt obligation issued a private corporation © 2019 Crowe BGK LLP 7

1. Brief summary of the TOSI rules – Exceptions • TOSI does not apply to the following types of income: o Exceptions available to all “specified individuals”: Ø Taxable capital gains realized personally or via a trust on the disposition of “qualified small business corporation shares” Ø Income or taxable capital gains earned by a “specified individual” whose spouse or common-law partner has reached the age of 64, to the extent that this income/gain would not have been “split income” if it had been earned by the spouse/common-law partner © 2019 Crowe BGK LLP 8

1. Brief summary of the TOSI rules – Exceptions (cont’d) • TOSI does not apply to the following types of income: o Exceptions available to “specified individuals” aged at least 17: Ø Income not derived from a “related business” of the “specified individual” Ø Income derived from an “excluded business” of the “specified individual” An “excluded business” is a business with which the “specified individual” is/was actively engaged on a regular, continuous and substantial basis in the relevant year or in five past years. Where an individual works in the business at least 20 hours/week on average during the portion of the year in which the business operates, he or she is deemed to be actively engaged on a regular, continuous and substantial basis. © 2019 Crowe BGK LLP 9

1. Brief summary of the TOSI rules – Exceptions (cont’d) • TOSI does not apply to the following types of income: o Exceptions available to “specified individuals” aged at least 24: Ø Income that is a “reasonable return” for the contribution in the business made by the “specified individual” considering labour, capital, risks assumed, etc. Ø Income from (or taxable capital gains from the disposition of) “excluded shares” owned by the “specified individual”. Shares qualify as “excluded shares” if the following conditions are met: i. the corporation carries on business, is not a “professional corporation” and less than 90% of its prior year’s business income is from the provision of services; ii. the shares represent 10% or more of the votes and value of the corporation; and iii. 90% or more of the corporation’s business income is not derived from another related business of the “specified individual” © 2019 Crowe BGK LLP 10

2. Recent guidance from the CRA on the TOSI rules © 2019 Crowe BGK LLP 11

2. Recent guidance from the CRA on the TOSI rules The CRA has confirmed that the application of the TOSI rules may cause surprising results. Two structures which are economically similar may not attract the same TOSI treatment: Scenario 1 Scenario 2 In this scenario, dividends received by the Spouse on shares of Opco are not subject to TOSI. The “excluded shares” exception is met. In this scenario, dividends received by the Spouse on shares of Holdco are subject to TOSI. The “excluded shares” exception is not met. Source: Technical interpretations 2018 -0761601 E 5 and 2018 -0768801 C 6 © 2019 Crowe BGK LLP 12

2. Recent guidance from the CRA on the TOSI rules (cont’d) The CRA has confirmed that supporting documentation is key in claiming an exception to the TOSI rules. Example: Dividends received by Mrs. X that are derived from business A only will not be subject to TOSI as business A is an “excluded business” of Mrs. X. To support the right to claim the “excluded business” exemption, the CRA requires that funds can be clearly traced. Source: Technical interpretation 2018 -0761601 E 5 © 2019 Crowe BGK LLP 13

3. Selected planning opportunities © 2019 Crowe BGK LLP 14

3. Selected planning opportunities – A. Structures involving family trusts Are typical estate freezes still relevant? Illustration of typical estate freeze Before the freeze © 2019 Crowe BGK LLP 5 years after the freeze 15

3. Selected planning opportunities – A. Structures involving family trusts (cont’d) Are typical estate freezes still relevant? YES: • A typical estate freeze structure still allows the multiplication of the lifetime capital gains exemption. • A typical estate freeze structure can help reduce taxes payable upon eventual death of the Founder by reducing the value of the assets owned directly by the Founder at the time of death. Children However, under the new TOSI rules, this structure no longer allows the splitting of dividends amongst family members who are beneficiaries of the trust and who do not contribute to Opco’s business. © 2019 Crowe BGK LLP 16

3. Selected planning opportunities – A. Structures involving family trusts (cont’d) Modified structure #1: dividend splitting opportunity in certain circumstances Dividends received by the Founder’s spouse and children who are at least 24 will not be subject to TOSI (“excluded shares” exception). © 2019 Crowe BGK LLP The common shares of Opco held by the family members must represent at least 10% of Opco’s votes and value. 17

3. Selected planning opportunities – A. Structures involving family trusts (cont’d) Modified structure #2: purification of Opco and potential additional dividend splitting opportunity • Inter-corporate dividends can be paid from Opco to Holdco (via the trust) to remove excess cash and cashlike investments which may disqualify Opco’s shares for the purposes of claiming the capital gains exemption. • Can Holdco’s investment income derived from its portfolio of marketable securities be paid out as dividends to a family member without attracting TOSI? Needs to be further clarified. * © 2019 Crowe BGK LLP The common shares of Opco held by the family members must represent at least 10% of Opco’s vote and value. * Source: technical interpretations 2018 -0768801 C 6; 2018 -0771861 E 5; 2018 -0779981 C 6; 2018 -0768821 C 6 18

