The 4 Common Investment Practice Mistakes which can

2) 3) 4) Treat the")

vs. Historical Total Return (HTR) � Understanding the Difference between")

� Total Return is a methodology which counts all income,")

� Historical Total Return (HTR) measures the total return realized")

Restrictive Investment Policies Behavioral: 2)")

and their")

- Slides: 61

The 4 Common Investment Practice Mistakes which can keep you and your Members from the Benefits of an Outperforming Investment Portfolio – And Actions You Can Take Now Presented by Tobias E. Timm, CIMA® Director – Investments Credit Union Investment Strategy Group Oppenheimer & Co. Inc.

Our Team Credit Union Investment Strategy Group of Oppenheimer & Co. Inc. 1400 Abbot Road East Lansing, MI 48823 (517) 333 -7791 (844) 616 -4431 Mark Wickard Managing Director – Investments Regina Wickard Director – Investments Kevin Lynch Director – Investments Elizabeth Duncan Group Analytical Associate Tobias Timm, CIMA® Director – Investments Isaiah J. Timm Associate Financial Advisor Seth Kellicut Group Marketing Associate Bryan Bell Group Business Associate

The Credit Union Investment Strategy Group

Ø Ø Ø About Me Working Exclusively with Credit Unions since 1990 Educated by John R. Brick, Ph. D of Brick & Associates in ALM principles and applications for Investment Portfolio management Educated by Frank J. Fabozzi, Ph. D, of Fabozzi Associates, and visiting fellow at Princeton & Yale Universities on development and implementation of Fixed Income Investing Graduated from Eli Broad School of Management MSU Certified Investment Management Analyst (CIMA), The Wharton School University of Pennsylvania/Investment Management Consultant Association (IMCA)

Intelligence vs. Arrogance When people call you intelligent it is almost always because they agree with you. Otherwise, they would call you arrogant. -- Nicholas Taleb Author of The Black Swan: The impact of the Highly Improbable

The 4 Common Mistakes of Investment Portfolio Underperformance 1) 2) 3) 4) Treat the Management of your Investment Portfolio as a Chore Failure to Recognize Change is Necessary for Portfolio Outperformance Missing Market Opportunities Not Getting Your Brokers’/Trading Desks’ Best Offerings (bonds) and Best Ideas (strategies)

Mistake #1: Treat The Management of your investment Portfolio as a Chore: noun § An unpleasant but necessary task.

Treating Portfolio Management as a Nuisance � Many Portfolio Managers dedicate a disproportionately small amount of time to the management of their portfolio relative to the Earnings Potential for their credit union

Time Relative to Your Balance Sheet Ratio � Are you dedicating enough of your time and resources proportionate to your Investment portfolios Earnings potential of your balance sheet?

Action: Education and Strategic Partnerships � Your Investment Portfolio is the only discretionary asset which may: § Help drive earnings § Manage balance sheet interest rate risk Without directly affecting your members while increasing your Net Income

Mistake #2: Recognizing Change is Necessary

Change � People � Loss ◦ ◦ don’t resist change…they resist loss. of: of What I know how to do Habit Certainty Security

Gardening your Portfolio…? !

Total Return Analysis (TRA) vs. Historical Total Return (HTR) � Understanding the Difference between Total Return and Historical Total Return � Most models measure an amortizing bond’s projected future performance based on a prepayment assumption, i. e. a bond’s Book Yield. This measurement ignores that bond’s past performance and its contribution to the portfolio

Total Return Analysis (TRA) � Total Return is a methodology which counts all income, both current and future. The most important variable in this calculation is the assumption of a future reinvestment rate which is an assumed rate and future value. � Total Return = Current Income + Future Income/Value

Historical Total Return (HTR) � Historical Total Return (HTR) measures the total return realized between the purchase date and present (end) date for amortizing securities. � This analysis can show the price/prepayment speed relationship has positively or negatively affected the bond’s return since its purchase.

Can too much of a good thing be a bad thing?

