Supply Chain Finance SME DEPARTMENT BANK ALFALAH 22516

Supply Chain Finance SME DEPARTMENT , BANK ALFALAH 2/25/16

Definitions Supply Chain = Series of actors and activities needed to bring a product from production to corporate buyer. Value Chain = Series of actors and activities needed to bring a product from production to the final consumer. Value Chain Finance = Credit or other financial products, services and support services flowing to and/or through a value chain to address the needs of those actors involve in a value chain

What is Supply Chain Finance SCF is commonly perceived as a bank product structured around corporate buyer risks and, therefore, benefiting SMEs that are direct suppliers to those buyers. The small supplier benefits from the financing mechanism, which effectively allows it to achieve early payment of invoices. Meanwhile, the corporate buyer benefits from longer payment terms and a more robust supply chain. SCF in the broader definition includes inventory finance, purchase order finance, and various types of accounts receivable finance

Supply Chain Finance

Financial availability fluctuates with business activity SCF products are usually delivered by some form of revolving credit facility. This should be linked closely to supply chain transaction levels and, as activity rises and falls, credit availability also rises and falls.

SCF Approaches • Supply chain finance can be viewed as a series of tools and mechanisms. • It is also an approach that takes a systemic viewpoint, looking at the collective set of actors, processes and markets of the chain as opposed to an individual lenderborrower within the system.

• Decisions about financing value chains are based on the health of the entire value chain and not just on the individual borrower. • In value chain based finance, knowledge of the entire value chain actors is required but for conventional financing creditworthiness of the client and business in the criteria. • Value chain financing focuses more on the payments to be received from activities such as production and value-added transactions

SCF Smallholder’s Perspective • Without affordable financial services, reliable information on market demand or direct market linkages, many small farmers remain in the unprofitable trap of low-investment and low-return production cycles. • Smallholders who do have access to bank loans frequently find the terms to be too rigid, the amounts too small or fees too high to permit the kinds of investments that can significantly increase production

• In some cases, small farmers borrow their working capital from other non-financial participants within the VC (whether formal or informal), such as input suppliers, associations, buyers or traders. • While borrowing from these sources may be appropriate in some situations, it offers little transparency and can put significant constraints on financing due to the lenders’ limited liquidity and lending knowledge.