3. Selected planning opportunities – B. Prescribed interest rate loans Loan to low-income family member is Loan to trust in which a low-income family member beneficiary The loan must bear interest at the prescribed rate applicable at the time the loan is granted (currently 2%). Interest must be paid annually, by January 30 of the following year at the latest. Very important to avoid tax attribution rules Result: TOSI will not apply to dividends and capital gains earned on public corporation shares as there are specific exceptions in the definition of “split income” for these types of income. © 2019 Crowe BGK LLP 19

3. Selected planning opportunities – C. Paying salaries to low-income family members • Salaries received by family members from a corporation are not subject to the TOSI rules. • Like any expense, salaries are subject to a reasonability test. o To be tax deductible by the corporation that pays them, the salaries must be reasonable in regards to the work performed by the employees. o Work done by family members earning a salary should be carefully documented. • In addition to being an effective income splitting strategy in the year in which they are paid, reasonable salaries paid to family members provide other long-term tax benefits by allowing family members to accrue RRSP room. © 2019 Crowe BGK LLP 20

3. Selected planning opportunities – D. Paying dividends to lowincome family members who were previously involved in the business • If a family member was actively engaged in the business carried on by a corporation but has temporarily or permanently ceased to be active in the business, dividends can still be paid to this low-income family member without causing the TOSI rules to apply to the dividend if the family member was actively involved in the business during at least five years in the past. o These years do not need to be consecutive. • The dividends paid to this family member will not be subject to TOSI based on the “excluded business” exception available to “specified individuals” having reached the age of 17. • The non-application of TOSI in this context has been confirmed by the CRA in technical interpretation 2018 -0783741 E 5. © 2019 Crowe BGK LLP 21

3. Selected planning opportunities – E. Other simple income splitting strategies Paying to family members dividends from the corporation’s capital dividend account • These dividends are not taxable and therefore they are excluded from the definition of “split income”. The family members can then invest the funds to earn investment income that will be taxed in their hands at the lower tax rates. TFSA contributions • A high-income individual may contribute to his or her spouse’s TFSA. This allows the spouse to earn tax-free investment income. • Tax attribution rules do not apply to TFSA contributions. Payment of family expenses • The high-income spouse should consider paying for all family expenses to allow the lowincome spouse to retain his or her earnings. This will maximize the capital that low-income spouse can invest to generate investment income that can then be taxed at the lower tax rates. © 2019 Crowe BGK LLP 22

Thank You Isabelle Nadeau, B. C. L. , LL. B. , LL. M. Fisc. Tax Partner Crowe BGK LLP T: +1 (514) 908 3625 E: i. nadeau@crowebgk. com Crowe BGK LLP is a member of Crowe Global, a Swiss verein. Each member firm of Crowe Global is a separate and independent legal entity. Crowe BGK LLP and its affiliates are not responsible or liable for any acts or omissions of Crowe Global or any other member of Crowe Global does not render any professional services and does not have an ownership or partnership interest in Crowe BGK LLP. © 2019 Crowe BGK LLP

Analyzing the New Passive Investment Income Rules & RDTOH Regime Robert Korne LLB/B. C. L. , TEP, Spiegel Sohmer Inc. June 13, 2019 (This presentation was part of a larger presentation previously prepared and presented with Steven Moses of PSB Boisjoli S. E. N. C. R. L. - LLP)

Passive Investment Income Why the changes? Current corporate taxation A Canadian-controlled private corporation (“CCPC”) earning active business income (“ABI”) can benefit from a “small business deduction” (“SBD”) and taxed at an even lower rate on its first $500, 000 of ABI (SBD limit must be shared among a group of associated corporations) SBD is eliminated gradually as taxable capital within an associated corporate group increases from $10 M to $15 M

Passive Investment Income Stated objectives of SBD: To increase the after-tax cash available for CCPCs to reinvest in their business Recognizes that small businesses may have difficulty accessing capital Perspective of Finance Department: “When retained earnings taxed at the small business rate are used for passive investments rather than in the business, significant tax deferral advantages can be realized relative to an individual investor”

Passive Investment Income

Passive Investment Income 2018 federal budget proposed to: i. Reduce the tax rate on active business income eligible for the SBD (10% for 2018 and 9% for 2019) – (from fall 2017) ii. Reduce the SBD limit for companies within an associated group based on passive income beginning after 2018. iii. Limit the availability to recover RDTOH when an eligible dividend is paid.

