Systemic Risk and Insurance Yas Suttakulpiboon Definition Systemic

Systemic Risk and Insurance Yas Suttakulpiboon

Definition • Systemic risk means a risk of disruption in the financial system with the potential to have serious negative consequences for the internal market and the real economy. All types of financial intermediaries, markets and infrastructure may be potentially systemically important to some degree

Systemic Risk vs Financial Crisis

Systemic Risk vs Market Risk or Price Risk

Systemic risk is not the same as Systematic risk

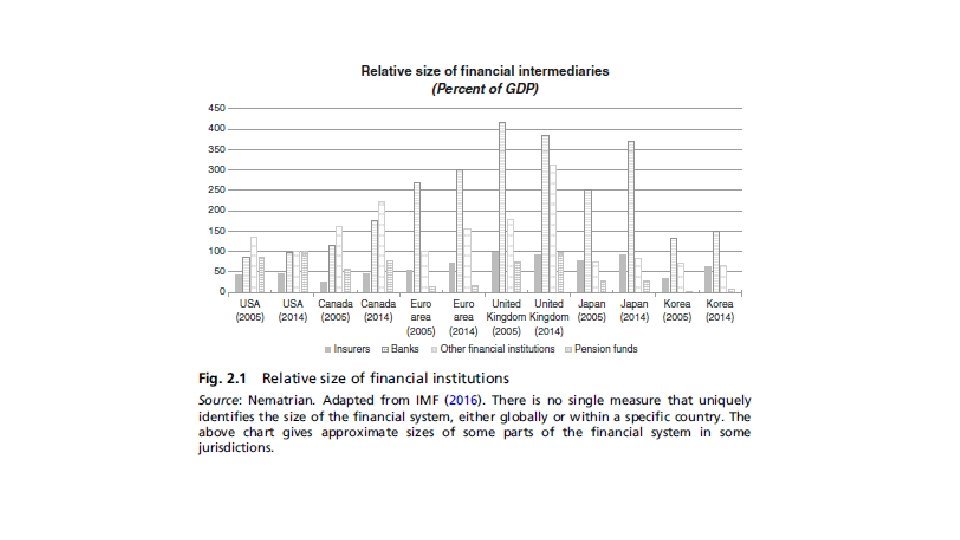

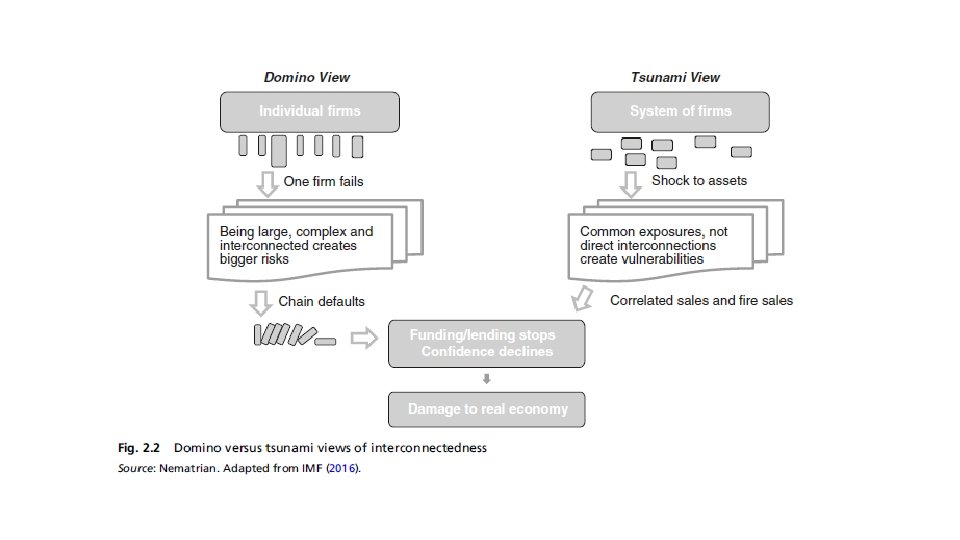

Anatomy of Systemic Risk • Size • Market share concentration • Competitive barriers to entry or how easily a product can be substituted • Interconnectedness • Complexity • Economic multiplier of all other commercial activities dependent specifically on that institution

