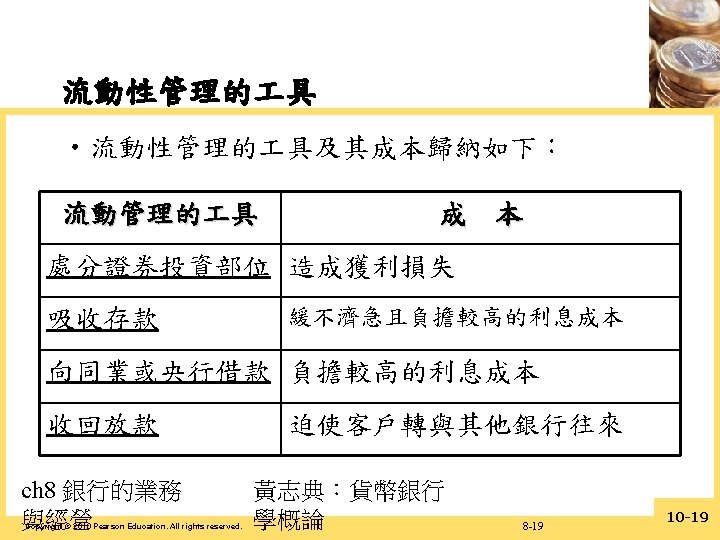

The Bank Balance Sheet Liabilities Checkable deposits Nontransaction

– Nontransaction deposits (非交易存款)")

The Bank Balance Sheet • Liabilities – Checkable deposits (支票存款) – Nontransaction deposits (非交易存款) – Borrowings (借入款) – Bank capital (銀行資本) Copyright © 2010 Pearson Education. All rights reserved. 10 -1

– Cash items in process")

The Bank Balance Sheet • Assets – Reserves (準備金) – Cash items in process of collection (託收中現金 ) – Deposits at other banks(在他行存款) – Securities (證券投資) – Loans (放款) – Other assets Copyright © 2010 Pearson Education. All rights reserved. 10 -2

of All Commercial Banks (items as a percentage of the")