Passive Investment Income How does it work? The SBD will be reduced based on an associated group’s annual passive income Up to $50, 000 of prior year’s passive income (“adjusted aggregate investment income” (“A. A. I. I. ”)) is acceptable A. A. I. I. of between $50, 000 and $150, 000 will reduce access to the SBD Each $1 of passive income in excess of $50, 000 reduces SBD availability by $5

Passive Investment Income For these purposes, two new definitions were added in s. 125(7): (i) A. A. I. I. and (ii) “active assets” for the purposes of calculating the business limit reduction. To determine A. A. I. I. , start with the “aggregate investment income” and modify: i. exclude capital gains or losses realized on the disposition of “active assets” ii. add back net capital losses carried over from another year and foreign taxes paid on foreign accrual property income (“FAPI”) iii. Include dividends from non-connected corporations (portfolio dividends) and iv. Include income from a specified investment business and income from savings in a life insurance policy that is not an exempt policy

Passive Investment Income An asset of a CCPC will be an “active asset” if: i. it is an asset used principally in an active business carried on primarily in Canada by the CCPC or a related CCPC (an “Active Business Property”) ii. it is a share of a corporation with which the CCPC is connected (for the purposes of Part IV) and would meet the definition of a “qualified small business corporation share” in s. 110. 6(1) if it were held by an individual shareholder (“Active Shares”) or

Passive Investment Income iii. the asset is an interest in a partnership where a) the fair market value of the interest held by the CCPC is at least 10% of the fair market value of all of the partnership interests b) throughout the 24 months prior to the disposition date more than 50% of the fmv of the partnership’s property (directly, or through another partnership) was attributable to Active Business Property or Active Shares and c) on the disposition date all or substantially all of the fmv of the partnership’s property (directly or through another partnership) was attributable to Active Business Property or Active Shares

Passive Investment Income – Aggregate Investment Income

Passive Investment Income – A. A. I. I.

Passive Investment Income Impact on associated companies Daughter-in-law Beneficiaries 100% shares DILco - Father-in-law - Son - Grandchildren (minors) FT 100% Common shares FILco Father-in-law 100% freeze voting preferred shares Active Business Portfolio earns $200, 000 of A. A. I. I.

Passive Investment Income Question: Is the SBD of DILco ground down? Answer: Yes, as DILco and FILco are associated, pursuant to s. 256(1)(b) Why? - s. 256(1. 2)(f)(ii) deems each beneficiary (including minors) to own all of the common shares owned by FT - s. 256(1. 3) deems each parent to own shares owned by minors, including those deemed by s. 256 (1. 2)(f)(ii) - s. 256(1. 2)(c)(ii) deems control by a person who owns common shares of a corporation with a FMV of more that 50% of the FMV of all issued common shares Therefore, daughter-in-law is deemed to control both companies

Passive Investment Income Technical Interpretation: 2017 -0685121 E 5 (September 14, 2017) Associated corporations - through third corporation: 256(2) Aco, Bco and Cco – each owned 100% by a different child; Dco – controlled by taxpayer + nonvoting common shares owned by discretionary trust S. 256(2) applies such that Aco, Bco and Cco are associated among selves Three s. 256(2) elections by Dco: Aco, Bco and Cco are not associated for purposes of s. 125(1) and Dco’s business limit deemed nil S. 256(2) election now more important Aco will avoid A. A. I. I. and taxable capital of Bco and Cco; Aco, Bco and Cco each still associated with Dco A. A. I. I. and taxable capital of Dco taken into account for Aco’s, Bco’s and Cco’s business limit grind under s. 125(5. 1)

Passive Investment Income Planning ideas to minimize SBD grind Corporate-owned life insurance - not A. A. I. I. contributions in excess of pure cost of insurance and then extract as CDA policy as collateral for loan Investments that minimize taxable distributions Capital gains Investing in longer-term assets Timing dispositions – (i) no longer active or (ii) all in same year Investments in non-associated corporation Restructure ownership Caution: s. 125(5. 2) – anti-avoidance rule. Transfer or loan to a related corporation - one of the purposes is to avoid the new rules - related corporations deemed to be associated for the purpose of A. A. I. I.

Passive Investment Income New RDTOH Regime Before new regime: tax refund by corporation on investment income regardless of whether dividends paid were as eligible or non-eligible. The objective for the changes was to “better align the refund of taxes paid on passive income with the payment of dividends sourced from passive income” (2018 federal budget). For taxation years beginning after 2018, the amount of RDTOH available is limited when eligible dividends are paid (i. e. from income taxed at the general corporate active rate).

Passive Investment Income

Passive Investment Income How does it work? 30. 67% of investment income is included in the RDTOH account Canadian portfolio dividends: 38. 33% Part IV tax and same added to RDTOH Refund rate: $0. 3833 for each $1 of taxable dividends paid Two RDTOH pools - Exception: eligible refundable dividend tax on hand (“ERDTOH”): - Part IV tax resulting from eligible portfolio dividends; and - connected corporate dividends to the extent of any ERDTOH refund - General rule: non-eligible refundable dividend tax on hand (“NRDTOH”)

Passive Investment Income How does it work? (con’t) Ordering on how a dividend refund is calculated: - Eligible dividends only enable a refund of the company’s ERDTOH balance - Eligible dividends do NOT enable a refund of NRDTOH - ONLY non-eligible dividends enable a refund of the company’s NRDTOH - Non-eligible dividend may enable a refund of the company’s ERDTOH

