THE GENERAL LEDGER Unit 3 CHAPTER 3 LEDGER

- Slides: 33

THE GENERAL LEDGER Unit 3 CHAPTER 3

LEDGER ACCOUNTS an accounting record showing all the transactions that affect a particular item The word ‘debit’ in this context simply means the left side of a ledger account, and ‘credit’ means the right side of a ledger account – neither one should be thought of as good or bad.

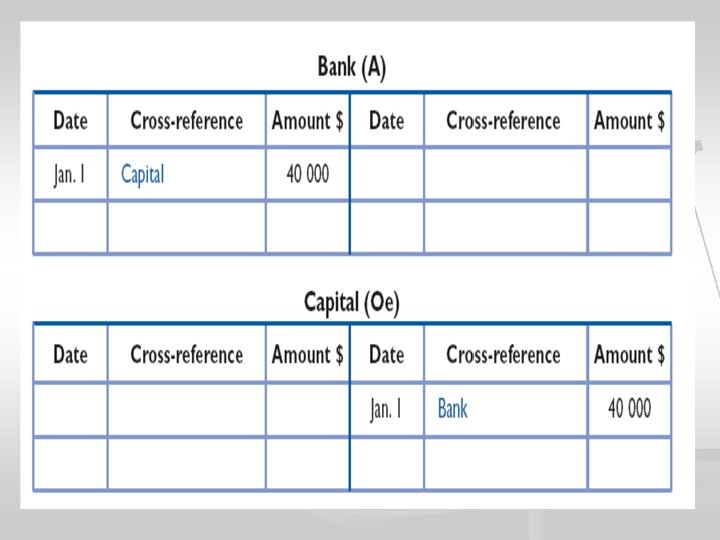

Double-entry rules Every transaction must be recorded in at least two ledger accounts Every transaction must be recorded on the debit side of one ledger account and the credit side of another

