THE CHALLENGES OF CAPITAL INFLOWS INCLUDING AID Thorvaldur

")

")

")

")

- Slides: 60

THE CHALLENGES OF CAPITAL INFLOWS INCLUDING AID Thorvaldur Gylfason Joint Vienna Institute/ Institute for Capacity Development Distance Learning Course on Financial Programming and Policies Vienna, Austria NOVEMBER 26–DECEMBER 7, 2012

OUTLINE �Capital flows �History, theory, evidence �Foreign aid �Effectiveness: Does aid work? �Macroeconomic challenges Dutch disease Aid volatility

1 CAPITAL FLOWS �Definition International capital movements refer to the flow of financial claims between lenders and borrowers o The lenders give money to the borrowers to be used now in exchange for IOUs or ownership shares entitling them to interest and dividends later o �Benefits of international trade in capital Allows for specialization, specialization like trade in commodities o Allows for intertemporal trade in goods and services between countries o Allows for international diversification of risk o 3

GOODS AND CAPITAL The case for free trade in goods and services applies also to capital Trade in capital helps countries to specialize according to comparative advantage, advantage exploit economies of scale, scale and promote competition Exporting equity in domestic firms not only earns foreign exchange, but also secures access to capital, ideas, knowhow, technology But financial capital is volatile

SYMMETRY BETWEEN GOODS AND CAPITAL The balance of payments d i a s e d u l c n R = X – Z + F i X where R = change in foreign reserves X = exports of goods and services Z = imports of goods and services F = FX – FZ = net exports of capital Foreign direct investment (net) Portfolio investment (net) Foreign borrowing, net of amortization

DETERMINANTS OF TRADE IN GOODS AND SERVICES Trade in goods and services depends on Relative prices at home and abroad Exchange rates (elasticity models) National incomes at home and abroad Geographical distance from trading partners (gravity models) q Trade policy regime q q Tariffs and other barriers to trade

DETERMINANTS OF TRADE IN CAPITAL Again, capital flows consist of foreign borrowing, portfolio investment, and foreign direct investment (FDI) Trade in capital depends on q. Interest rates at home and abroad q. Exchange rate expectations q. Geographical distance from trading partners q. Capital account policy regime Capital controls and other barriers to free flows

CAPITAL FLOWS: CONCEPTUAL FRAMEWORK Emerging countries save a little Real interest rate Saving Investment Loanable funds

CAPITAL FLOWS: CONCEPTUAL FRAMEWORK Real interest rate Industrial countries save a lot Saving Investment Loanable funds

CAPITAL FLOWS: CONCEPTUAL FRAMEWORK Emerging countries Industrial countries Financial globalization encourages investment in emerging countries and saving in industrial countries Real interest rate Saving Borrowing Investment Loanable funds Lending Saving Investment Loanable funds

RELEVANCE AND CONTEXT �Since 1945, trade in goods and services has been gradually liberalized (GATT, WTO) �Big exception: Agricultural commodities �Since 1980 s, trade in capital has also been freed up �Capital inflows (i. e. , foreign funds obtained by the domestic private and public sectors) have become a large source of financing for many emerging market economies

EVOLUTION OF CAPITAL FLOWS Capital mobility A stylized view of capital mobility 1860 -2000 First era of international financial integration Return toward financial integration Capital controls Source: Obstfeld & Taylor (2002), “Globalization and Capital Markets, ” NBER WP 8846.

TOTAL CAPITAL INFLOWS (USD, BILLIONS)

CAUSES OF CAPITAL INFLOWS: PUSH VS. PULL FACTORS Capital flows result from interaction between supply and demand �Capital is “pushed” pushed away from investor countries Investors supply capital to recipients �Capital is “pulled” pulled into recipient countries Recipients demand capital from investors

CAUSES OF CAPITAL INFLOWS: PUSH VS. PULL FACTORS Internal factors “pulled” pulled capital into LDCs from industrial countries �Macroeconomic fundamentals in LDCs �More productivity, more growth, less inflation �Structural reforms in LDCs �Liberalization of trade �Liberalization of financial markets �Lower barriers to capital flows �Higher ratings from international agencies