Passive Investment Income ORDERING: how does this work? S. 129(1) provides that the dividend refund will be equal to the total of: i. for eligible dividends, an amount equal to the lesser of a) 38 1/3% of the total of all eligible dividends paid by it in the year, and b) its ERDTOH at the end of the year, and ii. in respect of taxable dividends (other than eligible dividends), an amount equal to the total of a) the lesser of I. 38 1/3 % of the total of all taxable dividends (other than eligible dividends) paid by it in the year, and II. its NRDTOH at the end of the year, and

Passive Investment Income b) either I. if the amount determined under (a)(I) exceeds the amount determined under (a)(II), the lesser of 1. the amount of the excess, and 2. the amount by which the corporation’s ERDTOH at the end of the year exceeds the amount, if any, determined under subparagraph i. for the year, or II. in any other case, nil If 38 1/3% of non-eligible div ˃ NRDTOH balance → access ERDTOH bal.

Passive Investment Income Example: ERDTOH balance = $ 50 NRDTOH balance = $ 200 Pay non-eligible dividend = $1, 000 Dividend refund equals the following: 1. in respect to eligible dividends: $0 2. in respect of non-eligible dividends: $250 ($200 + $50) Therefore all ERDTOH is refunded on a non-eligible dividend paid

Passive Investment Income Part IV tax refunds will remain available from all the accounts, subject to the s. 129(1)(a) ordering rule. Effect will be that GRIP dividends will only give rise to Part IV tax refunds if there is sufficient ERDTOH Non-eligible dividends will give rise to NRDTOH first and then to ERDTOH Eligible dividends are much less attractive when NRDTOH exists in excess of the ERDTOH balance

Passive Investment Income THANK YOU VERY MUCH

POTPOURRI presented to PAC 2019 Nancy Cleman LAPOINTE ROSENSTEIN MARCHAND MELANÇON, S. E. N. C. R. L. June 13, 2019

49 Topics ► Bill 86 - Amendments to the CBCA to identify individuals with signifigant control –in force June 13, 2019 ► Enquiries in Canada and Abroad in the context of a tax audit- what you need to produce for a Requirment ► Estate matters- Obligations to file US Estate returns if deceased holds US situs assets in excess of US $60 K ; ► Digital Assets- developments and tips

50 From Corporations Canada website ► As of June 13, 2019, all Canada Business Corporations Act (CBCA) corporations, except some distributing corporations, will have to create and maintain a new type of register that lists all individuals that have a significant control over the corporation. ► The intent of the Individuals with Significant Control (ISC) Register is to provide greater transparency over who owns and controls a corporation, and to help law enforcement agencies expose activities like money laundering and tax evasion.

NEW Corporate Register INDIVIDUALS WITH SIGNIFIGANT CONTROL (ISC) 51 ► The Canada Business Corporations Act has been amended to require that individuals who control 25% or more of votes or value of a corporation must be declared in the minute book; ► Control means direct or indirect influence that if exercised would result in control in fact over the corporation; ► This also applies to Joint ownership of control ie two or more individuals and can extend to interests or rights or a combination thereof;

52 Need to prepare a new register for ISCs ► name ► date of birth ► last known address ► jurisdiction for tax purposes ► date on which the individual acquired significant ownership or control ► date on which the individual ceased to have significant ownership or control ► description of how the individual meets the definition of significant control

53 The definition is quite broad: ► Defining 'individual with significant control' ► An individual with significant control, or ISC, is an individual who ► owns a significant number of shares ► controls or directs a significant number of shares ► has significant influence over the corporation without necessarily owning a significant number of shares, or ► has a combination of any of these factors.

54 Significant control means: ► A significant number of shares is ► 25% of the voting shares, or ► 25% of all the shares based on the fair market value of the shares. ► An individual can also be an ISC if this individual owns or controls a significant number of shares with one or more other individuals. While each of these individuals may not be an ISC on their own, together they become ISCs when they own or control shares. The corporation will need to record each individual, as each is an ISC, in the ISC Register.

55 Who is implicated ► Trusts ► Holding companies ► Voting trusts ► Testamentary trusts

56 Need to identify Name of each individual (each, an "Individual"): i) with direct or indirect : a) control or direction over the Shares ("Control") or; b) influence that, if exercised, would result in control in fact of the Corporation ("Influence"); ii) having an interest or right (or a combination of interests or rights) in the Shares or direct or indirect control or direction over the Shares that is held jointly with one or more other individuals ("Joint Control"), or

57 Corporations have 3 Obligations for ISC Register ► Identify ISCs ► Record ISCs ► Update the ISC register at least once a year and within 15 days of becoming aware of a change ► Failure to comply can result in corporations directors, officers or shareholders being subject to penalties, including fines and imprisonment ( $200 K /6 mon) ► Obligation to dispose of information on the ISC within one year after the 6 th anniversary person ceased to be an ISC

58 Must contact and identify ISCs ► Corporations must identify ISCs for the corporation. This includes contacting all shareholders and asking them if they own the shares directly or if they are holding them on behalf of someone else. ► Shareholders have an obligation to provide accurate and complete information in response to any request from the corporation about the ISC Register. Once shareholders receive a request from the corporation, they are expected to respond as soon as possible.

