THE DOLLAR PROFITS TO INSIDER TRADING PETER CZIRAKI

and $12, 000 (mean)")

SHORT SWING PROFIT RULE “We find that insiders are 104% more likely to")

- Slides: 9

THE DOLLAR PROFITS TO INSIDER TRADING PETER CZIRAKI AND JASMIN GIDER, MARCH 2019 DISCUSSION BY PAUL ZUREK, CORNERSTONE RESEARCH

THE AUTHORS ADDRESS AN INTERESTING QUESTION Thought provoking research. The paper contributes to the literature on informational advantages of insiders and whether these insiders earn economic rents as a result of this information. Are profits earned by corporate insiders economically meaningful, in dollar terms? Prior literature has found statistically significant returns to trading by insiders, and this study asks whether these returns economically significant as measured by dollar profits. Dollar profits may be a more relevant measure of agency costs in aggregate. The authors argue that in addition to expected return from trading, trade size and frequency of trading are relevant choice variables for insiders. Key findings: $$$ profits are small; proxies for informed trading that are positively correlated with returns are negatively correlated with quantities and therefor $$$ profits.

DATA AND MEASUREMENT METHODOLOGY Form 4 reported trades from 1986 to 2013 Outright buys and sells (codes S and P) Appears to exclude transactions related to derivatives and any transactions Two approaches to measure profits: 20 day window Round-trip transactions (buys followed by sells and vice-versa) Adjust for FF 3 returns as benchmark Exclusions: unreasonable book to market values (11%), missing return histories (19%), no analyst coverage in I/B/E/S (22%); in the end, retain approximately 50% of the transactions in the database.

HAVE WE THROWN THE BABY OUT WITH THE BATHWATER? It is unlikely that outright buys and sells present a complete economic picture of an insider’s trading. E. g. , the authors find that 57% of insiders only ever sell shares. This is not surprising, because acquisition of shares through option grants would not be captured. Excluding derivative trading would be problematic if the use of derivatives is correlated with having inside information. May be excluding trading by insiders at firms where informational advantages may be most severe and where internal monitoring systems may be least developed.

KEY FINDINGS 20 -day window annual profits are $464 (median) and $12, 000 (mean) 6 -month (16(b) threshold) round-trip annual profits are $2, 530 (median) and $54, 000 (mean) All round-trip annual profits are $5, 000 (median) and $125, 000 (mean) with an average holding period of 2. 4 years 7% of insiders enjoy trading profits that exceed 10% of their compensation Are these measures of profit really that small?

WHAT WOULD ONE EXPECT TO OBSERVE? Trading on material non-public information is illegal. This suggests that insiders engaged in illegal insider trading would be unlikely to report such trading on Form 4 presumably the most profitable trades not reported Relatedly, it may be the case that insiders with information that would be expected to affect the value of the stock over a short window (such as 20 days) may be dissuaded from trading due to concerns about their trades being considered illegal insider trading would expect insiders who trade not to make significant profit in the days following the trade Consistent with the finding that informed trading proxies are negatively correlated with $$$ profits. Managers who believe their company is over or under valued and who are willing to wait for their profits are least likely to run afoul of illegal insider trading laws would expect round-trip profits to be greatest given that the average holding period is over 2 years in the data The data represent a subset of reported transactions by insiders (excluding derivatives and excluding firms with certain data availability limitations and lack of analyst coverage) this may depress observed round-trip profits by excluding firms with greater informational asymmetries between insiders and the market

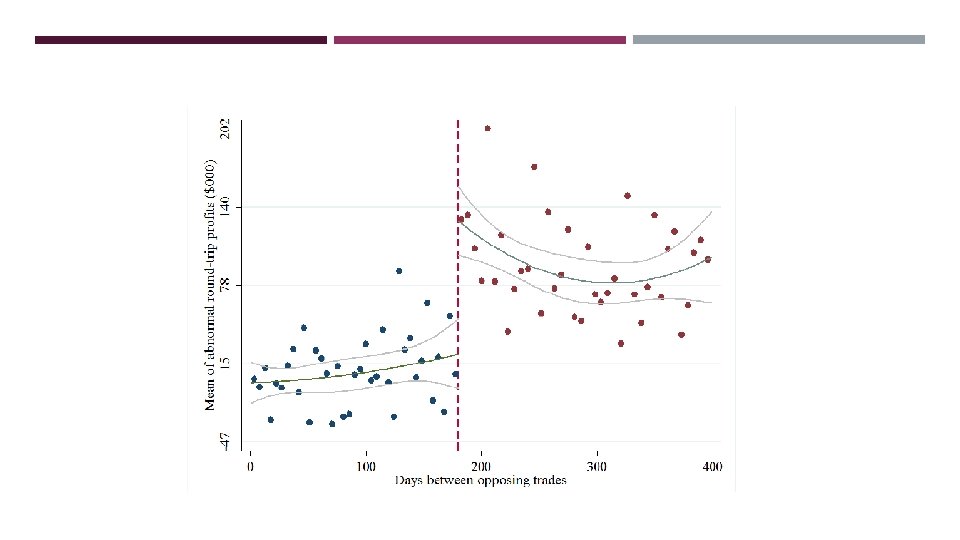

16(B) SHORT SWING PROFIT RULE “We find that insiders are 104% more likely to close round-trip trades right after the 6 -month threshold than they are right before. We also find that round-trip trades completed just after the 6 month threshold earn profits more than twice as large as trades closed just before threshold. Further, insiders who close a trade just after the 6 -month threshold trade more frequently, have higher abnormal returns, trade higher dollar values on a yearly basis, and make higher dollar profits. Thus, our novel measure does well in identifying a small set of insiders who make high profits. ” This finding is not surprising given the punitive nature of the short-swing rule. Conditional on having made a profitable trade, it would be irrational to close it out before the short swing threshold. So one would expect profitable trades to be closed out after the threshold. The results do suggest, however, that profitable trades by an insider tend to be repeated over time, which is an interesting finding.

ADDITIONAL COMMENTS While returns may not be fully informative about economic significance, the $$$ profits measure is not normalized in any way (except where the authors report findings as a fraction of compensation). It may be useful to consider presenting normalized results (e. g. , % of market capitalization). Is the SEC budget the right measure of enforcement intensity? SEC budget may not be a good measure of SEC efforts to combat illegal insider trading, which are presumably a fraction of the overall budget that may or may not vary much over time Potential endogeneity, correlating the size of the police department with crime rates