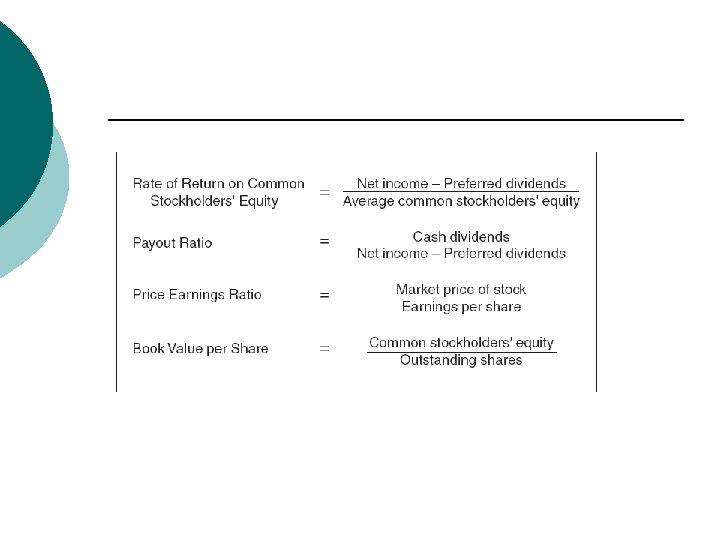

Stockholders Equity Why are we studying Stockholders Equity

x proceeds ¡")

- Slides: 18

Stockholder’s Equity

¡ Why are we studying Stockholders’ Equity l l l Owners Investments Residual Equity Required Reconciliation Statement

2. Components of Shareholders Equity Capital Stock ¡ Preferred Stock ¡ Additional Paid in Capital ¡ Treasury Stock ¡ Other changes in Assets Accounts ¡ l l l Investments Pensions Foreign Currency

Preferred Stock 1. preferred as to dividends ¡ 2. preference as to assets upon liquidation ¡ 3. convertible into common stock ¡ 4. callable at option of corporation ¡ 5. non-voting ¡

Preferred Stock ¡ Cumulative preferred l Dividends in arrears Participating preferred ¡ Convertible preferred ¡ l ¡ Participation limited Callable preferred l Call premium

Convertible Preferred Assume 500 s of $100 par sold at $120 s 1 Cash 500 x $120 60, 000 Preferred Stock 500 x 100 50, 000 Paid in Capital Preferred stock 10, 000 Assume each preferred=4 shares of CS Preferred Stock 500 x 100 Paid in Capital Preferred stock $20 Common Stock 4 x 500 x Paid in Capital PS conversion Book value Method 50, 000 10, 000 40, 000 20, 000

Preferred Stock Conversion Assume each preferred=7 shares of CS Preferred Stock 500 x 100 50, 000 Paid in Capital Preferred stock 10, 000 Retained Earnings ( 70, 00060, 000) 10, 000 Common Stock 7 x 500 x $20 Book value Method 70, 000

Preferred Stock With Warrants APB 14 ¡ PS$ = FMV-PS/ (FMV-PS+FMV-warrants) x proceeds ¡ W$ = FMV-Warrants/ (FMV-PS+FMV-warrants) x proceeds ¡ PS = 115, 192 = 119, 000/(119, 000+6, 000)x 121, 000 ¡ Warrants = 5, 808 = 6, 000/(119, 000+6, 000)x 121, 000

Preferred Stock with warrants Cash 1000 x$121 121, 000 Preferred Stock , 1000 x 100, 000 Paid in capital preferred 115, 192 - 100, 000 15, 192 Common Stock warrants 5, 808 Assume all warrants are exercised Cash 1000 x 40 40, 000 Common Stock warrants 5, 808 Common Stock 1000 x 10 10, 000 Paid in capital 35. 808

4. Treasury Stock ¡ Why? l l l Non taxable to shareholders Increase Earnings per Share Increase return on Equity To provide shares for compensation agreements To thwart take over attempts To make a market for the stock

Treasury Stock Treasury stock is not an asset ¡ Treasury stock is issued but not outstanding ¡ Accounting for Purchase ¡ l l Cost method Par value method (seldom used)

Purchase and sale of treasury Stock 1 Cash 72, 000 Common Stock 6000 x $10 60, 000 Paid in Capital 2 Treasury Stock 1, 000 s x $13 12, 000 13, 000 Cash 3 Cash 600 x $15 Treasury Stock 600 x 13 Paid in capital – Treasury Stock 13, 000 9, 000 7, 800 1, 200

Purchase and sale of treasury Stock 4 Cash 200 x $8 1600 Paid in Capital –Treasury Stock 1000 Treasury Stock 200 x $13 Analysis of PIC Treasury stock: 2600 Debit 1 Credit 1200 2 1000 Balance is now 200 credit

Purchase and sale of treasury Stock 5 Cash 100 x $10 1, 000 Paid in capital Treasury stock 200 Retained Earnings 100 Treasury Stock 100 x $13 1, 300

Retirement of Treasury Stock Common Stock 100 s x $10 1, 000 Paid in Capital Common Stock ($12, 000/6, 000 s) X 100 shares 200 Retained Earnings 100 Treasury Stock 100 x $13 $12, 000 is remaining par value 6, 000 s remaining shares 1, 300

Green Mail Black Mail? ¡ When Common stock is re-acquired at a price substantially greater than the market value l l Thwart takeover attempt Seller may agree to Restrict purchases ¡ Abandon acquisition ¡

Green Mail 6 Treasury Stock 2000 x $13 26, 000 Paid In capital Treasury Stock (NO) 0 Litigation expense settlement 2000 26, 000 x $13 Cash 2, 000 x 26 52, 000