CAUSES OF CAPITAL INFLOWS: PUSH VS. PULL FACTORS External factors “pushed” pushed capital from industrial countries to LDCs �Cyclical conditions in industrial countries �Recessions in early 1990 s reduced investment opportunities at home �Declining world interest rates made IC investors seek higher yields in LDCs �Structural changes in industrial countries �Financial structure developments, lower costs of communication �Demographic changes: Aging populations save more

EFFECTS OF CAPITAL INFLOWS: POTENTIAL BENEFITS Improved allocation of global savings allows capital to seek highest returns Greater efficiency of investment More rapid economic growth Reduced macroeconomic volatility through risk diversification dampens business cycles �Income smoothing �Consumption smoothing

EFFECTS OF CAPITAL INFLOWS: POTENTIAL RISKS I Open capital accounts may make receiving countries vulnerable to foreign shocks �Magnify domestic shocks and lead to contagion �Limit effectiveness of domestic macroeconomic policy instruments Countries with open capital accounts are vulnerable to �Shifts in market sentiment �Reversals of capital inflows May lead to macroeconomic crisis �Sudden reserve loss, exchange rate pressure �Excessive BOP and macroeconomic adjustment �Financial crisis

EFFECTS OF CAPITAL INFLOWS: POTENTIAL RISKS II � Overheating of the economy � Excessive expansion of aggregate demand with inflation, real currency appreciation, widening current account deficit � Increase in consumption and investment relative to GDP § Quality of investment suffers § Construction booms – count the cranes! Monetary consequences of capital inflows and accumulation of foreign exchange reserves depend on exchange regime § Fixed exchange rate: Inflation takes off § Flexible rate: Appreciation fuels spending boom

EPISODES OF LARGE NET PRIVATE CAPITAL INFLOWS: NUMBER, SIZE, AND ENDING Source: IMF WEO, Oct. 2007, Chapter 3, Table 3. 1.

REAL STOCK PRICES DURING INFLOW PERIODS, SELECTED COUNTRIES Chile 1978 -81 Mexico Venezuela Chile 1989 -94 Sweden Finland Year with respect to start of inflow period Note: The index for Finland, Mexico, and Sweden is shown on the left; the index for Chile during the 1980 s and 1990 s and for Venezuela is shown on the right. Source: World Bank (1997).

EARLY WARNING SIGNS Large deficits �Current account deficits �Government budget deficits Poor bank regulation �Government guarantees (implicit or explicit), moral hazard Stock and composition of foreign debt �Ratio of short-term liabilities to foreign reserves Mismatches �Maturity mismatches (borrowing short, lending long) �Currency mismatches (borrowing in foreign currency, lending in domestic currency)

RATIO OF SHORT-TERM LIABILITIES TO FOREIGN RESERVES IN ASIA 1997 n a p s n e e r G it t o id u G rule

FINANCIAL CRISES IN 1990 S CALLED CAPITAL LIBERALIZATION IN DOUBT � Financial globalization is often blamed for crises in emerging markets �It was suggested that emerging markets had dismantled capital controls too hastily, leaving themselves vulnerable � More radically, some economists view unfettered capital flows as disruptive to global financial stability �These economists call for capital controls and other curbs on capital flows (e. g. , taxes) �Others argue that increased openness to capital flows has proved essential for countries seeking to rise from lower-income to middleincome status

ROLE OF CAPITAL CONTROLS �Capital controls aim to reduce risks associated with excessive inflows or outflows � Specific objectives may include �Protecting a fragile banking system �Avoiding quick reversals of short-term capital inflows following an adverse macroeconomic shock �Reducing currency appreciation when faced with large inflows �Stemming currency depreciation when faced with large outflows �Inducing a shift from shorter- to longerterm inflows

TYPES OF CAPITAL CONTROLS � Administrative �Outright controls bans, quantitative limits, approval procedures � Market-based �Dual or �Explicit controls multiple exchange rate systems taxation of external financial transactions �Indirect taxation E. g. , unremunerated reserve requirement � Distinction �Controls inflows between on inflows and controls on outflows on different categories of capital