59 Access to info / fines and penalties ► Shareholders, creditors or personal representatives and revenue authorities may request access to the registers; ► It will eventually become available to police forces and federal and provincial revenue agencies ► Need to fulfil some formalities; ► For now the registers will not be public; ► We expect this type of requirement will be adopted by the provinces;

60 Use of information ► Shareholders and creditors may only use the information in connection with an effort to influence the voting of shareholders of the corporation, an offer to acquire securities or other matters relating to the affairs of the corporation;

61 Challenges for professionals –value and control ► On the website Corporations Canada advises: ► The Canada Business Corporations Act does not provide a definition of fair market value. You can seek guidance from your financial and legal advisors on how to determine fair market value of your corporation's shares. ► The Canada Business Corporations Act does not provide a definition for control in fact. You can seek legal advice to determine how "control in fact" applies to your circumstances. ► ( thank you to Rosa Pinheiro, Perry Kliot & Simon Robillard)

US Situs assets- filing obligations for Canadian estates ► There may be an obligation to file a US estate return if the deceased held more than US 60, 000 US situs assets; ► US situs assets include shares held in an investment account or RRSP ; ► The filing obligation exists even if there is NIL exposure to pay taxes; ► The form is normally filed within 9 months after date of death ; an extenstion to file must be requested before the 9 month period expires; ► Post 9 months the request for an extenstion may be refused and there may be a penalty; 62

US SITUS PROPERTY – ESTATE RETURNS FOR CANADIAN ESTATES -INFO ► Date of Birth Of DECEASED ► Executor(s)name and Address(es) and telephone number. ► Beneficiaries names, addresses and distribution received so far. ► How will the distribution among the beneficiaries be done i. e. proportions ► Names & SSN of the beneficiaries US citizens or applied for or received a green card ► Identify beneficiaries currently living in the US under a work visa or TN visa 63

64 Forms to be filed ► 706 -NA with schedules ► Schedule R and related annexes of Form 706 , if assets are not liquidated and are transferred to another trust the beneficiaries of which are likely to be US citizens ► Form 8833 Treaty based disclosure ► Form 8971 Information regarding beneficiaries ; ( penalty is USD $260 per form filed) ► ( thank you to Hachem Halabi of RSW)

Informal request for information and requirements in the context of a tax audit 65 ► In the course of an audit Canadian tax authorities can send a Requirement request which is more coercive than an informal request; ► Requirements require a person ( taxpayer or 3 rd party) to produce information or documents with respect to enforcement of the Income Tax Act (ITA), a tax treaty or international agreement; ► Requirements carry penalties and imprisonment if there is a failure to comply and must follow certain formalities ( i. e. service/certified or registered mail)

66 Requirements in a tax audit ► Tax authorities cannot require a specific format ► Tax authorities can contact third parties (e. g. financial institutions) ► 2018 decision Canada (National Revenue) v. Hydro. Québec, 2018 CF 622, it was decided that full scale fishing expeditions are not permitted; ► If Revenue Canada wants information on a group it must be an identifiable group pursuant to the parameters of the tax legislation

67 Canadian documents ► If tax authorities have not identified the taxpayers who may be included in the bonafide tax audit then the group is not identifiable; ► A tax audit is not in good faith when taxpayers have been identified as a result of a search based on parameters not related to the Act; ► The fact that the tax authorities ask for something does not mean it will be accorded if there is no strong link to the Act and the group is not identifiable;

68 Requirements continued ► Requirements about unnamed persons require that an application be filed with the Federal Court by the minister. ► Requirements for information about unnamed persons can be contested in front of the court on the basis that the group is not identifiable and (ii) that the information sought is not useful to verify if the taxpayer respects the ITA. ► NB: if the information is accessible in Canada but stored in a cloud in US it can be treated as a Canadian document and subject to Canadian rules ( e. Bay Canada Ltd v MNR 2010 1 FCR 145)

69 Foreign based information or documents ► Foreign based information requests relate to information that is available or located outside Canada and may be relevant to the enforcement of the ITA. ► Test is whether the information requested is useful for the purposes of the Act; not in determining the person’s liability for tax. ► Taxpayers can apply to a judge for review of a requirement regarding foreign documents. The judge can confirm the requirement; vary it or set it aside. ► ( with thanks to Pierre Girard & Jean Francois Dorais)

70 Other matters ► Inform your clients that if they receive a call from Revenue Canada or Revenue Quebec to assist with an inquiry there is nothing wrong with speaking to your counsel and having them call the investigator; ► The client should not feel compelled to submit themselves to an “interview”; ► Tip for a non resident who may be getting a refund for withholding taxes: consider opening a bank account in Canada so that the cheque(s) can be cashed; ► It is difficult to cash a Revenue Canada cheque abroad; RC will issue a cheque in another currency if asked;