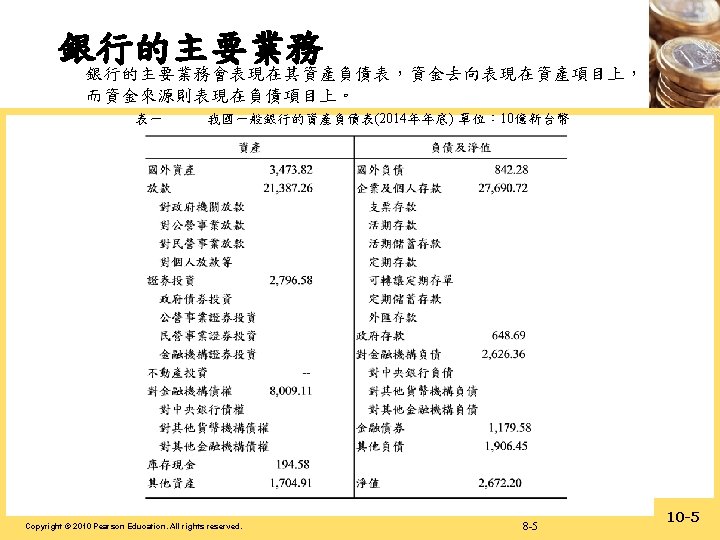

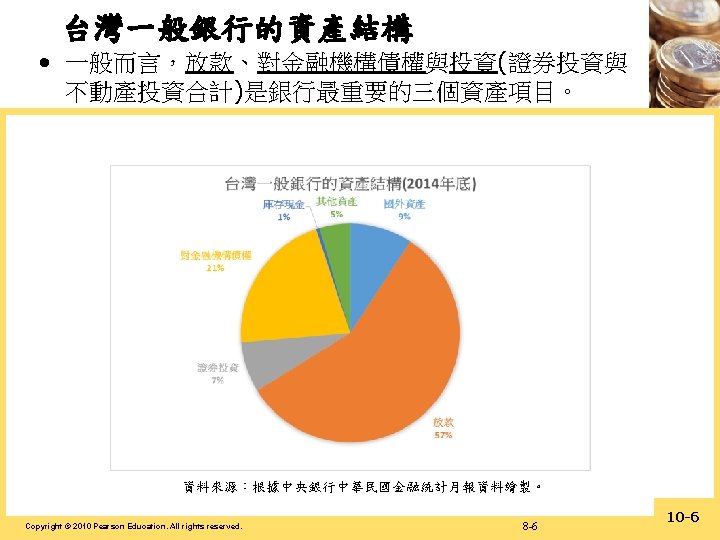

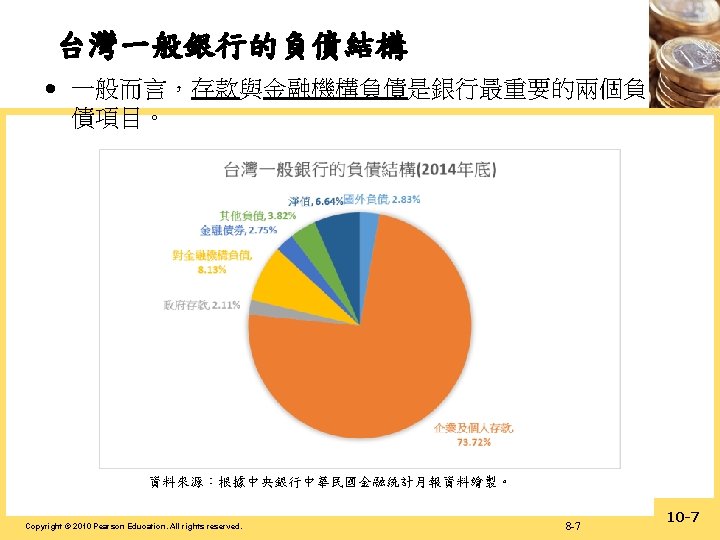

Table 1 Balance Sheet(資產負債表) of All Commercial Banks (items as a percentage of the total, December 2008) Copyright © 2010 Pearson Education. All rights reserved. 10 -3

Table 1 Balance Sheet of All Commercial Banks (items as a percentage of the total, June 2011 Copyright © 2010 Pearson Education. All rights reserved. 10 -4

Basic Banking: Cash Deposit First National Bank Assets Vault Cash +$100 First National Bank Liabilities Checkable deposits +$100 Assets Reserves +$100 Liabilities Checkable deposits +$100 • Opening of a checking account leads to an increase in the bank’s reserves equal to the increase in checkable deposits(開立支票存款帳戶+$100,同時增 加準備金+$100) Copyright © 2010 Pearson Education. All rights reserved. 10 -8

Basic Banking: Check Deposit First National Bank Assets Liabilities Cash items in +$100 process of collection Checkable deposits +$100 First National Bank Assets Reserves +$100 Second National Bank Liabilities Checkable deposits +$100 Assets Reserves Liabilities -$100 Checkable deposits -$100 Cash items in process of collection(託收中現金) Copyright © 2010 Pearson Education. All rights reserved. 10 -9

Basic Banking: Making a Profit First National Bank Assets Required reserves Excess reserves First National Bank Liabilities +$100 Checkable deposits +$90 +$100 Assets Required reserves Loans Liabilities +$100 Checkable deposits +$100 +$90 • Asset transformation(資產轉換): selling liabilities with one set of characteristics and using the proceeds to buy assets with a different set of characteristics(賣出各種性質的負債(存款)再將本 金買進不同性質的資產(放款)) • The bank borrows short and lends long (借短貸長) Copyright © 2010 Pearson Education. All rights reserved. 10 -10