Let’s Analyze the Systemic Risk of Insurance Companies

Terms to know TBTF TICTF G-SIFI, D-SIFI

Systemic Risk Measurement • SRISK • Co. Va. R • Pair/Vine Copula

SRISK • A financial institution represents a systemic risk if it becomes undercapitalized when the financial system as a whole is undercapitalized. • SRISK can be interpreted as the amount of capital that needs to be injected into a financial firm as to restore a certain form of minimal capital requirement.

SRISK has several nice properties: • SRISK is expressed in monetary terms and is, therefore, easy to interpret. • SRISK can be easily aggregated across firms to provide industry and even country specific aggregates. • The computation of SRISK involves variables which may be viewed on their own as risk measures, namely the size of the financial firm, the leverage (ratio of assets to market capitalization), and a measure of how the return of the firm evolves with the market

Co. Va. R • Example: What is Citibank’s 5% Va. R when JP Morgan Chase is at its 5% Va. R?

Co. Va. R • Co. Va. R simply tells us the boundary on a large loss for some institution(s), given that a particular institution is stressed to a certain degree • We need to compare the Co. Va. R measure to another “reference” measure in order to see the change in the boundary caused by institution i’s financial stress

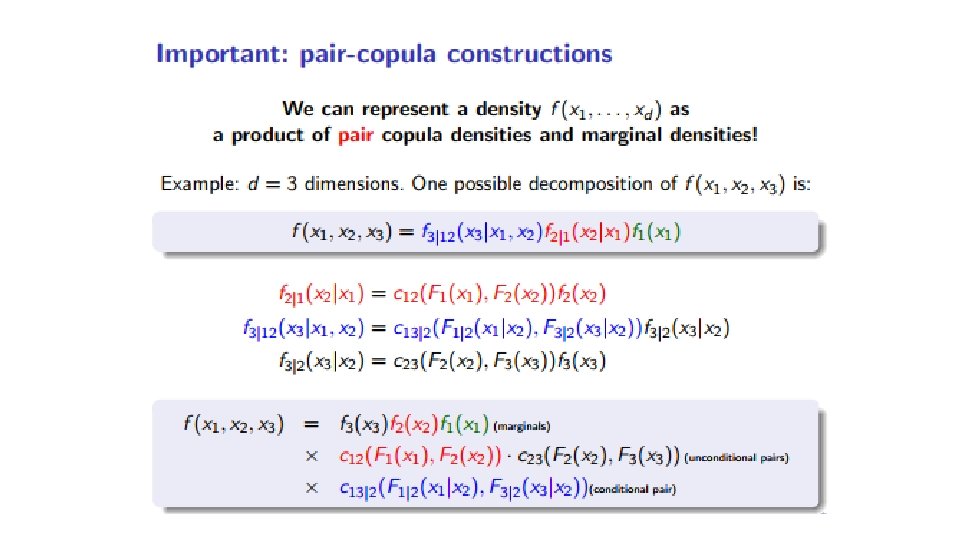

Vine Copula • Combined with bivariate copulas, regular vines have proven to be a flexible tool in high-dimensional dependence modeling. • Vines owe their increasing popularity to the fact that they leverage from bivariate copulas and enable extensions to arbitrary dimensions

Systemic Risk and Insurance: Issues to Consider

Systemic Risk and Insurance: Issues to Consider • Look at the anatomy of systemic risk… do you think “traditional” insurance companies would impose systemic risk to the economy? • MET LIFE Case • Bank run… yes! Insurance run? • Non-traditional insurers? • Shadow insurance and regulatory challenges • Can catastrophe risk be managed?

- Slides: 24