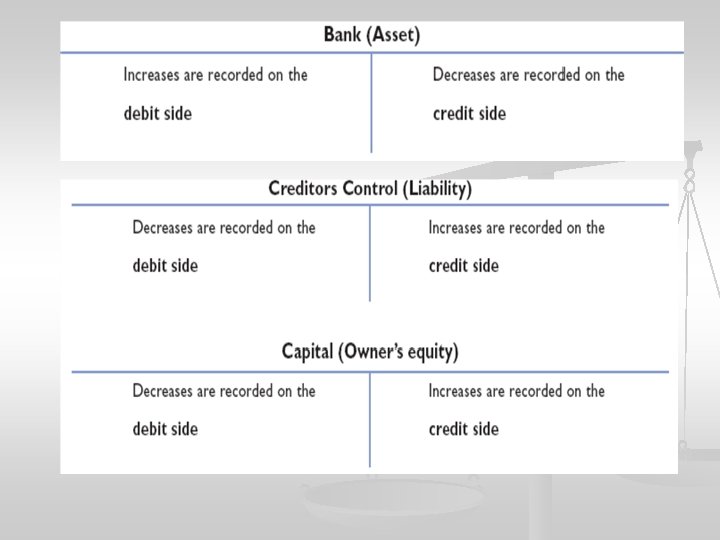

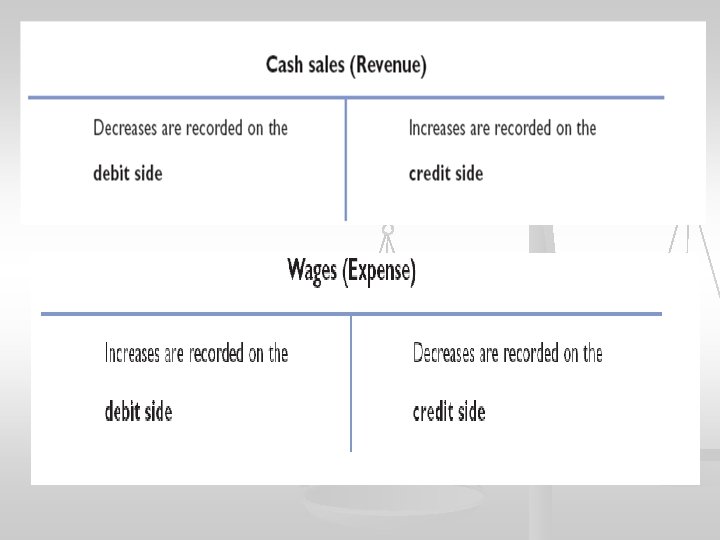

Summary of ledger entries

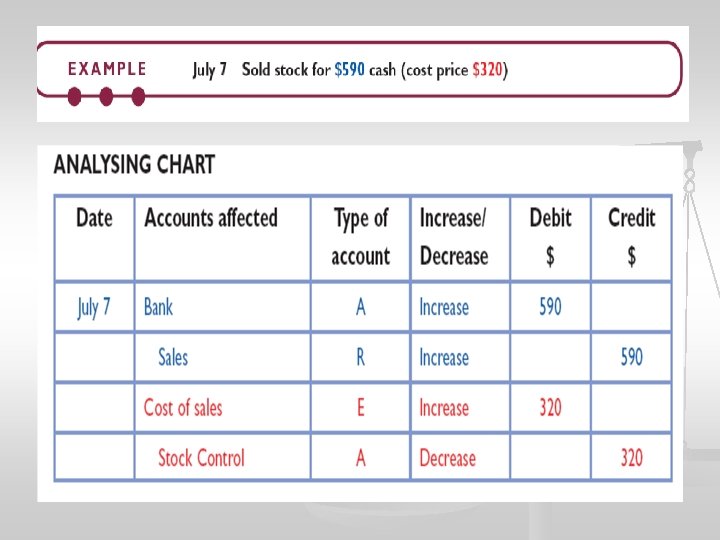

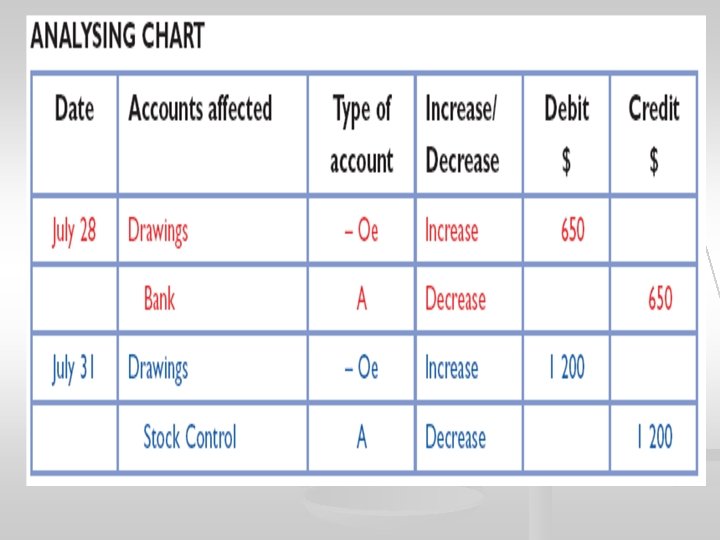

Recording procedure n n Step 1: Identify the items/accounts affected Step 2: Identify what type of accounts they are – A / L / Oe / R / E Step 3: Identify whether they are increasing or decreasing. Step 4: Use the table to identify whether the account should be debited or credited.