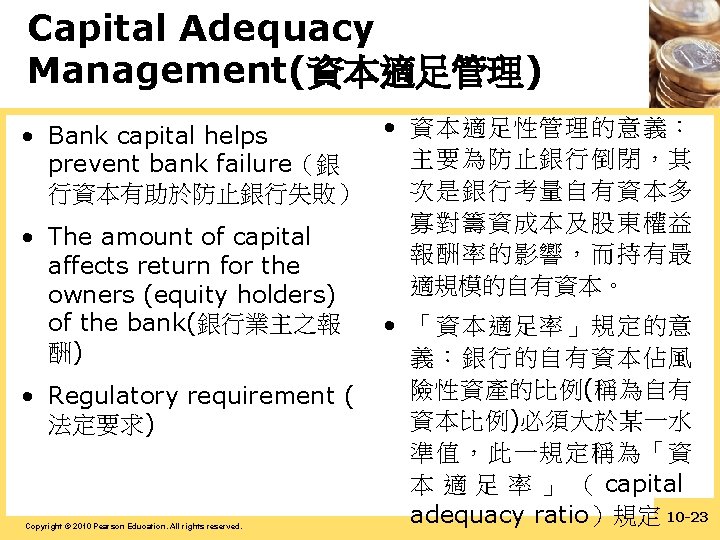

Asset Management(資產管理) Liability Management(負債管理) Capital Adequacy Management(資本適足管理)")

Bank Management • • • Liquidity Management(流動性管理) Asset Management(資產管理) Liability Management(負債管理) Capital Adequacy Management(資本適足管理) Credit Risk(信用風險) Interest-rate Risk(利率風險) Copyright © 2010 Pearson Education. All rights reserved. 10 -11

Assets Liabilities Reserves $20 M Deposits Loans $80")

Liquidity Management: Ample Excess Reserves (足夠的超額準備) Assets Liabilities Reserves $20 M Deposits Loans $80 M Bank Capital $10 M Securities $100 M $10 M Assets Liabilities Reserves $10 M Deposits $90 M Loans $80 M Bank Capital $10 M Securities • Suppose bank’s required reserves(法定準備) are 10% • If a bank has ample excess reserves, a deposit outflow does not necessitate changes in other parts of its balance sheet (存款流失不需要改變資產負債表其 他部分) Copyright © 2010 Pearson Education. All rights reserved. 10 -12

Assets Liabilities Reserves $10 M Deposits Loans $90")

Liquidity Management: Shortfall in Reserves (準備不足) Assets Liabilities Reserves $10 M Deposits Loans $90 M Bank Capital $10 M Securities $100 M $10 M Assets Reserves Loans Securities Liabilities $0 Deposits $90 M Bank Capital $10 M $90 M $10 M • Reserves are a legal requirement and the shortfall must be eliminated (準備金(的作用)是法定準備與(使 用超額準備)排除資金不足) • Excess reserves are insurance against the costs associated with deposit outflows(超額準備的作用是為 保障(免於)因存款流失所導致的成本) Copyright © 2010 Pearson Education. All rights reserved. 10 -13

Assets Reserves Liabilities $9 M Deposits $90 M Loans $90 M")

Liquidity Management: Borrowing(借入款) Assets Reserves Liabilities $9 M Deposits $90 M Loans $90 M Borrowing $9 M Securities $10 M Bank Capital $10 M • Cost incurred is the interest rate paid on the borrowed funds ((借入款)成本來自於借入資金的利息支 付) Copyright © 2010 Pearson Education. All rights reserved. 10 -14

Assets Reserves Loans Securities Liabilities $9 M Deposits $90 M")

Liquidity Management: Securities Sale(賣出證券) Assets Reserves Loans Securities Liabilities $9 M Deposits $90 M Bank Capital $90 M $1 M • The cost of selling securities is the brokerage and other transaction costs(銷售證券的成本是經紀商手續費 與其他交易成本 Copyright © 2010 Pearson Education. All rights reserved. 10 -15

Assets Reserves Liabilities $9 M Deposits Loans $90 M Borrow")

Liquidity Management: Federal Reserve(聯邦準備) Assets Reserves Liabilities $9 M Deposits Loans $90 M Borrow from Fed Securities $10 M Bank Capital $90 M $9 M $10 M • Borrowing from the Fed also incurs interest payments based on the discount rate(向聯邦準備銀行 (央行)借入資金也會引發來自於貼現窗口利率之利息支付) Copyright © 2010 Pearson Education. All rights reserved. 10 -16

Assets Reserves Liabilities $9 M Deposits Loans $81 M Bank")

Liquidity Management: Reduce Loans(放款減少) Assets Reserves Liabilities $9 M Deposits Loans $81 M Bank Capital Securities $10 M $90 M $10 M • Reduction of loans is the most costly way of acquiring reserves(以放款減少來籌措準備金所耗費的成本最高) • Calling in loans antagonizes customers(收回放款會得罪客戶) • Other banks may only agree to purchase loans at a substantial discount(其他銀行可能會同意在實質折扣下購買放款) Copyright © 2010 Pearson Education. All rights reserved. 10 -17