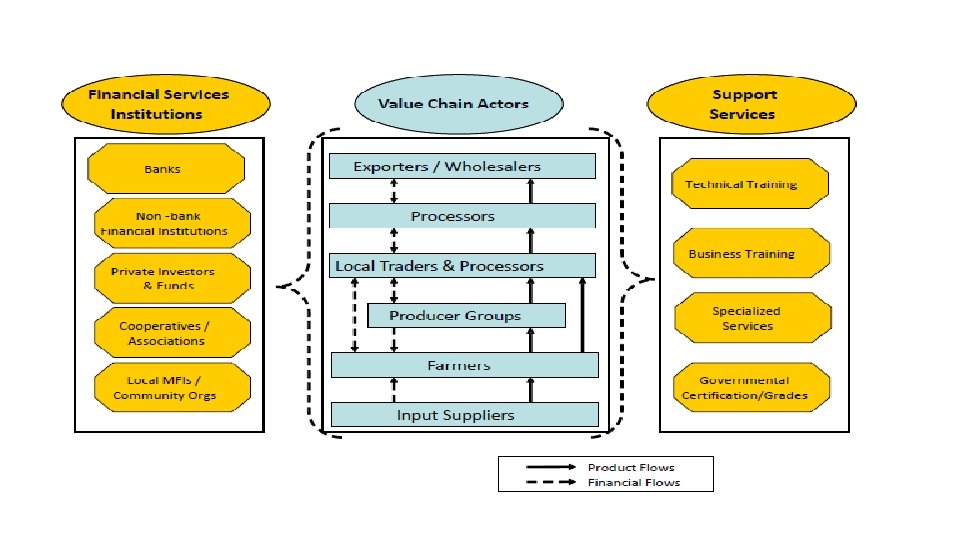

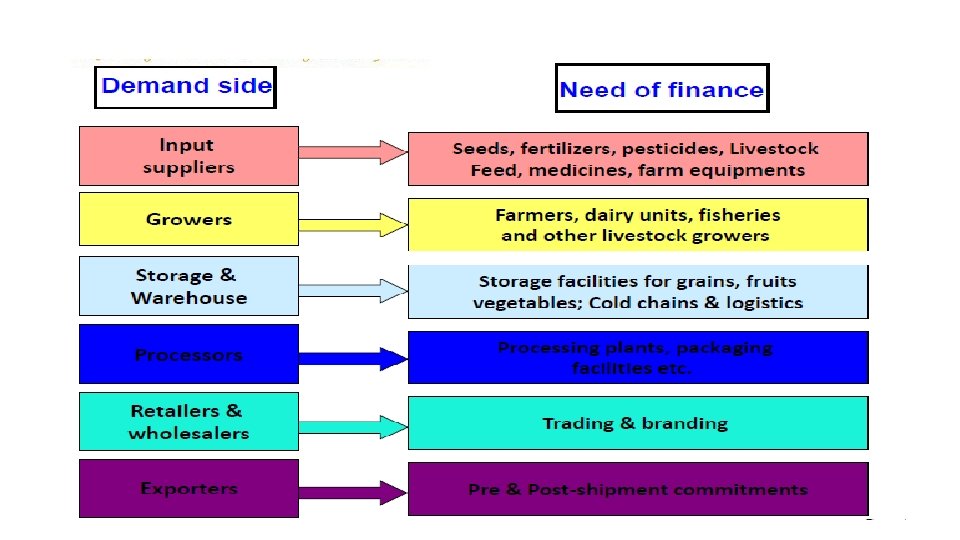

SCF – Demand Side • The demand for agriculture finance starts with the producers’ need for finance for improved technology, inputs and the labour. • The other actors in the value chain also need finance to smoothly run their business of storing, processing and facilitating the produce to reach to the consumers

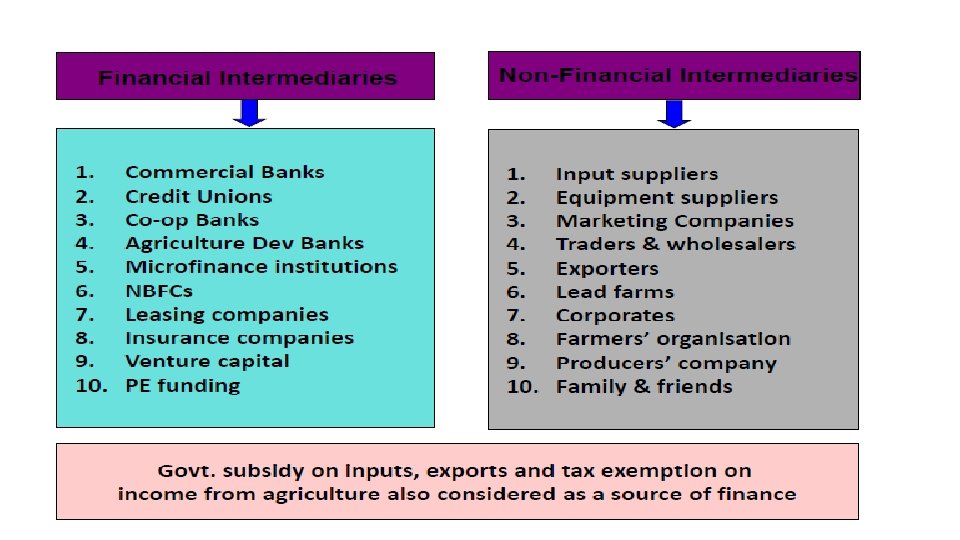

SCF – Supply Side • Both financial institutions and VC actors supply agricultural finance. • In urban areas, financial institutions tend to be the primary provider of financial services. • In rural areas, however, high transaction costs and risk associated with agricultural production keep financial institutions from playing as active a role

Facilitating Role in Potato Value Chain : BRAC, Bangladesh Payment made directly to BRAC Grading, Packaging and selling Technical support and working capital Buy back the seed produced Contract farming with marginal farmers to grow potato seeds Payment made to farmers after deducting the cost POTATO SEED DEALERS Direct Repayments Working capital loans COMMERCIAL BANKS

Examples of Supply Chain Finance in Pakistan Bill Discounting CPR Financing Grower Financing

Increasing Access to Finance Traditional SCF based on corporate buyer risk increases finance availability for SME suppliers. Through SCF SME client could get access to bank finance based on its supply chain collateral strength which they would otherwise can not be able to access.

Financial Constraints Financial intermediaries still lack desired depth in identifying the value chain and the critical actors who are still under served. • The available financial products and services are focused on stand alone financing instead of value chain. • The smallholder growers and the other actors of the chain are not getting proper attention from the financial institutions.

Benefits Supply Chain Finance can: Improve the overall effectiveness and efficiency of the value chain by: • Improving product flow and market security • Improving financing opportunities • Increasing investment and reducing risks for financing • Applying new financial products and innovation • Building stronger value chain linkages among chain actors

Benefits In Nutshell supply chain finance is a transaction-based lending approach: • It is tailored to the needs of the value chains and its recipients • Product flow and cash flow are the primary security; fixed assets are of lesser importance

- Slides: 20