Credit Union Investment Performance as of Q 1/2019 3/31/19 1. 66 % 2. 13 % All CU $50 M+ Nationally 3. 07 % 3/31/19 All NY CU $50 M+ 1. 69 % 2. 15 % 3. 07 % Source: Callahan Peer to Peer 3/31/19

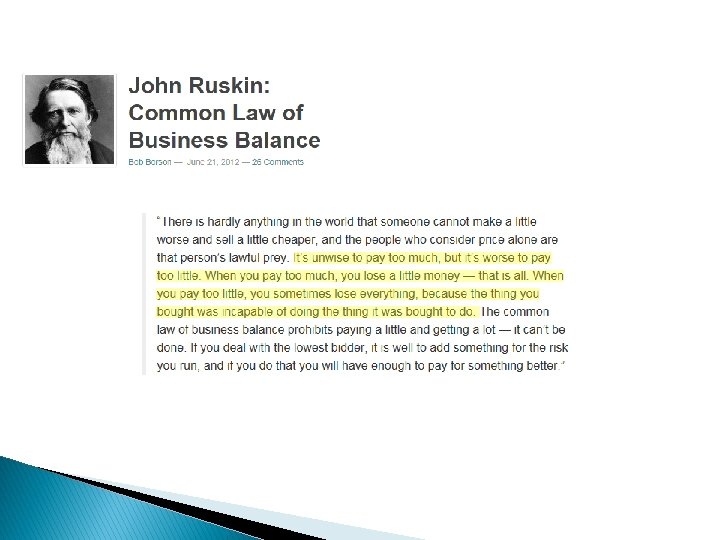

Historical Total Return � “Dollars don’t lie…” – Dr. Frank J. Fabozzi

Action: Moving from Static to Dynamic Portfolio Management � CD ladders are Optimal for Liquidity Management, however the Opportunity Cost to the Credit Union and its Members can be high � Utilize Strategically placed Amortizing and Floating Rate Investments in order to De-Risk your Balance Sheet AND Increase your Interest Income � Harnessing the Power of Historical Total Return in Managing your Portfolio by replacing your Underperforming investments with Performing investments

Mistake #3: Missing Market Opportunities

3 Common Reasons for Missing Market Opportunities Structural: 1) Restrictive Investment Policies Behavioral: 2) 3) Lack of Knowledge/Comfort to Investment Alternatives Resistance to Change

Examples of “Pre-Positioned” Investment Strategies SBA Floating Rate Pools Bank Notes Deeply Discounted Agency CMO Discounted Floater 15 yr Agency CMO Support Wes. Corp Structure Agency Inverse CMO Floater Bank Notes & Discount Agency Callable Deep Discount Agency Callable Source: Bloomberg

Examples of “Pre-Positioned” Investments � August 2008 – December 2009 : Senior Bank Notes = ◦ Great Recession – Perception of Collapse of Banking Sector � November 2008: Wescorp FCU Floating Rate Note = ◦ Unique offering (Senior to Deposits) � April 2010: Deeply Discounted Agency CMO Floaters = ◦ Anticipation of Rising Rates � March 2011: Discounted Fixed-Rate 15 yr Agency CMO (Sup) = ◦ Anticipation of Higher Prepayments on Collateral � November 2013: Agency Inverse Floating Rate CMO = ◦ Anticipation of Higher Prepayments on Collateral � October 2015: Deep Discounted Agency Callables = ◦ Anticipation of Lower Rates and Being Called � January 2016: SBA Floating Rate Pools= ◦ Anticipation of Rising Interest Rates � Fall 2018 – Spring 2019 = ◦ Senior Bank Notes and Discounted Callable Bonds

Action: Pre-Positioning for “Future Outlier” Highly Probable Events � Matching strategic opportunities in the Market with opportunistic investment security selection Investments that are “Pre-Positioned” are a Key determinant for “Portfolio Outperformance” � Utilizing

Mistake #4: Not Getting Your Brokers and their Trading Desks Offerings (bonds) and their best Ideas (strategies)

Price vs. Value-Added “The Wrong Bond at the Best Price …………Is STILL the WRONG Bond” Holistic Portfolio management utilizes the correct fit of each bond within the context of your overall portfolio strategy of balancing Liquidity vs. Income needs…

Price vs. Value-Added

What is the Value of a Strategy?