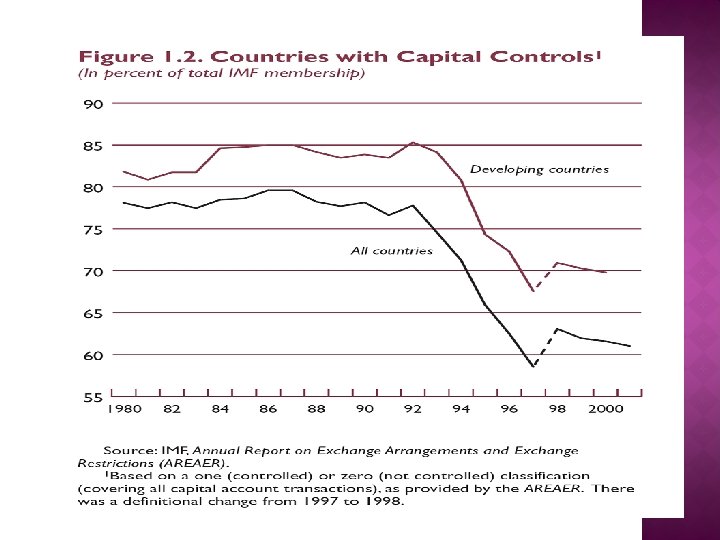

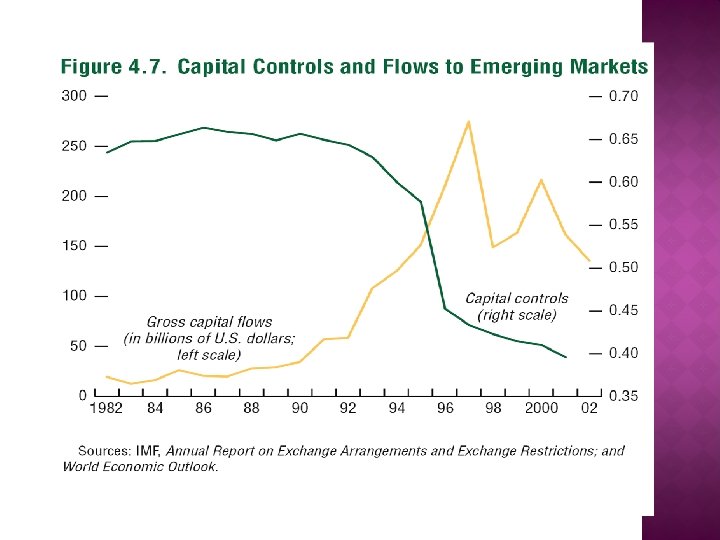

IMF ANNUAL REPORT ON EXCHANGE ARRANGEMENTS AND EXCHANGE RESTRICTIONS � IMF (which has jurisdiction over current account, not capital account, restrictions) maintains detailed compilation of member countries’ capital account restrictions � The information in the AREAER has been used to construct measures of financial openness based on a 1 (controlled) to 0 (liberalized) classification � They show a trend toward greater financial openness during the 1990 s � But these measures provide only rough indications because they do not measure the intensity or effectiveness of capital controls (de jure versus de facto measures)

CONCLUSION ON CAPITAL FLOWS �Capital flows can play an important role in economic growth and development �But they can also create macroeconomic vulnerabilities �Recipient countries need to manage capital flows so as to avoid hazards �Need sound policies as well as effective institutions, including financial supervision, and good timing

2 FROM CAPITAL INFLOWS TO AID: DEFINITION �Development aid �Unrequited transfers from donor to country designed to promote the economic and social development of the recipient (excluding commercial deals and military aid) �Concessional loans and grants included, by tradition �Grant element ≥ 25%

DEFINITION �Development aid can be �Public or private �Bilateral (from one country to another) or multilateral (from international organizations) �Program, project, technical assistance �Linked to purchase of goods and services from donor country, or in kind �Conditional in nature IMF conditionality, good governance