71 DIGITAL ASSETS UPDATES ► Very important to take an inventory of digital assets including who controls them and ensure access; ► This includes social media sites; domain names; email accounts; ► The rules around management of these assets are constantly changing ; ► Facebook default position is now to memorialize all accounts; ► Digital assets such as domain names are very valuable and should be taken into consideration when doing valuations;

72 What you can’t see can hurt you ► Google & Gmail: - can appoint a trusted contact; user must set up inactive account manager and decide which data to share with trusted contact; ► Google will not provide password but may provide content to immediate family members and representatives ► Can be critical if people use Gmail to manage their online life and business; ► All platforms have different policies so it is important to review from time to time and ensure you have a plan; ► ensure proper clauses in wills and mandates

73 Other considerations ► Before you give away an asset such as a laptop or phone make sure you have a copy of the relevant data ; ► You may need to keep a cellphone account active for several months since it is the access point to other online accounts such as whats app; ► Cell phones can be used to reset passwords or for two step identification;

74 Contact Me Nancy Cleman Téléphone : 514 925 -6374 Nancy. cleman@lrmm. com Pierre. Girard@lrmm. com The content of this presentation is to provide general information only and should not be relied upon as legal advice

Osler, Hoskin & Harcourt S. E. N. C. R. L. /S. R. L Jewish Community Foundation of Montreal Professional Development Seminar – Pot. Pourri David Wilson June 13, 2019

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Agenda • Quebec Minister of Finance – Information Bulletin 2019 -5 ◦ Nominee (prête-nom) agreements and sham transactions ◦ Sham case law update • Federal Budget 2019 – employee stock option changes • New trust reporting rules 77

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 • Released on May 17, 2019 • Three additional measures that will apply from May 17, 2019 ◦ 1) Mandatory disclosure of nominee agreements ◦ 2) Extension of mandatory disclosure rules to prescribed transactions ◦ 3) Measures related to “sham” transactions 78

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 1) Mandatory disclosure of nominee agreements • Applies to relationships governed by “secret contracts” containing “true intent” of parties – as opposed to “apparent contract” available to third parties. • Includes “prête-nom” (nominee) agreements and certain contracts of mandate. ◦ Very common in real estate space • Parties to nominee agreement are required to file a prescribed form within 90 days of the conclusion of the agreement. • Where the tax consequences of a transaction concluded before May 17, 2019 continue after that date, the parties to the transaction have until September 16, 2019, to disclose the information pertaining to the nominee agreement. • Where disclosure is made by one of the parties to the nominee agreement, all parties to the agreement will be deemed to have made the required disclosure. 79

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 1) • Mandatory disclosure of nominee agreements Prescribed form: ◦ Not yet available (August 17, 2019 earliest possible due date for new nominee agreements, September 16, 2019 for existing nominee agreements) ◦ Must include: • Date of nominee agreement • Identities of parties to nominee agreement • Full description of the facts of the transaction or series of transactions to which the nominee agreement relates and the identity of any person or entity for which such transaction or series of transactions has tax consequences ◦ • Prescription period / statute-barring: ◦ 80 Penalties for failure to file: $1, 000 base penalty + $100 per day up to maximum of $5, 000 (parties jointly liable) If prescribed form is not duly filed, prescription period otherwise applicable will be suspended indefinitely with respect to the tax consequences arising from a transaction or series of transactions that are part of the nominee agreement

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 2) Extension of mandatory disclosure rules to “prescribed transactions” • Mandatory disclosure rules currently apply to limited number of transactions (e. g. transactions where advisor requires confidentiality from client, where advisor’s compensation is contingent) • Failure to comply with mandatory disclosure rules exposes taxpayers to penalty of $10, 000 plus $1, 000 per day up to maximum of $100, 000 • New measures: ◦ Mandatory disclosure rules will be expanded to transactions that are “prescribed transactions” ◦ “Prescribed transactions”: transaction or a series of transactions carried out by a taxpayer “whose form and substance are very similar, but not necessarily identical” to transactions specified by Revenu Québec on a public list ◦ “Prescribed transactions” not yet announced ◦ Disclosure obligation satisfied by filing of prescribed form within 60 days of the commencement of the prescribed transaction or 120 days from the day disclosure of the particular prescribed transaction is made mandatory by Revenu Québec ◦ Failure to file: • penalties up to $100, 000 plus 50% of the tax benefit resulting from the undisclosed transaction • Indefinite suspension of prescription period for taxation year for which disclosure required 81

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 2) • Extension of mandatory disclosure rules to “prescribed transactions” Tax advisors and promoters: ◦ New measures will also apply to tax advisors and promoters ◦ Advisors or promoters who commercialize or promote a prescribed transaction whose form and substance has not required a material change when implemented for different taxpayers is required to file an information return including following information: • Full description of the facts of the prescribed transaction; • Any other information requested in the prescribed form ◦ Information return required to be filed on earlier of: • 60 days after the day on which the advisor or promoter first commercializes or promotes the prescribed transaction, or • 120 days after the day on which Revenu Québec publically announces that transaction is prescribed ◦ Failure to file information return: • $10, 000 base penalty plus $1, 000 per day up to maximum of $100, 000 • Liable for entire amount received in fees earned in relation to prescribed transaction 82