Asset Management: Three Goals • Seek the highest possible returns on loans and securities( 尋找放款與證券之最高可 能報酬) • 目標: • 追求放款與投資的 機會、 • 降低經營風險、 • 保持適度的流動性 • Reduce risk (降低風險) • 以獲取最大的經營 利潤。 • Have adequate liquidity(要有適度的流 動性) Copyright © 2010 Pearson Education. All rights reserved. 10 -20

Asset Management: Four Tools • Find borrowers who will pay high 主要原則: interest rates and have low • 尋找願意支付較高利息 possibility of defaulting(最高利率與最低違約可能)且違約風險低的客戶。 • Purchase securities with high returns and low risk (最高報酬與最 低風險) • 篩選出風險低、報酬率 高的證券進行投資。 • Lower risk by diversifying(越分散風 險越低) • 分散投資與放款,以降 低風險。 • Balance need for liquidity against increased returns from less liquid assets (越高報酬越低流動性的資產越 需要流動性以平衡之) • 持有流動性高的證券。 Copyright © 2010 Pearson Education. All rights reserved. 10 -21

• Recent phenomenon due to rise of money center banks (貨幣中心(大型)銀行) •")

Liability Management(負債管理) • Recent phenomenon due to rise of money center banks (貨幣中心(大型)銀行) • Expansion of overnight loan markets(隔夜拆款市場) and new financial instruments ( 新金融 具) (such as negotiable CDs(可轉讓定期存 單)) • Checkable deposits have decreased in importance as source of bank funds Copyright © 2010 Pearson Education. All rights reserved. • 負債管理的意義:積極 尋找資金來源,並監控 存款及其他負債項目的 組合與成本,以達成資 產成長的目標。 • 負債管理的 具:發行 可轉讓定期存單、推銷 存款、從事附買回交易、 發行金融債券、向同業 拆款。 10 -22

High Bank Capital Assets Low Bank Capital Liabilities")

Capital Adequacy Management: Preventing Bank Failure(防止銀行倒閉) High Bank Capital Assets Low Bank Capital Liabilities Assets Liabilities Reserves $10 M Deposits $90 M Reserves $10 M Deposits Loans $90 M Bank Capital $10 M Loans $90 M Bank Capital High Bank Capital Assets $10 M Deposits Loans $85 M Bank Capital Copyright © 2010 Pearson Education. All rights reserved. $4 M Low Bank Capital Liabilities Reserves $96 M Assets $90 M Reserves $5 M Loans Liabilities $10 M Deposits $96 M $85 M Bank Capital -$1 M 10 -24

Capital Adequacy Management: Returns to Equity Holders Copyright © 2010 Pearson Education. All rights reserved. 10 -25

Capital Adequacy Management: Safety • Benefits the owners of a bank by making their investment safe(維護投資的安全是銀行股 東權益) • Costly to owners of a bank because the higher the bank capital, the lower the return on equity(耗費股東越多的資本導致越低的資本 報酬) • Choice depends on the state of the economy and levels of confidence (根據經濟現況與信心 水準做出(最適資本)選擇) Copyright © 2010 Pearson Education. All rights reserved. 10 -26

Application: How a Capital Crunch Caused a Credit Crunch in 2008 • Shortfalls of bank capital led to slower credit growth(銀行資本不足會導致信用成長遲緩) – Huge losses for banks from their holdings of securities backed by residential mortgages(不動 產抵押貸款所擔保發行的證券). – Losses reduced bank capital (損失減縮銀行資本) • Banks could not raise much capital on a weak economy, and had to tighten their lending standards and reduce lending. (在經 濟低迷時銀行很難籌措資本,因此必須緊縮放款標 準減少放款), Copyright © 2010 Pearson Education. All rights reserved. 10 -27

and Moral Hazard(道德危險) • Screening(篩選) and Monitoring(監督 ) –")

Credit Risk: Overcoming Adverse Selection(相反選擇) and Moral Hazard(道德危險) • Screening(篩選) and Monitoring(監督 ) – Screening – Specialization in lending(貸款專門化) – Monitoring and enforcement of restrictive covenants(強制性限制條款) Copyright © 2010 Pearson Education. All rights reserved. 10 -30

and Moral Hazard(道德危險) • Long-term customer relationships(長 期的顧客關係) •")