Strategy and Success � It not relying on this: is based on sound investment strategies refined over 30 years of experience

Example of the Value of Strategic Thinking S & P 500 December 1 - 24 2018 = -14. 82% S & P 500 December 24 2018 – April 30 2019 = +25. 30% U. S. 10 yr December 1 - 24 2018 = -25 bps U. S. 10 yr December 24 2018 – June 10 2019 = -60 bps Source: Bloomberg Flight to Quality. . . Fear FED Changes Course FED Discusses “Preemptive” Deflation Risks

Example of the Value of Strategic Thinking Purchased Long Term Discounted Callables and 10 yr Treasuries Purchased Discounted Inverse CMO Floaters Purchased Long Term Discounted Callables and Longer Term Bank Notes Source: Bloomberg

The Lesson as Always…

Action: Nurture a Mutually Beneficial Relationship with your Brokers/Advisors � Portfolio Management requires a thorough understanding of a combination of securities and their purpose which is essential for long term Portfolio Outperformance will get MORE …“First Looks” at the “Best Idea/Market Opportunity” from your Broker/Trading Desk � You

What should you do now?

What Are Interest-Rate Expectations for 2019 -2020 & Beyond… The DOT PLOT indicates that the FED expects the “Fed Funds Rate” to remain flat in 2019. This does NOT mean all rates across the curve will remain flat. Source: Bloomberg

What Are Interest-Rate Expectations for 2019 -2020 & Beyond… The December 2018 DOT PLOT indicated (gray line/dots) that the FED expected the “Fed Funds Rate” to rise. But the 2019 outlook is now flat. Do you see a change in the trend in the coming years? Source: Bloomberg

The 10 YR TSY Historical Interplay Between FOMC Activity and the Yield Curve Can be a Predictive Tool for Recessions 10 YR TSY = Yellow Line FED FUNDS Target = White Line Source: Bloomberg

What Can the Spread Between the 2 YR/ 10 YR Treasury Tell Us About the Economy? Yield Curve Flattening to Continue? Signal for Pending Recession? Conclusion: A Flattening/Inverted Yield Curve Can Signal a Pending Recession

Is the 10 yr Cheap or Rich? � Formula: Traditional ◦ 10 yr Yield = 1. 0 x(U. S. Inflation Rate + Real U. S. GDP) ◦ Let’s assume that a combination of factors (advances in technology, demographic trends, consequences of debt loads, central bank easing, etc. ) reduce the multiplier of 10 yr bond yields to nominal GDP from 1. 0 x to 0. 8 x. � Formula: ◦ Revised 10 yr Yield = 0. 8 x(U. S. Inflation (Y) + Real U. S. GDP (Z)) � X=2. 14% � 2. 14% (Actual), Y=1. 6% (Est. ), Z=1. 5% (Est. ) =. 08(1. 6% + 1. 5%) ∴ 2. 14% ≠ 2. 56% Source: Seabreeze Partners

Yield Curve 6/10/18 – 6/10/19

FOMC Spectrometer

FOMC Chairman Powell 6/4/2019 Here is the key segment from his speech: � “I’d like first to say a word about recent developments involving trade negotiations and other matters. We do not know how or when these issues will be resolved. We are closely monitoring the implications of these developments for the U. S. economic outlook and, as always, we will act as appropriate to sustain the expansion, with a strong labor market and inflation near our symmetric 2 percent objective. ” � � � In a surprising twist, Powell said that with the economy growing, unemployment low and inflation stable "it's time to rethink long-run strategies. " Powell also hinted that both QE and ZIRP, and perhaps NIRP are on deck, stating that interest rates so close to zero "has become the preeminent monetary policy challenge of our time, " and admitting that "perhaps it is time to retire the term 'unconventional' when referring to tools that were used in the crisis. Powell said that "my FOMC colleagues and I must—and do—take seriously the risk that inflation shortfalls that persist even in a robust economy could precipitate a difficult-to-arrest downward drift in inflation expectations. ” An even stronger statement was made by Fed Governor Richard Clarida later on CNBC. Clarida said in reference to possible slow growth amid low inflation. . . "As Chair Powell and I and others have indicated we are going to put in place appropriate policy to achieve those goals, . Whether or not that means acting preemptively or when the data comes in is just going to depend on the context at the time. "

Fed Fund Futures Probabilities

FOMC Quantitative Easing and the 10 yr U. S. Treasury QE 1: Fed Buys $100 billion of agency debt, and $500 billion of MBS QE 2: Fed Buys $600 billion of LT treasuries @ $75 billion per month Operation Twist: Fed Buys $400 billion of LT treasuries between 6 yrs – 30 yrs and sells ST between 3 mos. and 3 yrs QE 3: Fed Buys $40 billion per month of MBS Source: Bloomberg

U. S. Government 2 yr TSY 20 bps – 80 bps

U. S. Government 5 yr TSY 60 bps – 180 bps

U. S. Government 10 yr TSY 150 bps – 250 bps

So What Are My Options?