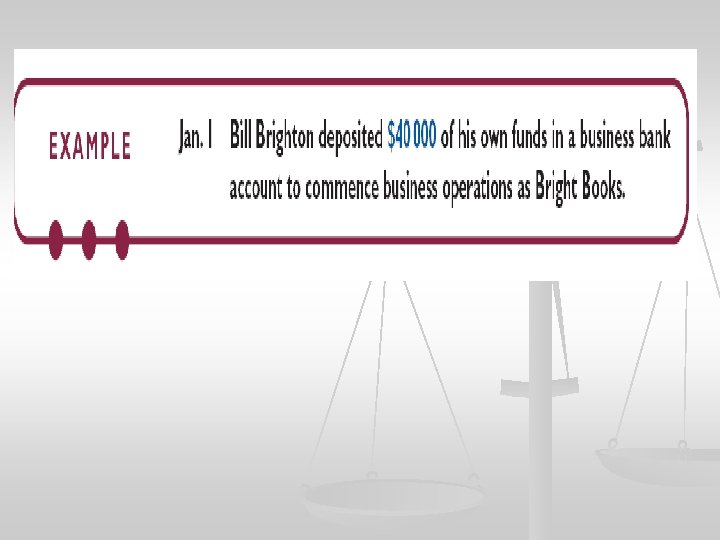

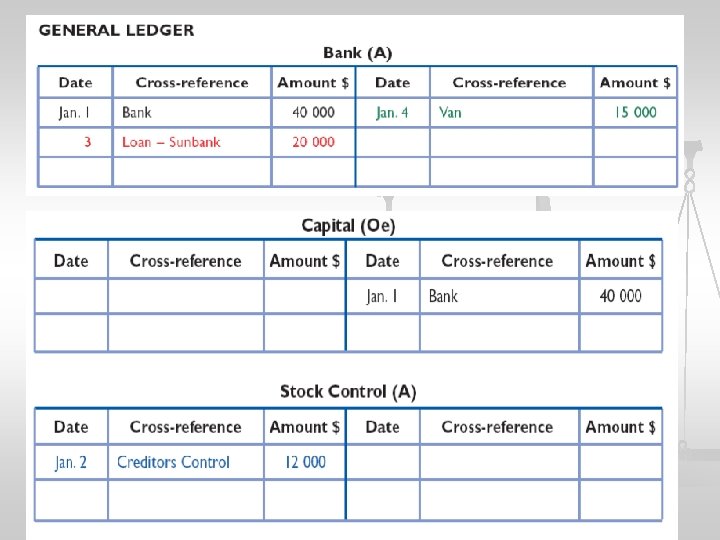

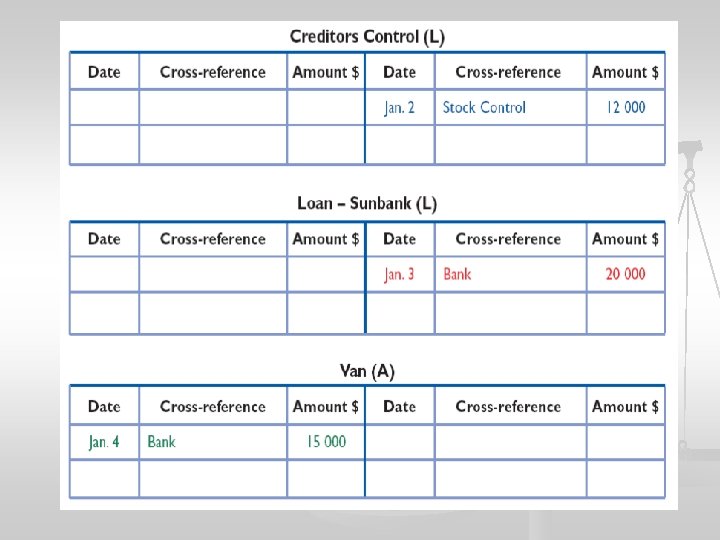

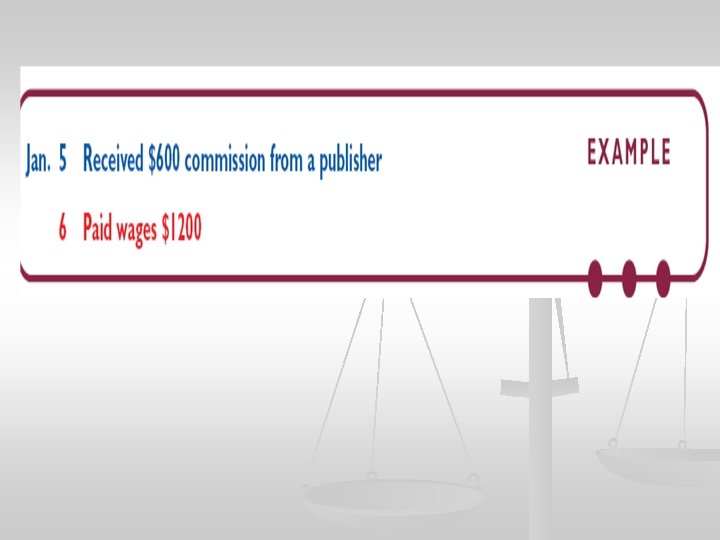

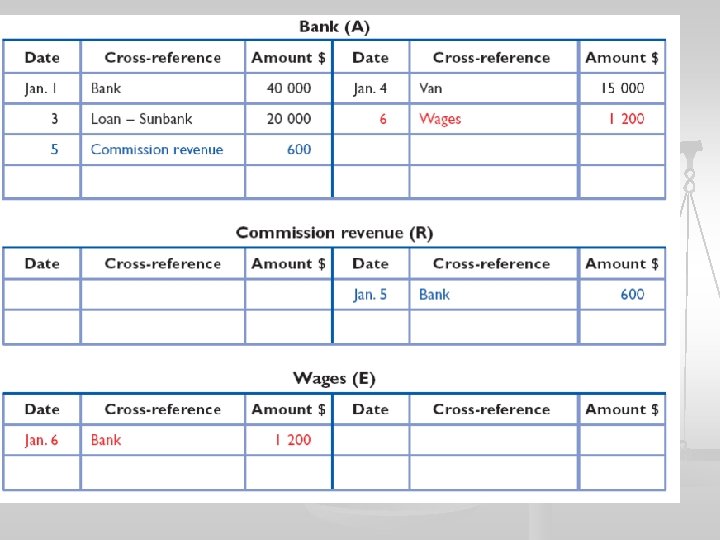

Complete the following : Jan. 2 Purchased $12 000 worth of stock on credit Jan. 3 Borrowed $20 000 from Sunbank Jan. 4 Paid $15 000 cash for a van to use for business deliveries

