Sources of Government Revenue The Economics of Taxation

part of the Treasury Department")

- Slides: 38

Sources of Government Revenue

The Economics of Taxation : Economic Impact of Taxes • Taxes/Other government revenues affect: – resource allocation, – consumer behavior, – nation’s productivity – Growth

Economic Impact of Taxes : Resource Allocation • Affects factors of production • A TAX placed on a good at the factory = rise in production cost • Supply curve shifts to the left • If demand stays the same = equilibrium price goes op

Economic Impact of Taxes: Behavior adjustment • TAXES affect the economy – Encourage or discourage certain activities – SIN Tax: high percentage tax that raises revenue while reducing consumption of a socially undesirable product

Economic Impact of Taxes: Productivity and Growth • Taxes affect productivity and economic growth: – Change incentives to save, invest, and work • Why people favor lower taxes….

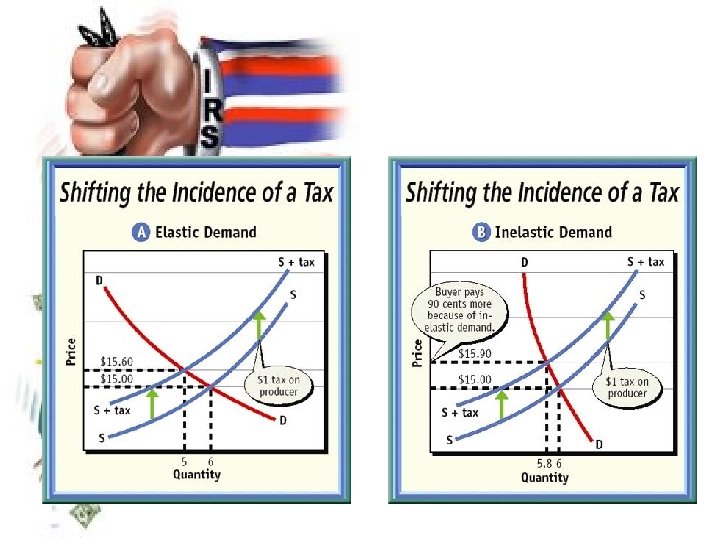

Economic Impact of Taxes: The Incidence of a Tax • “Final Burden of the Tax” • I. e. Utility company: – Raise rates: consumer bears the burden • (easy if demand is inelastic) – Rates are regulated = • Shareholders receive smaller dividends; postpone raises • (more elastic = producer will absorb the tax)

Criteria for Effective Taxes • TAXES are effective when they are: – Equitable – Simple – Efficient

Criteria for Effective Taxes • Criterion 1: Equity or fairness – Taxes should be IMPARTIAL and JUST – Fairness is subjective – Taxes are considered FAIRER – Fewer loopholes: exceptions, deductions, and exemptions

Criteria for Effective Taxes • Criterion 2: Simplicity – Tax LAWS should be EASY to understand – Individual income taxes: the taxes on peoples earnings • Complex tax = dislike – Sales tax: general tax levied on most consumer purchases; • paid at the time of purchase • Anyone purchases = pay tax

Criteria for Effective Taxes • Criterion 3: Efficiency – Easy to administer and successful at generating revenue – Individual income tax – Less efficient: toll booths – Luxury taxes

Two Principles of Taxation • Benefit Principle: those who benefit from government and services should pay in proportion to the amount of benefits received – Gas tax (built in) pay more if you drive more • Two limitations: – Many gov’t services provide the greatest benefits to those who can least afford to pay for them – Benefits are hard to measure

Two Principles of Taxation • Ability-to-Pay Principle: people should be taxed according to their ability to pay, regardless of the benefits they receive. • Two factors – Recognizes that societies cannot always measure benefits – Assumes that people with higher incomes suffer less discomfort paying taxes than people with lower income

Types of Taxes • Proportional: imposes same percentage rate of taxation on everyone • Progressive: imposes a higher percentage rate of taxation on people with high incomes than on those with low incomes • Regressive: imposes a higher percentage rate of taxation on low incomes than on high incomes