So What Are My Options? I. II. Increase Duration What If We Could De-Risk AND Increase Income? (HINT: Acquire Floating Rate Assets)

Yield is fine, “What About Risk”? 247% Less Sensitive than 1 -3 Years 620% Less Sensitive than 3 -5 Years 1073% Less Sensitive than 5 -10 Years 1687% Less Sensitive than >10 Years Less Risk & Potentially More Income in Floating Rate Investments & Loan Participations NEV Supervisory Test Asset Sensitivity Estimates Source: NCUA Guide to Using NCUA’s Interest Rate Risk Examinations Procedures Workbook

Why Differentiate Between Floating Rate & Adjustable Rate Assets? Adjustable Rate Bonds/ Loans � Infrequent and/ or Irregular Resetting Coupon Rate – Typically one year or much longer (3 -5 years) � Inferior during rising rates because they are slow/ late to react to a rising rate environment (0 -1 adjustment during 4 Fed Fund increases in 2018) � Thus, rate not as ALM or income friendly as a floating

Why Differentiate Between Floating Rate & Adjustable Rate Assets? Floating Rate Bonds/ Loans: � Frequent resetting coupon rate under 1 -year (preferably 1 -3 months) � Will react positively/ quickly to rising rates and benefit your CU from an income and earnings perspective. � Frequent friendly (1 -3 months) reset = ALM (low IRR risk)

Credit Union Investment Performance as of Q 1/2019 3/31/19 1. 66 % 2. 13 % All CU $50 M+ Nationally 3. 07 % 3/31/19 All NY CU $50 M+ 1. 69 % 2. 15 % 3. 07 % Source: Callahan Peer to Peer 3/31/19

Portfolio Composition vs. Yield on Investments CD Ladder with Larger allocation of Amortizing Securities Longer Term CD ladder with some Amortizing Securities Predominantly Short Term CD ladder Top 20% 3. 07 % Median 2. 13 % Bottom 20% 1. 66 % Source: Callahan Peer to Peer 3/31/19

What Should You Do Now? � Dedicate the time and resources for Bottom Line Focus that will help make your Credit Union more Profitable regardless of Interest Rate direction � Educate yourself/align with a strategic partner who will help you understand develop the right approach at the right time with the objective of having an outperforming investment portfolio � By identifying market opportunities and Selecting Risk Adjusted Bonds utilizing Dynamic Portfolio Management, you can Drive Higher Income on a Risk Adjusted basis thru your Income Statement!

Thank you for your time, input…and patience! Questions?

Complete our survey and receive a $10 Starbucks gift card.

Want to Learn More? For a full description or further details on these topics – Visit Us at our Exhibit Booth or you can call or email… Tobias Timm, Director (517) 333 -7791 | tobias. timm@opco. com The Credit Union Investment Strategy Group of Oppenheimer & Co. Inc.

Important Disclosures The securities mentioned in this commentary may not be suitable for all types of investors. It does not take into account the investment objectives, financial situation or specific needs of any particular client of Oppenheimer. Recipients should consider the commentary as only a single factor in making an investment decision and should not rely solely on its content as a substitution for the exercise of independent judgment of the merits and risks of investments. No representation or warranty, express or implied, is made regarding future performance of any security mentioned in this commentary. The price of the securities mentioned in this commentary and the income they may produce may fluctuate and/or be adversely affected by market variables, and investors may realize losses on investments in such securities, including the loss of investment principal. The information and statistical data contained herein have been obtained from sources which we believe to be reliable. Past performance is not indicative of future results and we do not undertake to advise you as to any change in figures or our views. Oppenheimer & Co. Inc. (“Oppenheimer”), including any of its affiliates, officers or employees, does not provide legal or tax advice. © 2019 Oppenheimer & Co. Inc. Transacts Business on All Principal Exchanges and Member SIPC. 2550042. 1