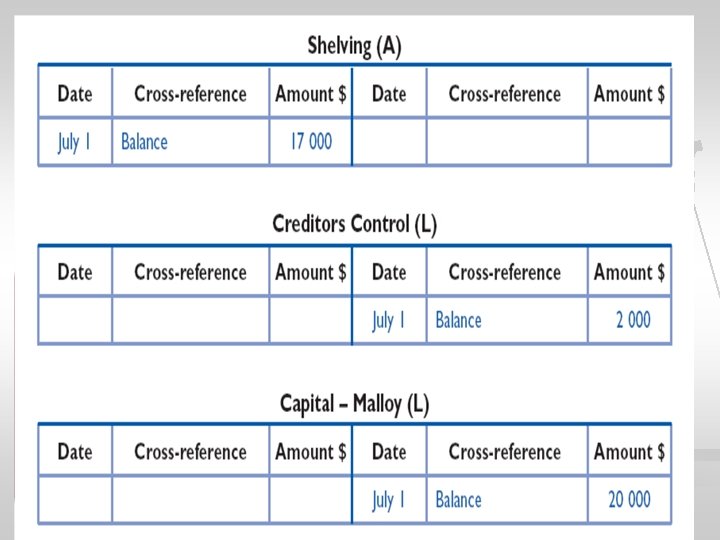

Opening balances in the General Ledger

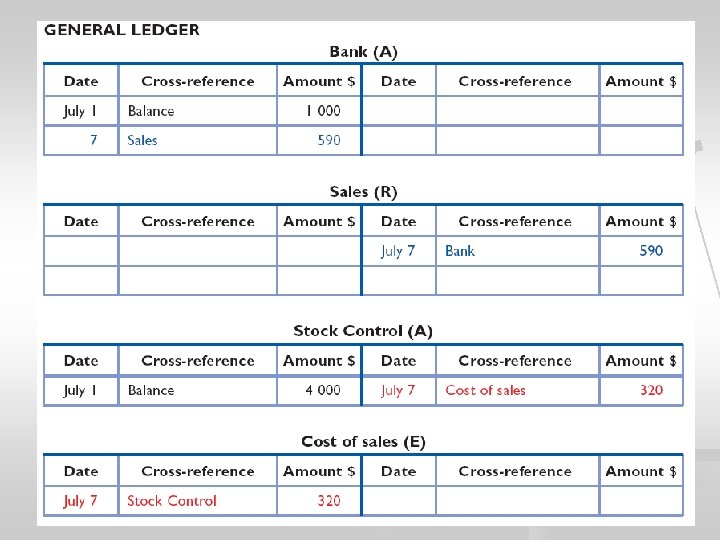

n What will be different when we sell goods on credit?