Figure 9. 3

The Federal Tax System

IRS (Internal Revenue Service) part of the Treasury Department

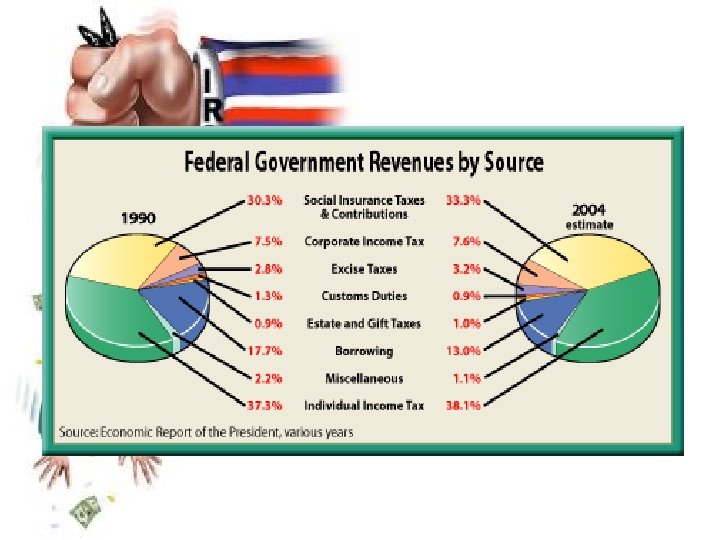

Individual Income Taxes • Fed. Gov’t collects 45% of its revenue from Individual income taxes • Paid over time through payroll withholding system • Before April 15 th each year, an employee must file a tax return: an annual report to the IRS summarizing total income, deductions, & taxes withheld by employers

Individual Income Taxes • Progressive tax – Individuals earning higher incomes pay higher tax rates • Progressive Tax that ranges from 15% -39. 6%

FICA: What is FICA? And why does it take part of my paycheck • FICA stands for Federal Insurance Contributions Act • FICA tax includes Social Security (6. 2% of wages) & Medicare (1. 45% of wages) • 2 nd largest source of Gov’t revenue

FICA • Social Security is a proportional tax up to $65, 400 (the capping point) and then it is regressive • Medicare is not capped; it’s proportional at all levels of income • Total FICA tax = 7. 65%

Corporate Income Taxes • 3 rd largest category of federal taxes • Corporation is recognized as a separate entity • Rates vary from 15% 35% (slightly progressive)

Other Federal Taxes • Excise Tax: tax on the manufacture or sale of certain items, such as gasoline and liquor • Estate Tax: tax the gov’t levies on the transfer of property when a person dies • Gift Tax: tax on gift of money/wealth paid by person making gift

State and Local Tax Systems

State Government Revenue Sources • Intergovernmental Revenues - money from federal gov’t • Sales tax - general tax on consumer purchases • Employee Retirement Contributions • Individual Income Taxes (not all states)

STATE SALES TAX States with the Highest Sales Tax: • Mississippi • Rhode Island • Washington • Texas • Illinois

STATE SALES TAX • States Without a State Sales Tax: • Alaska • Delaware • Montana • New Hampshire • Oregon

Advantages of Sales Tax • Effective way to raise large sums of money • Difficult to avoid because it affects large numbers of consumers • Relatively easy to administer - merchant collects at point of sale

Local Property Taxes • Second largest source of revenue for local governments • Real Property: includes real estate, buildings, & anything permanently attached

Local Property Taxes • Tangible Personal Property: includes tangible items, not permanently attached. • Intangible Personal Property: property with invisible value, such as stock, bond, patent, check

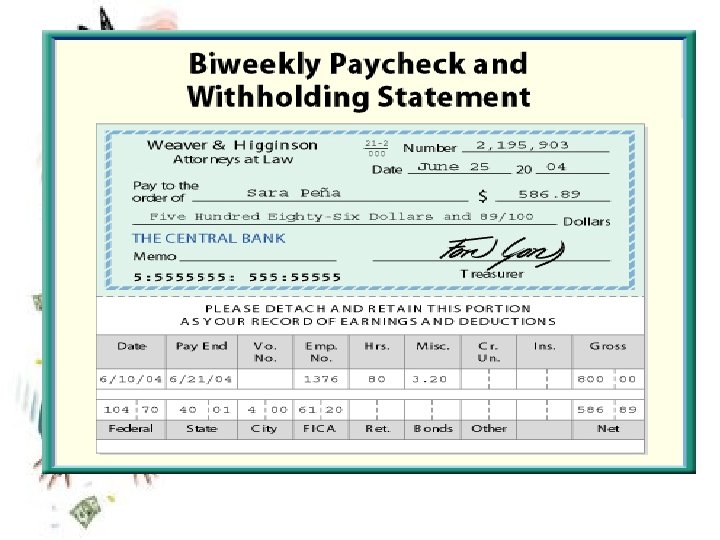

Examining Your Paycheck • Payroll withholding statement: the summary statement attached to a paycheck that summaries income, tax withholdings, and other deductions

QUESTION: WHY ARE STATE & LOCAL GOVERNMENTS LOSING MONEY TO THE INTERNET? ? ? • State & local governments rely heavily on sales tax for revenues • State & local governments already lose $3. 3 billion each year to untaxed interstate sales • This figure will increase as more sales are made over the Internet • Should there be an Internet sales tax? ? ? How would it work?