Subsidary BooksI Cash Book Cash Book A cash

")

Subsidary Books-I (Cash Book)

Cash Book A cash book is a special journal which is used to record all cash receipts and cash payments. The cash book is a book of original entry or prime entry since transactions are recorded for the first time from the source documents. Cash Book will always show debit balance, as cash payments can never exceed cash available. In short, cash book is a special journal which is used for recording all cash receipts and cash payments.

Cash Book Definition The book in which all cash transactions (either cash is received or paid) are primarily recorded according to dates, is called 'Cash Book'. Features It plays a dual role. It is both a book of original entry as well as a book of final entry. All cash transactions are primarily recorded in it as soon as they take place; so it is a journal (a book of original entry). On the other hand, the cash aspect of all cash transactions is finally recorded in the Cash Book (no posting in Ledger); so a Cash Book is also a Ledger (a book of final entry). Only one aspect of cash transaction is posted to the ledger account. The other aspect ( i. e. cash aspect) needs no posting in Cash A/c. Since the Cash Book is the substitute for Cash A/c, no Cash A/c is opened in the ledger. It has two identical sides-left hand side, the debit side and right hand side, the credit side.

Features Its balance is verified by counting actual cash in the cash box. It always shows debit balance. It can never show credit balance The difference between the total of two sides shows cash in hand All the items of cash receipts are recorded on the left hand side and all items of cash payments on the right hand side in order of date. The difference between the total of two sides shows cash in hand.

Advantages 1. Saves time and labour: When cash transactions are recorded in the journal a lot of time and 2 labour will be involved. To avoid this all cash transactions are straight away recorded in the cash book which is in the form of a ledger. 2. To know cash and bank balance: It helps the proprietor to know the cash and bank balance at any point of time. 3. Mistakes and frauds can be prevented: Regular balancing of cash book reveals the balance of cash in hand. In case the cash book is maintained by business concern, it can avoid frauds. Discrepancies if any, can be identified and rectified. 4. Effective cash management: Cash book provides all information regarding total receipts and payments of the business concern at a particular period. So that, effective policy of cash management can be formulated.