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 3) Measures related to “sham” transactions • According to Quebec Minister of Finance: “A sham is a complex transaction or series of transactions which has an element of deception aimed at misleading the tax authorities as to a taxpayer’s identity or the actual nature of a transaction or series of transactions. ” • New measures relate to: 83 ◦ Penalties ◦ Prescription period ◦ Access to public contracts

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 3) Measures related to “sham” transactions • 84 Penalties: ◦ If Revenu Québec issues an assessment to a taxpayer in respect of a transaction or series of transactions that involve a sham transaction, penalties can apply to taxpayers involved and tax advisors or promoters ◦ Penalty is applied at time of assessment: taxpayers forced to file notice of objection to defend against penalties ◦ Taxpayer penalty: greater of $25, 000 and 50% of the difference between tax that would have been payable but for the sham, and the amount of tax actually paid prior to the assessment ◦ Advisor penalty: all fees received with respect to the sham transaction at issue

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 3) Measures related to “sham” transactions • 85 Prescription period: ◦ Prescription period extended an additional 3 years to issue reassessment to parties to a sham transaction ◦ Extended prescription period also applies to associated persons: may impact related entities within a corporate group ◦ Prescription period can be suspended as of time Revenu Québec seeks authorization from judge of the Court of Québec with respect to formal demand concerning unnamed persons until final settlement

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Quebec Minister of Finance – Information Bulletin 2019 -5 3) Measures related to “sham” transactions • 86 Access to public contracts ◦ Once the assessed “sham penalty” becomes final (i. e. no objection is filed or all appeal rights exhausted/final decision of a court), the taxpayers and the advisors or promoters will be listed in the register of enterprises ineligible for public contracts (RENA) by the Autorité des marchés publics ◦ Such penalties will also be taken into account in the decision-making process through which the Autorité des marchés publics may grant or deny a company the authorization to conclude contracts with a public body

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI The “sham” doctrine – renewed interest • Sham was considered in two recent decisions of the Tax Court of Canada – Cameco and Lee • Cameco • 87 ◦ Cameco is a transfer pricing case – sham was raised as an alternative argument ◦ Justice Owen in Cameco: Minister’s position “reflects a fundamental misunderstanding of the concept of sham” ◦ Under appeal by Crown Lee ◦ Lee involved “Quebec truffle” tax planning involving a Quebec trust ◦ CRA in Lee began with GAAR-based assessing position – but abandoned this position due to Court decision in similar case in Veracity – refocused arguments on validity of Quebec trust and sham ◦ CRA unsuccessful on both arguments

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI The “sham” doctrine – renewed interest • Sham doctrine not perfectly defined in tax context • Application of doctrine by tax authority fell into disuse with enactment of GAAR • Renewed interest in sham doctrine • How to distinguish sham doctrine from incomplete or ineffective transactions? • New Quebec rules create uncertainty for taxpayers and advisors as it is difficult to predict which situations the tax authorities will consider to be potential “shams” 88

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Federal Budget 2019 – employee stock option changes • • Employee stock option deduction currently available if certain conditions met: ◦ Options are granted with FMV exercise price (i. e. are not “in the money”); or ◦ Options are granted by a CCPC and shares (once options exercised) are held for at least 2 years Deduction = 50% of taxable benefit associated with option, providing “effective capital gains treatment” ◦ Caution: despite 50% deduction, taxable benefit is not technically a capital gain, but remains employment income – this can create mismatch if shares later decrease in value, as any capital loss incurred on their disposition cannot be applied against employment benefit • Employee stock options are a very popular form of executive and employee compensation • Quebec deduction generally only 25%, but can be increased to 50% for: 89 ◦ Certain corporations that claim SR&ED credits; ◦ Corporations listed on stock exchange, with more than $10 M in total wages

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Federal Budget 2019 – employee stock option changes • Budget 2019 proposes to: ◦ Limit the availability of the employee stock option deduction for high-income individuals employed at “large, long-established, mature firms” by applying a $200, 000 annual cap on employee stock option grants based on the fair market value of the underlying shares at the time that the option is granted that are eligible for the employee stock option deduction. ◦ No annual limit is contemplated for employee stock options granted by “start-ups and rapidly growing Canadian businesses. ” • The government’s stated objective in proposing these changes is to align Canada’s employee stock option tax treatment with that of the United States. • Budget 2019 does not provide any legislative proposals in respect of the limitation on employee stock option deductions. In particular, no clarity is provided with respect to the meaning of the phrases “large, long-established, mature firms” and “start-up or rapidly growing Canadian businesses. ” • In addition, Budget 2019 does not provide any guidance on whether the $200, 000 annual limit will be indexed to inflation. • Budget 2019 indicates that any new measures would only apply on a going-forward basis and will not apply to any employee stock options granted prior to the announcement of legislative proposals. Further details will be released before the summer of 2019. 90

