THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA

")

(b) (c) An entity")

- Slides: 32

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA POSTGRADUATE DIPLOMA IN BUSINESS AND FINANCE - 2013/201 PRINCIPLES OF FINANCIAL AND COST ACCOUNTING Nadeeshani Dissanayake B. Sc. Accounting (Sp), First Class, ACA, ACMA, CPA (Aust)

Accounting Policies, Changes in Accounting Estimates and Errors: LKAS 8

� Key is comparability � Objectives: � How to choose accounting policies � Reporting changes in estimates � Reporting the correction of errors

IAS 8 – SELECTION AND APPLICATION OF ACCOUNTING POLICIES For a specific transaction or event First, look to the IFRS/SLFRS that deals specifically with that situation: � � � International Financial Reporting Standards, International Accounting Standards, and Interpretations developed by IFRIC or predecessor SIC Appendices and implementation guidance attached to these are an integral part of each only if stated on the specific standard. � IFRS/SLFRS standards and interpretations - top of the GAAP hierarchy � When applied – information is assumed to be relevant and reliable � What if no specific IFRS/SLFRS that applies?

� If no specific IFRS/SLFRS that applies: � Use judgment � Develop a policy that results in relevant and reliable information � Hierarchy of sources to use � IFRS/SLFRS Conceptual framework basics � If not in conflict with above, use other sources: � Pronouncements of other standard setters with similar frameworks, accounting literature, accepted industry practice, etc.

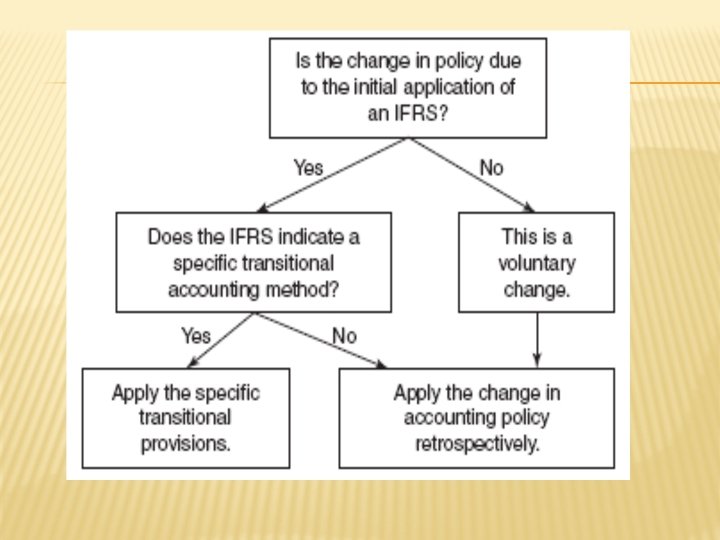

IAS 8 – CHANGES IN ACCOUNTING POLICIES � Accounting policies - � “specific principles, bases, conventions, rules and practices applied by an entity in preparing and presenting financial statements” � Source of changes in accounting policy: � required by a new or revised IFRS (most common) � voluntary change to reliable and more relevant information � Examples

� If change due to: � different economic conditions � new events or conditions � previously immaterial effects � Then NOT a change in accounting policy

l Initial application of an IFRS/SLFRS – – l Voluntary change in policy – l if transitional accounting method provided – follow it if no transitional method – retrospective application Retrospective (retroactive) application – – means apply new policy as if it had always been applied change past amounts

� Retrospective application: � for the earliest prior period presented � adjust opening balance of equity affected � adjust opening balance of other comparative amounts disclosed � Unless � impracticable to determine effects on specific prior periods or cumulative effect of change

� Impracticable: not able to determine adjustments needed after making reasonable effort, i. e. , � � effects of retroactive changes not determinable assumptions needed about management’s intentions in the prior period cannot make estimates without knowing circumstances that existed in the prior period; can only do using hindsight Example: need to estimate fair value of private company three years ago. Need to know expectations that existed then re cash flows and risk-adjusted discount rate. Not possible in many situations.

l If impracticable to apply full retrospective treatment, then – l apply the change to A, L, and equity accounts at beginning of earliest possible period for which effects are known If impracticable to determine cumulative effect even on current period opening balances, then – apply new policy prospectively

� For all changes in accounting policy, disclose � � If on application of a new/revised IFRS, also report � � nature of the change amounts of adjustments to all F/S items, EPS, and to prior periods if judged impracticable to apply retrospectively, explain why, and how applied name of IFRS, that transitional provisions are applied, any likely future effects Also disclosures about new IFRS released but not yet effective

LKAS /IAS 8 – CHANGES IN ACCOUNTING ESTIMATES � Change in accounting estimate – adjustment to carrying amount of an A/L or amount of asset consumed in period resulting from its present status and the expected future benefits/obligations associated with it. � Results from new information or new developments � If uncertain whether a change in policy or a change in estimate, account for it as a change in estimate