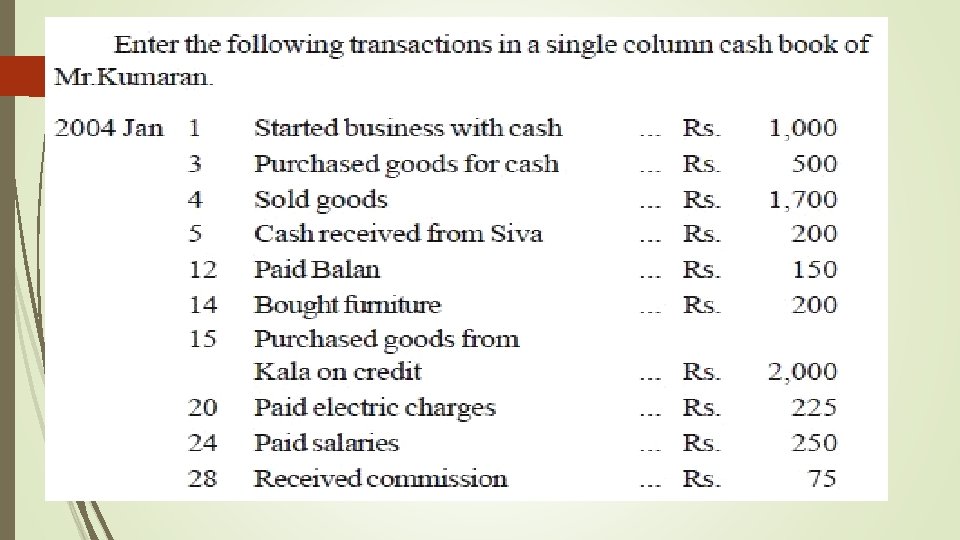

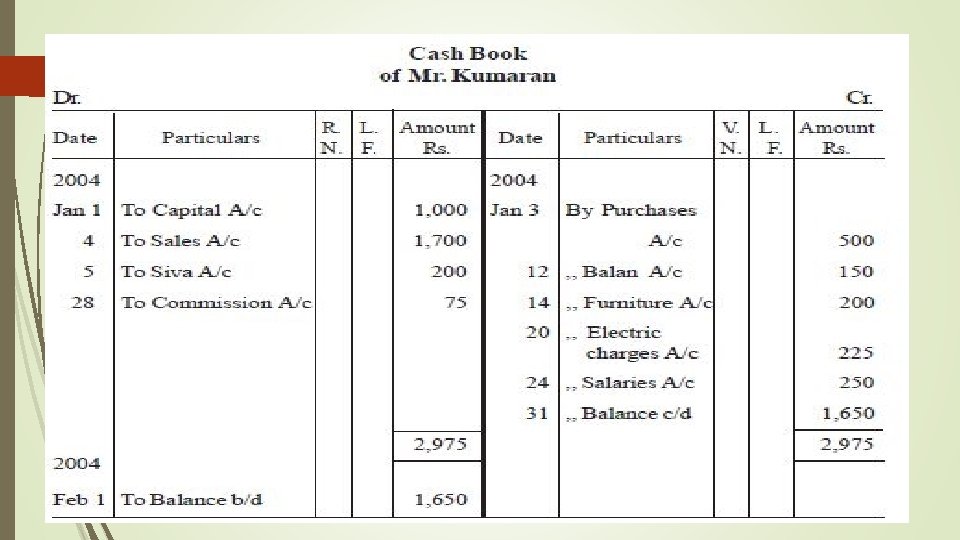

Single Column Cash Book This type of cash book is very simple because it is similar to the cash account. it has only one column on both sides. Debit side of cash book shows the all receipt and credit side shows all the payment made.

has one amount")

Single Column Cash Book Single column cash book (simple cash book) has one amount column in each side. All cash receipts are recorded on the debit side and all cash payments on the credit side. In fact, this book is nothing but a Cash Account. Hence, there is no need to open cash account in the ledger. The format of a single column cash book is given below.

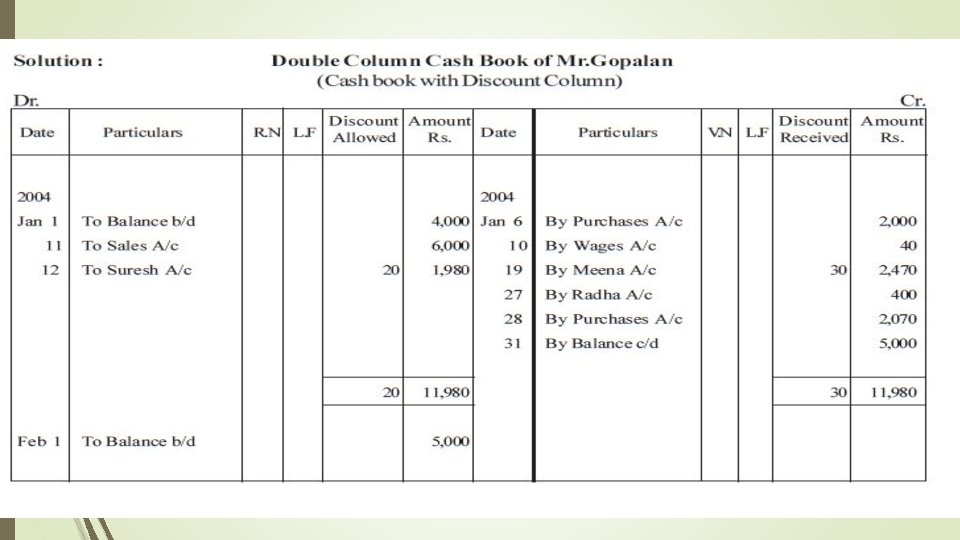

Double Column Cash Book Double Column Cashbook has a two account column on both sides of the cash book. it is three Type shown as below: Discount and Cash Column Bank and Cash Column Discount and Bank Column Cash Book is an original entry book So we need to record full transaction but in single column cash book, it is not possible to record properly of those cash transactions which are including discount account also. So we need discount and cash column cash book.

Double Column Cash Book The most common double column cash books are : i. Cash book with discount and cash columns ii. Cash book with cash and bank c 1. Cash Book with discount and cash columns On either side of the single column cash book, another column is added to record discount allowed and discount received. The format is given below columns.

Cash Discount A cash discount is a deduction allowed by the seller of goods or by the provider of services in order to motivate the customer to pay within a specified time. The seller or provider often refers to the cash discount as a sales discount. The buyer often refers to the same discount as a purchase discount. The cash discount is also known as an early payment discount.

