THE ACCOUNTING EQUATION Unit 3 CHAPTER 2 The

- Slides: 10

THE ACCOUNTING EQUATION Unit 3 CHAPTER 2

The Accounting equation It must always balance Equities claims on the assets of the business

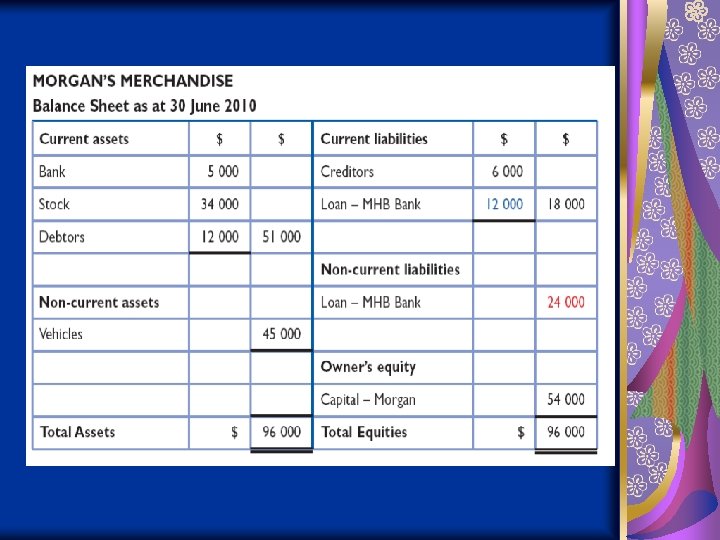

THE BALANCE SHEET an accounting report that details the business’s assets, liabilities and owner’s equity at a particular point in time

Current v. non-current assets Current asset a resource controlled by the entity as a result of past events from which a future economic benefit is expected to flow to the entity in the next 12 months Non-current asset a resource controlled by the entity as a result of past events from which a future economic benefit is expected to flow to the entity for more than 12 months

Current v. non-current liabilities Current liability a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow of economic benefits in the next 12 months Non-current liability a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow of economic benefits in more than 12 months

DOUBLE-ENTRY ACCOUNTING Rules of double-entry accounting 1 Every transaction will affect at least two items in the Accounting equation – a double entry. 2 After recording theses changes, the Accounting equation must still balance.

Imelda contributed $20 000 to establish a business bank account Dr Bank 20, 000 Cr Capital –Imelda 20, 000

Purchased stock on credit from Milano Leather Products for $45 000 Dr Stock $45, 000 Cr Creditors $45, 000

Paid $12 000 to purchase new shop fittings Dr Shop Fittings $12, 000 Cr Bank $12, 000