MOTIVATION: WHY AID? �Moral duty �Neocolonialism �Humanitarian intervention �Public good �National (e. g. , �International education and health care) Social justice to promote world unity UN aid commitment of 0. 7% of GDP �World-wide redistribution �Increased inequality word-wide �Marshall Plan after World War II 1. 5% of US GDP for four years vs. 0. 2% today Think tank in Nairobi disagrees, see www. irenkenya. com

MOTIVATION: WHY AID? �Objectives �Individuals in donor countries vs. governments in recipient countries Who should receive the aid? �Today’s poor vs. tomorrow’s poor Aid for consumption vs. investment �Conflicts �Beneficiaries’ needs �Donors’ interests

PAST TRENDS �Aid is a recent phenomenon �Four major periods since 1950 � 1950 s: Fast growth (US, France, UK) � 1960 s: Stabilization and new donors Japan, Germany, Canada, Australia � 1970 s: Rapid growth in aid again due to oil shocks, recession, cold war � 1980 s: Stagnation, aid fatigue, new methods

PAST TRENDS: 1950 S �Rapid growth of development aid �US provided 50% of total ODA �To countries ranging from Greece to South Korea along the frontier of the “Sino. Soviet bloc” �France provided 30% �To former colonies, mainly in West Africa �UK provided 10% �To Commonwealth countries

PAST TRENDS: 1960 S �Stabilization of aid from traditional donors and emergence of new donors �US contribution decreased considerably after the Kennedy presidency (1961 -63) �The French contribution decreased starting from the early 1960 s �New donors included Japan, Germany, Canada, and Australia

PAST TRENDS: 1970 S �Rapid growth in aid from industrial countries in response to the needs of developing countries due to �Oil shocks �Severe drought in the Sahel �The donor governments promised to deliver 0. 7% of GNI in ODA at the UN General Assembly in 1970 �The deadline for reaching that target was the mid-1970 s

PAST TRENDS: 1980 S AND 1990 S �Stagnation of development assistance �Donor fatigue? �Private investor fatigue?

DONOR FATIGUE? 41

WHO ARE THE DONORS? �United States: largest donor in volume, but low in relation to GDP �US aid amounts to 0. 2% of GDP �Japan: second-largest donor in volume �Nordic countries, Netherlands �Major donors to multilateral programs �Only countries whose assistance accounts for 0. 7% of GDP �EU: leading multilateral donor

WHO ARE THE DONORS? �Even though targets and agendas have been set, year after year, almost all rich nations have constantly failed to reach their agreed obligations of the 0. 7% target �Instead of 0. 7% of GNI, the amount of aid has been around 0. 4% (on average), some $100 billion short

OFFICIAL DEVELOPMENT ASSISTANCE BY DONOR 2004 (% OF GNP)

OFFICIAL DEVELOPMENT ASSISTANCE BY DONOR 2005 (USD BILLION)

MACROECONOMICS OF AID �Aid fills gap between investment needs and saving and increases growth �Poor countries often have low savings and low export receipts and limited investment capacity and slow growth �Aid is intended to free developing nations from poverty traps �Example: Capital stock declines if saving does not keep up with depreciation

AID AND INVESTMENT To understand the link between aid and investment, consider resource constraint identity by rearranging the National Income Identity: Y=C+I+G+X–Z I = (Y – T – C) + (T – G) + (Z – X) In words, investment is financed by the sum of private saving, saving public saving, saving and foreign saving

AID AND GROWTH �Poor countries are trapped by poverty �Driving forces of growth (saving, technological innovation, accumulation of human capital) are weakened by poverty �Countries become stuck in poverty traps �Aid enables poor countries to free themselves of poverty by enabling them to cross the necessary thresholds to launch growth �Saving �Technology �Human capital

AID AND POVERTY Is it feasible to lift all above a dollar a day? How much would it cost to eradicate extreme poverty? Let’s do the arithmetic (Sachs) Number of people with less than a dollar a day is 1. 1 billion Their average income is 77 cents a day, they need 1. 08 dollars Difference amounts to 31 cents a day, or 113 dollars per year Total cost is 124 billion dollars per year, or 0. 6% of GNP in industrial countries Less than they promised! – and didn’t deliver