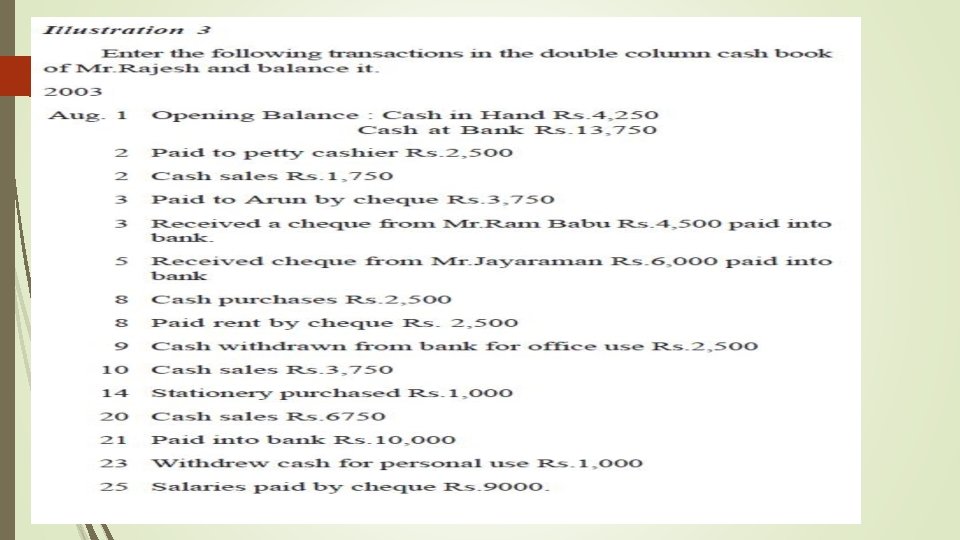

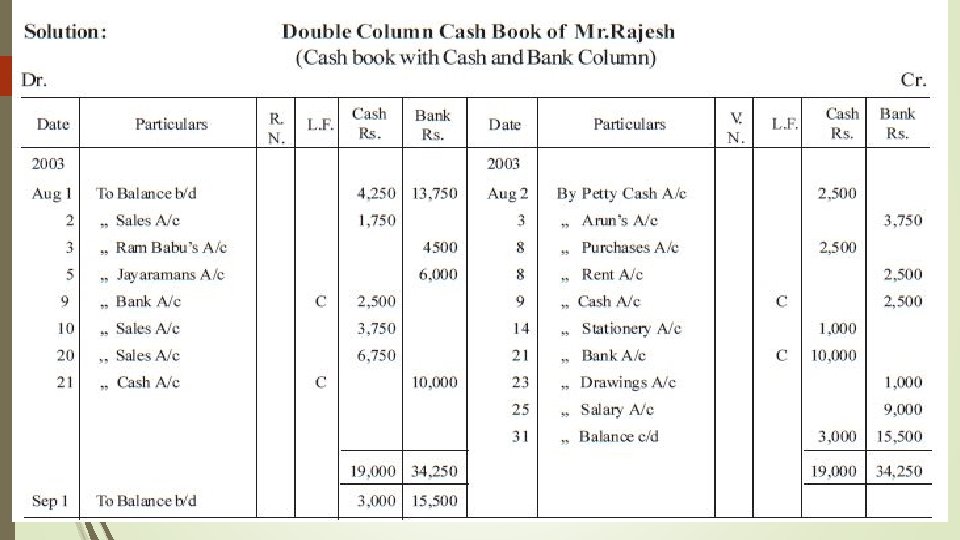

Prepare a Double Column Cash Book from the following transactions of Mr. Gopalan:

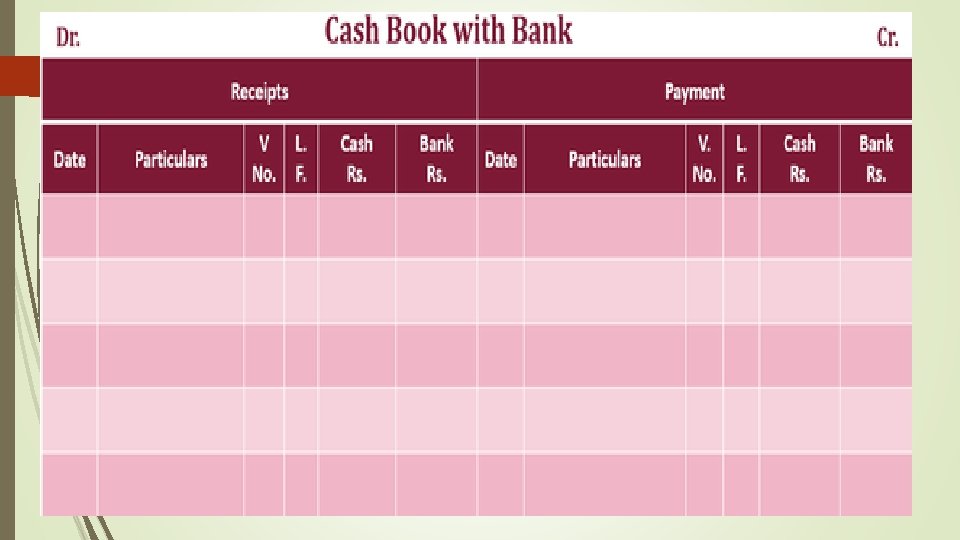

ii. Cash Book with Cash and Bank Columns When bank transactions are more in number, it is advisable to open a cash book by providing a separate column on either side of the cash book to record the bank transactions therein. In such case, it is not necessary to open a separate Bank Account in the Ledger because the two columns in the cash book serve the purpose of Cash Account and Bank Account respectively. It is a combination of Cash Account and Bank Account.

Contra Entries In the dual entry accounting system, a contra entry is an entry which is recorded to reverse or offset an entry on the other side of an account. If a debit entry is recorded in an account, it will be recorded on the credit side and viceversa. Debit and credit aspects of a single transaction are entered in the same account but in different columns. Each entry, in this case, is viewed as a contra entry of the other. Remember the word contra as “Against” or “Opposite”.

Examples of Contra Entry 1. Cash 50, 000 withdrawn for an official purpose from the bank. Journal entry for this transaction will be Cash A/C 50, 000 To Bank A/C 50, 000 In the above example, both entries, debit, and credit, are a contra entry of each other, they both offset each other. The narration is not required for such an entry and only a “C” is written in the left column which depicts that it is a contra entry.