� Estimates are fundamental to the accounting process � Changes are expected and recurring � Therefore, account for prospectively � Prospective application – recognize effect of change in current and future periods � Disclose � Nature of the change � Amount of the change, unless effect on future periods impracticable to estimate

LKAS/IAS 8 – CORRECTIONS OF ERRORS � Prior period error – an omission or misstatement in previously reported financial statements from failing to use/misuse of reliable information that � Was available when F/S were authorized, and � Could reasonably be expected to have been used in preparing those F/S � e. g. , arithmetic mistakes, mistakes in applying accounting policies, oversights, misrepresentation of facts, fraud

� Accounting for correction of an error – � Retrospective restatement � As if error had never been made � If impracticable to determine period-specific adjustments, use partial retrospective application, or even prospective treatment (see change in accounting policy) � Disclose � Nature of the error � Amount of correction for each F/S item, EPS, and to prior periods � If judged impracticable to apply retrospectively, explain why, how applied and date from which error is corrected

PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS (LKAS 37)

DEFINITIONS �A Provision – is a liability of uncertain timing or amount � A Liability – is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic benefits. � Legal Obligation + Constructive Obligation

�A Contingent Liability – is a possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or non- occurrence of one or more uncertain future events not wholly within the control of the entity ; OR � A present obligation that arises from past events but is not recognised because , it is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation or the amount of the obligation cannot be measured with sufficient reliability.

�A contingent Assets – is a possible asset that arises from past events and whose existence will be confirmed only by occurrence or non- occurrence of one ore more uncertain future events not wholly within the control of the company

RECOGNITION � A provision shall be recognized when : (a) (b) (c) An entity has a present obligation as a result of past event; It is probable that an outflow of resources embodying economic benefits will be required to settle obligation; and A reliable estimate can be made of the amount of the obligation

� Contingent Liability – Not recognised as a liability in FS. But needs to be disclosed. � Contingent Assets - Not recognised as a asset in FS. But needs to be disclosed where an inflow of economic benefit is probable.

EXAMPLE 1 Entity A is involved in a legal dispute. A customer claims they slipped and fell at the entity premises, sustaining a back injury. The customer is seeking a damage of Rs. 1 mn. Despite the fact that customers have been successful in winning similar claims in the past, the directors of entity A believe they will be successful in defending the claim. Entity A’s lawyers have also advised that it is probable that Entity A will not be found liable. Should Entity A recognise a provision for the legal claim ?

EXAMPLE 1 CONT…. � No, a provision does not need to be recognised in Entity A’s Financial Statements � In this fact pattern, although the entity has a present obligation resulting from a past event, it is not probable that an outflow to resources would be required to settle the obligation � The event would likely be disclosed as contingent liability in the FS

EXAMPLE 2 ABC is an oil exploration company. During the year, due to a lapse in safety procedures on one of ABC’ oil rigs, there was a major oil spill. There is no environmental legislation that requires ABC to clean up the contamination caused by the oil spill. However, in recent years, ABC has widely publicised its environmental policy, which includes an undertaking to clean up any contamination that it causes. ABC engineers estimate that it will cost approximately Rs. 15 mn to rectify the damage caused by the spill � Should ABC recognise a provision for the cost of rectifying the oil spill ?

EX 2 - SOLUTION � Is there a present obligation as a result of past event ? YES � Is the outflow of economic resources probable ? YES � Can the amount be reliably measured ? YES

MEASUREMENT OF PROVISIONS � A provision is measured as follows the best estimate of expenditure required to settle the present obligation at the end of the reporting period � Best estimate The amount that an entity would rationally pay to settle the obligation at that date or to transfer it to a third party at that time. Large Population of items : expected value Single obligation : most likely amount

EX : 3 � Using the same facts as for Ex 2, ABC engineers have revised their original estimates for the cost of rectifying the damages caused by the oil spill. The engineers now believe that there is a 15% chance of the clean-up costing Rs. 10 mn 30% chance of the clean-up costing Rs. 15 mn 55% chance of the clean-up costing Rs. 20 mn What is the appropriate value of the provision recognised by ABC in its FS ?

� Solution As the oil spill is a single obligation, the individul most likely outcome should be used to provide the best estimate of the liability The individual most likely outcome is Rs. 20 mn (55% likeliehood)

EX: 4 Using the same facts as for ex – 3, except now assume that the obligation is relating to a large population of items ( ex: warranties on cars manufactured) Calculate the value of the provision to be recognised.

Provision should be estimated using the expected value method 15% * Rs. 10 mn = Rs. 1. 5 mn 30% * Rs. 15 mn = Rs. 4. 5 mn 55% * Rs. 20 mn = Rs. 11. 0 mn Total provision RS. 17 mn