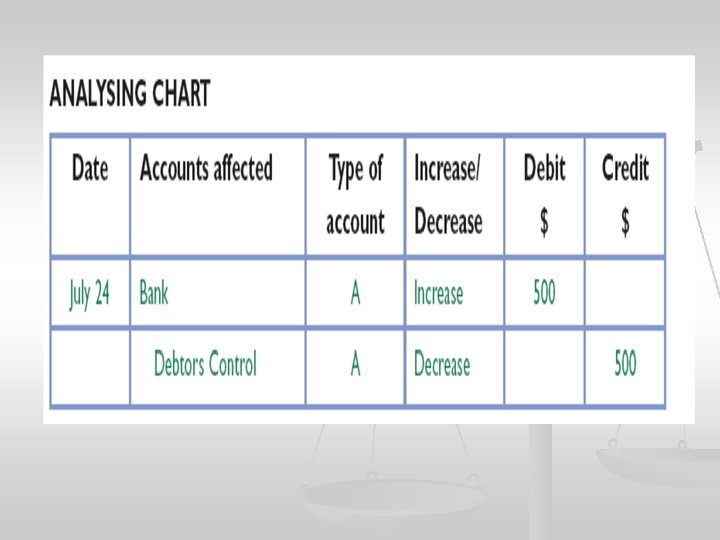

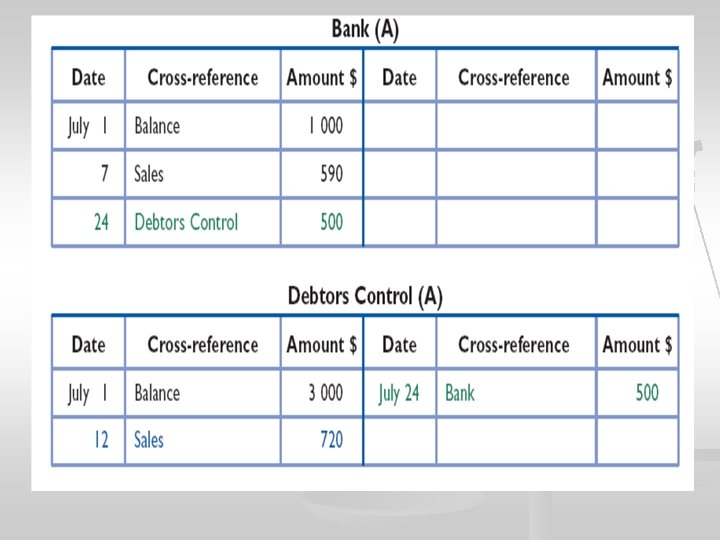

Receipts from debtors

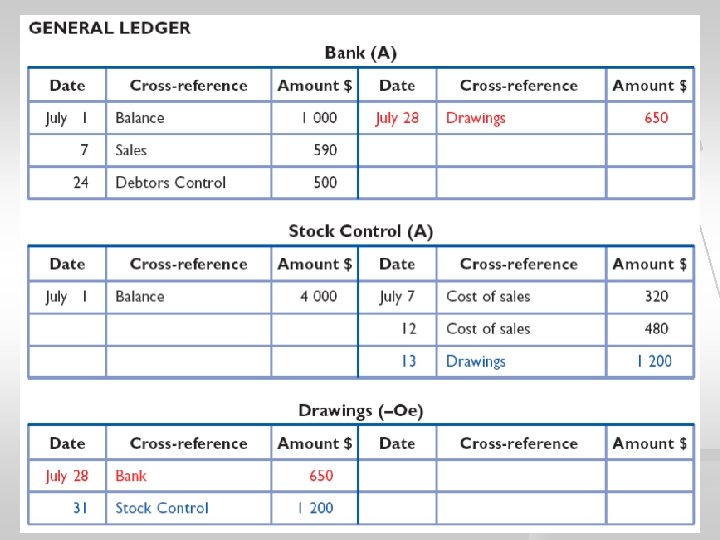

Drawings

Owner’s equity in the Balance Sheet

Footing an account Footing is the process of calculating the balance of an account and involves: 1 Adding up all the amounts on the debit side, and penciling the total below the last debit entry. 2 Adding up all the amounts on the credit side, and penciling the total below the last credit entry. 3 Deducting the smaller total from the larger total. 4 Penciling this figure – the balance – on the side of the larger total, and drawing a circle around it.

Footing an account The balance should be written in the cross-reference section

Trial Balance

Errors revealed 1 Two entries have been recorded on the same side – e. g. two debits or two credits, instead of one debit and one credit 2 Only one entry has been recorded – e. g. one debit entry without a corresponding credit entry, or vice versa 3 A different amount has been recorded on each side – e. g. $450 on the debit side, but $4500 on the credit side. In this case, the entry that has caused the difference between the two totals must be found, and corrected.

Errors not revealed 1 A transaction has been omitted all together 2 The debit and credit entries have been reversed – e. g. instead of recording a payment to a creditor by debiting Creditors Control and crediting Bank, the entry is erroneously recorded as a debit to Bank and a credit to Creditors Control 3 The transaction has been recorded in the wrong ledger accounts – e. g. instead of recording the payment of wages as a debit to the Wages account, the transaction is incorrectly debited to Rent 4 An incorrect amount is recorded on both sides of the ledger.

Balancing procedure Both footing and balancing involve calculating the balance of an account, but there are three main differences: 1 Balancing is done only at the end of the Reporting period. 2 Only asset, liability and owner’s equity accounts are balanced. (Revenue and expenseaccounts are closed – this will covered in detail in Chapter 9. ) 3 Balancing is a more formal process, involving a proper double-entry (a debit and matching credit entry).

‘Balancing’ an account