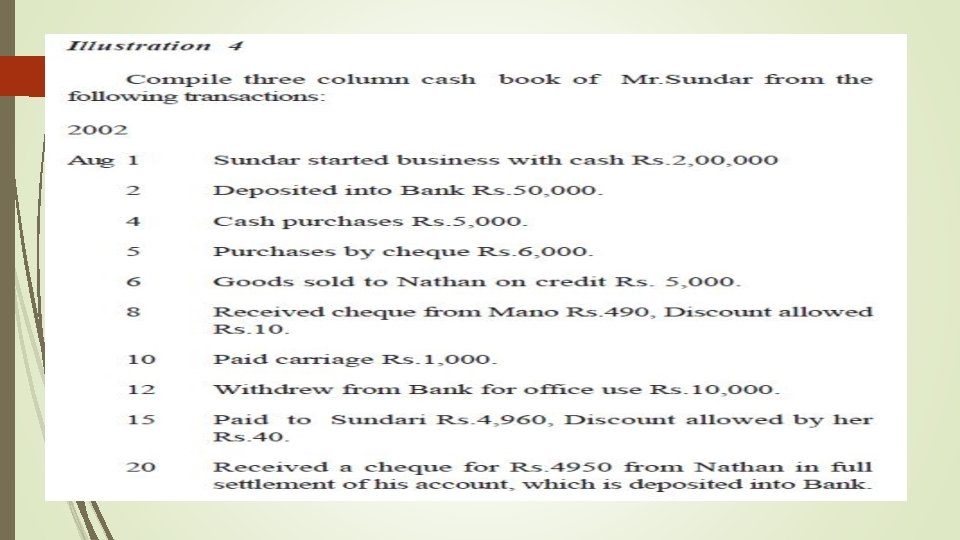

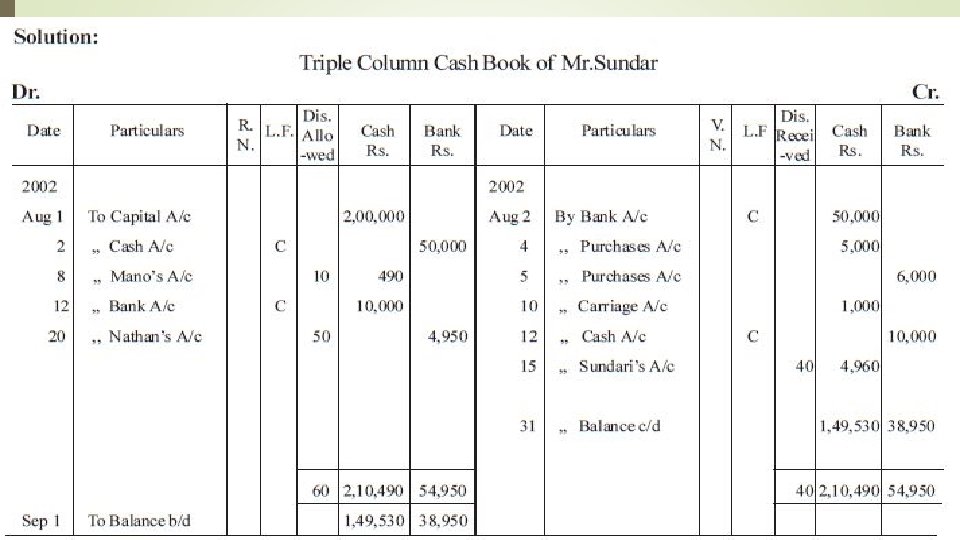

Triple Column Cash Book Large business concerns receive and make payments in cash and by cheques. Where cash discount is a regular feature, a Triple Column Cash Book is more advantageous. This cash book has three amount columns (cash, bank and discount) on each side. All cash receipts, deposits into bank and discount allowed are recorded on debit side and all cash payments, withdrawals from bank and discount received are recorded on credit side.

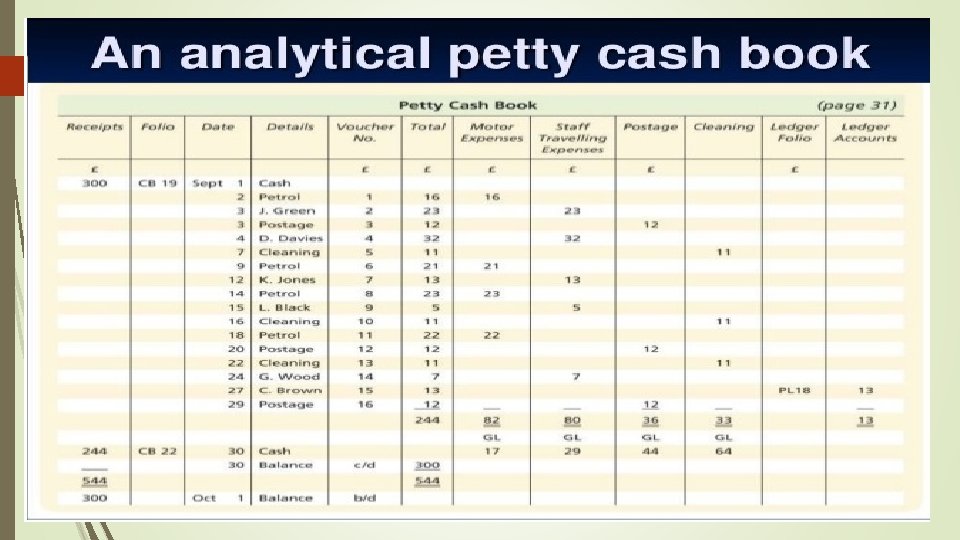

Analytical Petty Cash Book In big business apprehensions, the petty cash book is maintained in analytical form, with a detach column for each standard item of expense and a column for total. This kind of Petty Cash Book is known as Analytical Petty cash Book. This kind enables the businessman to know the information about the amount being spent on each head of petty expense. The credit side is bigger and thus has many columns. For each significant petty expense there is a detach column, and therefore columnar cash book is another name for this petty cash book. These analytical columns helps to know the actual amount spent on each and every type of petty expenses for the particular time.

Petty Cash Book It is another Cash Book which is maintained, generally, in large business concerns to reduce the burden of 'Main Cash Book', in which numerous transactions involving petty (small) amounts are recorded. For this purpose, a Petty Cashier is appointed by the Chief Cashier. The Chief Cashier advances a sum of money to the Petty Cashier to enable him to meet petty expenses for a fixed period. The Petty Cashier will record this amount on the Debit Side of the Petty Cash Book while the Chief Cashier will record the same amount on the Credit Side of the Main Cash Book. The fundamental difference between the Main Cash Book and the Petty Cash Book is that only petty expenses are recorded in the Petty Cash Book. No receipt (with the exception of money received from the Chief Cashier), however small it may be, is recorded in it. But in the main Cash Book all receipts (big and small) and large expenses are recorded.