EMPIRICAL STUDIES OF AID �Several empirical studies have assessed the impact of aid on growth, saving, and investment �The results are somewhat inconclusive �Most studies have shown that aid has no significant statistical impact on growth, saving, or investment �However, aid has positive impact on growth when countries pursue “sound policies” �Burnside and Dollar (2000)

AID AND GROWTH � Foreign aid has sometimes been compared to natural resource discoveries � Aid and growth are inversely related across countries � Cause and effect � 156 countries, 1960 -2000 r = rank correlation r = -0. 36

DOES AID WORK? THE CURRENT DEBATE �No robust relationship between aid and growth �Aid works in “countries with good policies” �Aid works if measured correctly �Distinction between fast impact aid (infrastructure projects) and slow impact aid (education) �Infrastructure: High financial returns �Education and health: High social returns

REASONS FOR THE POSSIBLE INEFFECTIVENESS OF AID I �Aid may lead to corruption �Aid may be misused, by donors as well as recipients �Donors: Excessive administrative costs �Recipients: Mismanagement, expropriation �Aid is badly distributed, sometimes for strategic reasons �Supporting opposition government against political

REASONS FOR THE POSSIBLE INEFFECTIVENESS OF AID II �Aid increases public consumption, not public investment �Aid is procyclical �When �Aid it rains, it pours leads to “Dutch disease” �Labor-intensive and export industries contract relative to other industries in countries receiving high aid inflows �Dutch disease may undermine external sustainability

REASONS FOR THE POSSIBLE INEFFECTIVENESS OF AID III �Aid volatility and unpredictability may undermine economic stability in recipient countries �Economic vs. social impact �Growth is perhaps not the best yardstick for the usefulness of aid �Long run vs. short run E. g. , increased saving reduces level of GDP in short run, but increases growth of GDP in long run

ics Online om on Ec of y ar on ti ic D ve e New Palgra See “Dutch Disease” in th DUTCH DISEASE � Appreciation of currency in real terms, either through inflation or nominal appreciation, leads to a loss of export competitiveness � In 1960 s, Netherlands discovered natural resources (gas deposits) �Currency appreciated �Exports of manufactures and services suffered, but not for long � Not unlike natural resource discoveries, aid inflows could trigger the Dutch Disease in receiving countries

AID REDUCES EXPORTS Real exchange rate Aid leads to appreciation, and thus reduces exports C B A Imports Exports plus aid Exports Foreign exchange

OIL: SAME STORY Real exchange rate Oil discovery leads to appreciation, and reduces nonoil exports C B A Imports Exports plus oil Exports Foreign exchange

MANAGEMENT OF AID FLOWS: MAIN LESSONS � Aid can play a key role in the development of recipient countries, but it can also generate macroeconomic vulnerabilities � Recipients need to implement appropriate policies to manage aid flows to avoid macroeconomic hazards �The appropriate policy response needs to take into account Potential impact of aid on competitiveness Existence of constraints to aid absorption Risks linked to aid volatility and to external debt sustainability

AID VOLATILITY AND UNPREDICTABILITY � Aid is increasingly volatile and unpredictable �Aid flows are 6 -40 times more volatile than fiscal revenue �Volatility is largest for aid dependent countries (Bulir and Hamann 2003, 2007) �Volatility increased in the 1990 s �Aid delivery falls short of pledges by over 40% � Reasons for aid volatility �Donors: Changes in priorities; administrative and budgetary delays �Recipients: Failure to satisfy conditions � IMF conditionality often guides donors, helping them decide if the country’s policies are on track

CONCLUSION ON AID THE END �Aid can play an important role in the growth and development of recipient countries … �… but it can also create macroeconomic vulnerabilities �Recipient countries need to manage aid flows so as to avoid hazards �Need to consider potential impact of aid on Competitiveness Constraints to aid absorption Risks linked to aid volatility and to external debt sustainability These slides will be posted on my website: www. hi. is/~gylfason