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI Federal Budget 2019 – employee stock option changes • Planning for stock option changes ◦ Transitional rules not yet completely clear, however indication is that options granted prior to announcement of legislation will be grand-fathered ◦ Unclear whether such grants must be “fully vested” or could be subject to contingencies – must in any case be “an agreement to issue shares” ◦ Possibility to grant new options in the short term (i. e. prior to legislative announcement) in order to position favourably for grand-fathering ◦ If CCPC: granting stock options in short term and quickly exercising may also facilitate satisfaction of 2 -year holding period • Department of Finance update (May 2019): Draft legislative proposals targeted for release by June 21 • Ultimate passage could be dependent on next government • Interesting divergence in policy approach of Federal and Quebec 91 ◦ Quebec: extending 50% deduction to options of large, publicly-listed companies ◦ Federal: restricting 50% deduction for “large, long-established, mature firms”

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI New trust reporting rules – T 3 tax returns • Currently, trusts may be exempted from filing T 3 tax returns under s. 150(1. 1) if: ◦ No Part I tax for the year; and ◦ No taxable capital gain or disposition of capital property (or for non-resident trusts, no gain or disposition on TCP) • New reporting rules for taxation years that end after December 30, 2021 • New s. 150(1. 2) will override 150(1. 1) exception, and force trusts to file T 3 tax returns • 92 ◦ Applies to “express trusts” resident in Canada (or deemed resident in Canada) ◦ “Express trust” not defined, but generally refers to trusts other than a trust established by law or judgment New s. 150(1. 2) itself subject to certain exceptions, including: ◦ Trusts in existence for less than 3 months at end of year ◦ Trusts with less than $50, 000 of assets (based on FMV), if assets are cash or cash-like securities (i. e. publicly listed securities) ◦ Trusts required under rules of professional conduct (e. g. lawyer’s trust account) – however does not apply to trust accounts which are separate and maintained specifically for particular clients ◦ Registered charities ◦ Graduated rate estate ◦ Trusts governed by registered plans (RRSP, RRIF, TFSA, etc. )

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI New trust reporting rules – Information returns • Trusts required to file T 3 return (under new rules) must file information return containing name, address, date of birth, jurisdiction of residence, and taxpayer identification number for each person who: ◦ is a trustee, beneficiary, or settlor, or ◦ has the ability (through the terms of the trust or a related agreement) to exert influence over trustee decisions regarding the appointment of income or capital of the trust, such as a trust protector. • Requirement to provide information regarding the beneficiaries is met if the information is provided with respect to each beneficiary whose identity is known with reasonable effort by the person making the return. • If any beneficiary is not known or ascertainable, the person filing meets the requirement if they provide detailed information on how to ascertain who the beneficiaries are. For example, if the beneficiaries of a trust might include children who have yet to be born, the person must disclose the terms of the trust which provide this fact. • Joint Committee has made submissions about disclosure for lawyer’s trust accounts potentially breaching solicitor-client privilege. 93

JCF PROFESSIONAL DEVELOPMENT SEMINAR – POT-POURRI New trust reporting rules – Penalties • If a trust fails to make the necessary disclosures on time, penalties of $25 per day to a maximum of $2, 500; • If the failure to disclose the required trust information is done knowingly or under circumstances amounting to gross negligence or as a result of a failure to comply with a demand made by CRA, the proposed rules will impose a penalty equal to the greater of: ◦ $2, 500 or ◦ 5% of the highest amount at any time of the year of the fair market value of the trust assets. 94

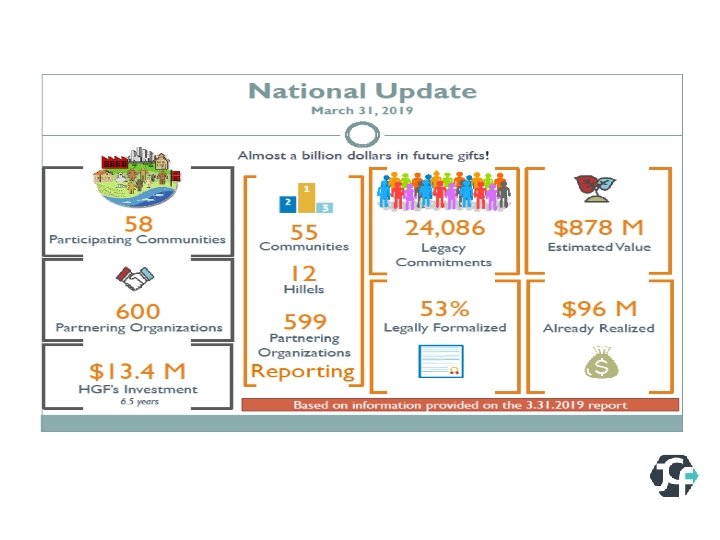

What does this mean for me? • Minimum of 540 Legacy gifts • You may be asked to leave a gift • Your clients and new clients will have questions! Numerous benefits of talking to your clients about philanthropy Endorse the program – be proactive!

Thank you!