System Of Petty Cash Accounting 1. Fixed Advance System: Under this system the Petty Cashier receives from the Chief Cashier a fixed Slim of money for a fixed period of time i. e. $200 per month. The Chief Cashier will pay $200 to the Petty Cashier every month irrespective of this that whether the Petty Cashier has spent the total sum or not. 2. Imprest System : This system is generally followed by most of the business concerns. Under this system, the total petty expenses for a particular period are estimated and that amount is advanced by the Chief Cashier to the Petty Cashier. This amount is called Imprest Cash. On the expiry of the fixed period the Petty Cashier prepares a statement of his expenses and submits it to the Chief Cashier. This statement is known as Statement of Petty, Expenses. The Chief Cashier examines the statement and if he finds it correct, hands over the Petty Cashier an amount equal to the amount actually spent. This amount plus the amount lying unspent with the Petty Cashier will be equal to the Imprest Cash.

Each petty payment is first entered in the whole payments column, and then recorded in the respective analytical column, so that: the total amount spent on each expenses for a particular period can be simply ascertained by adding up the particular column. only the periodical total of each column is posted to the ledger. the total petty payment for any period can be simply ascertained from the total payments column.

Imprest System of Petty Cash Book An imprest system of petty cash means that the general ledger account Petty Cash will remain dormant at a set amount. For example, if the petty cash custodian is entrusted with a locking bag containing $100 of currency and coins, then the Petty Cash account will always report a debit balance of $100. This $100 is the imprest balance. As long as $100 is adequate for the organization's small disbursements, then the general ledger account Petty Cash will never have an entry again. Under the imprest system, the petty cash custodian should at all times have a combination of coins, currency, and petty cash receipts equal to $100, the imprest amount.

Control occurs through the review of the petty cash receipts attached to each check request for replenishment. It also occurs by occasionally confirming that the items in the locking bag do indeed add up to the imprest amount. When the coins and currency in the locking bag get low, the petty cash custodian will request a check to replenish the coins and currency that were disbursed. Since the requested check is drawn on the organization's checking account, the Cash account (not the Petty Cash account) will be credited. The debits will go to the expense accounts indicated by the petty cash receipts, e. g. postage expense, supplies expense. In other words, the general ledger account Petty Cash is not involved in the replenishment. (Replenishment means getting the total of the coins and currency in the locking back to $100. )

in which miscellaneous")

Journal Proper Journal proper is book of original entry (simple journal) in which miscellaneous credit transactions which do not fit in any other books are recorded. It is also called miscellaneous journal. The form and procedure for maintaining this journal is the same that of simple journal. The use of journal proper is confined to record the following transactions: - § Opening entries § Closing entries § Transfer entries § Adjustment entries § Rectification entries § Entries for which there is no special journal § Entries for rare transactions

Opening Entries Opening entries are used at the beginning of the financial year to open the books by recording the assets, liabilities and capital appearing in the balance sheet of the previous year. Example: Mr. Ramnath commenced business with the following items, make the opening entries in journal proper as on 1 st January 2003.

Closing Entries Closing entries are recorded at the end of the accounting year for closing accounts relating to expenses and revenues. These accounts are closed by transferring the balances to the Trading, Profit and Loss Account. Example : Salaries paid Rs. 15, 000. Give the closing entry as on Dec. 31, 2003.

Adjusting Entries To arrive at a correct figure of profits and loss, certain accounts require some adjustments. Entries for making such adjustments are called as adjusting entries. These are needed at the time of preparing the final accounts. Example : Provide depreciation on furniture Rs. 1, 000 @ 10% per annum. Give adjustment entry as on Dec. 31, 2003.

Rectifying Entries Rectifying entries are passed for rectifying errors which might have committed in the book of accounts. Example : Purchase of furniture for Rs. 10, 000 was debited to Purchases Account. Pass rectifying entry on Dec. 31, 2003.