Credit Risk: Overcoming Adverse Selection(相反選擇) and Moral Hazard(道德危險) • Long-term customer relationships(長 期的顧客關係) • Loan commitments(放款承諾) • Collateral and compensating balances (擔保品與補償存款 ) • Credit rationing(信用分配) Copyright © 2010 Pearson Education. All rights reserved. 10 -31

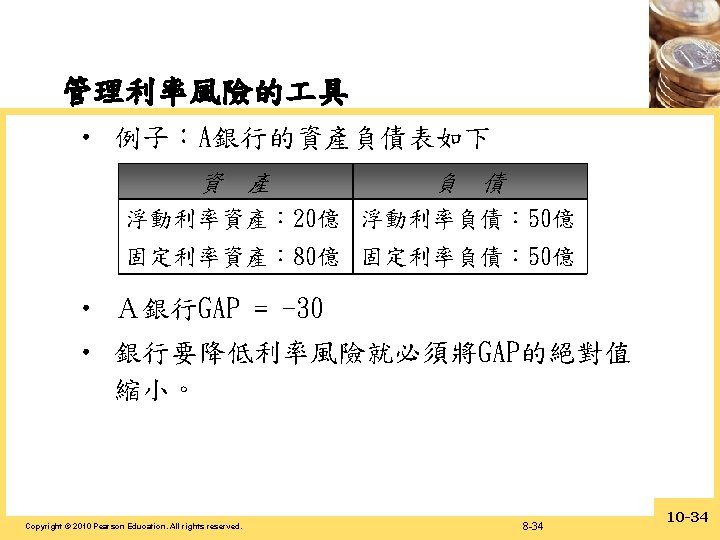

Interest-Rate Risk First National Bank Assets Rate-sensitive assets Liabilities $20 M Rate-sensitive liabilities Variable-rate and short-term loans Variable-rate CDs Short-term securities Money market deposit accounts Fixed-rate assets $80 M Fixed-rate liabilities Reserves Checkable deposits Long-term loans Savings deposits Long-term securities Long-term CDs $50 M Equity capital • If a bank has more rate-sensitive liabilities than assets(利率敏 感負債超過利率敏感資產), a rise in interest rates will reduce bank profits and a decline in interest rates will raise bank profits Copyright © 2010 Pearson Education. All rights reserved. 10 -32

• Basic gap analysis: (rate sensitive assets - rate")

Interest Rate Risk: Gap Analysis(缺口分析) • Basic gap analysis: (rate sensitive assets - rate sensitive liabilities) x interest rates = in bank profit △P (銀行的損益)= GAP ×△ i(利率變動幅度) • Maturity bucked approach – Measures the gap for several maturity subintervals. • Standardized gap analysis – Accounts for different degrees of rate sensitivity. Copyright © 2010 Pearson Education. All rights reserved. 10 -33

• Loan sales (secondary loan participation)(聯 貸) • Generation of fee")

Off-Balance-Sheet Activities (表外行為) • Loan sales (secondary loan participation)(聯 貸) • Generation of fee income(手續費收入時代). Examples: – Servicing mortgage-backed securities(MBS). (不動 產抵押貸款證券) – Bank’s acceptances (承兌)、 – loan commitment(貸款承諾) – Credit line(信用額度) Copyright © 2010 Pearson Education. All rights reserved. 10 -35

, options")

Off-Balance-Sheet Activities • Trading activities and risk management techniques – Financial futures (金融期貨), options for debt instruments (債務 具選擇權), interest rate swaps (利率交換), transactions in the foreign exchange (外匯買賣) market and speculation. – Speculation(投機) – Principal-agent problem arises (主人-代理人問題) Copyright © 2010 Pearson Education. All rights reserved. 10 -36

Off-Balance-Sheet Activities • Internal controls to reduce the principalagent problem – Separation of trading activities and bookkeeping( 交易行為與簿記分離) – Limits on exposure(限制曝險額) – Value-at-risk(風險值) – Stress testing(壓力測試) Copyright © 2010 Pearson Education. All rights reserved. 10 -37

- Slides: 38