Miscellaneous Entries or Entries of Casual Nature These are entries of casual nature which do not occur so frequently. Such transactions include the following: i. Credit purchases and credit sale of assets which cannot be recorded through purchases or sales book ii. Endorsement, renewal and dishonour of bill of exchange which cannot be recorded through bills book. iii. Other adjustments like interest on capital and loan, bad debts, reserves etc.

The advantages of Cash book Daily cash receipts and cash payments are easily ascertained. Cash in hand at any time can easily be ascertained through Cash Book balance. Any mistake in the book can be easily detected at the time of verification of cash. Any defalcation of money can be detected while verifying cash. Since cash is verified daily, Cash Book is always kept up-to-date

Breifly explain the Imprest system of petty cash book. State merits of the system. Under this system, a round sum of money estimated as necessary for the possible needs of the business to meet petty expenses for the week or fortnight is handed over to the Petty Cashier. At the end of the fixed period or earlier, when petty cashier needs further cash, he submits the petty cash book, along with vouchers. The Chief Cashier examines the cash book with the vouchers. Then, Chief Cashier gives money/cheque for the exact amount, which he actually spent during the period. Thus, he starts for the next period with the same sum as held previously. That is, the Petty Cashier will have again the fixed sum in the beginning of the next period.

The advantages of Petty imprest book are the following : It relieves the cash book and the Chief Cashier of the burden of recording tiny and frequent payments. 2. Commission of fraud is reduced as the Chief Cashier verifies petty cash book along-with vouchers and the Petty Cashier is more responsible. 3. This method is very scientific and labour saving. The total expenditure under each column can easily be ascertained and only the periodical totals of each column need be posted to the ledger.

Describe the methods of posting cash book in the ledger l. Ledger Posting from the Debit Side of the Cash Book The debit side of the cash book records all cash receipts. The posting will be made in all the ledger accounts appearing at the debit side of the cash book. Cash has been received through these accounts; therefore cash account must have been debited. The debit side of cash book shows that cash account has been debited for all these receipts, so the accounts appearing at the debit side of the cash book must have been credited at the time of receiving cash. It is, therefore, suggested that posting in the accounts appearing at the debit side will be made at the credit side of the accounts as ‘By Cash A/c’. This is due to the fact that we cannot use the name of the same account in its own ledger account. In the previous cash book sales account, rent account and David’s account have been posted at the debit side of the cash book, so we shall be preparing these accounts through cash book and the posting will be made as under:

Posting in credit side 2. Ledger Posting from the Credit Side of the Cash Book All accounts appearing at the credit side of cash book will be separately prepared. Posting will be made to the debit side of these accounts to complete double entry record. Credit side of the cash book shows cash payment to the accounts appearing at the credit side of the cash book. Purchases account, wages account, furniture account and John ‘s account must have been debited when payment would have been made to them, so the posting will be made at the debit side of these accounts. While making posting from cash book, it should be seen, whether the particular account has been posted at the debit side or the credit side of cash book. If it is posted at the debit side of the cash book, posting will be made at credit side of the account appearing there and vice versa

When discount column is provided on either side of he cash book, why is it necessary to open a discount account in the ledger The preparation of discount allowed account and discount received account separately enables the management to know how much amount was lost or gained due to discount In brief it helps the student to remember that whenever cash is debited discount will also be debited and conversely if cash is credited so discount will also be credited This allows a person to know how much money was lost to discount and how much money was gained by discount

What is the advantage of having a cash book without cash column This leaves less chances of money being misused by the cashier which in turn leaves less chance of loss by embezzlement Columns and Bank columns represent Cash a/c and bank a/c respectively. Hence Cash a/c dr Bank a/c in the ledger need not to be opened Large bank transactions can be made easily and large transactions can be recorded at ease

What is the utility of Imprest system of petty cash 1. It relieves the cash book and the Chief Cashier of the burden of recording tiny and frequent payments. 2. Commission of fraud is reduced as the Chief Cashier verifies petty cash book along-with vouchers and the Petty Cashier is more responsible. 3. This method is very scientific and labour saving. The total expenditure under each column can easily be ascertained and only the periodical totals of each column need be posted to the ledger.

“Cash book is a journalised Ledger. ” Comment Cash book is a journal because the transactions are recorded in it for the first time from the source of document and from journal these transactions are posted to the respective account in the ledger. We can say cash book is a ledger also in the sense that it serves the purpose of cash account also. As such cash book is journal as well as ledger, and hence it may call journalised ledger.

- Slides: 45