SEMINAR MANAJEMEN STRATEGIK Steph Subanidja 11 April 2015

SEMINAR MANAJEMEN STRATEGIK Steph Subanidja 11 April 2015

: Comprehensive master plan that stating how the")

DEFINISI STRATEGI v. Hunger & Wheelen (1996): Comprehensive master plan that stating how the corporation will achieves it mission and objectives. It maximizes competitive advantage and minimize competitive disadvantage. v. Gareth R. Jones (1998): The specific pattern of decisions and actions that managers take to use core competences and resources to generate competitive advantages, in order to achieve the organizational goals and outperform competitors. v. Hunger and Wheelen (2001) Strategy is set of managerial decisions and actions that determines long-run performance.

Towards Definition of Strategy “The process of identifying, choosing and implementing activities that will enhance the long term performance of an organization by setting direction and by creating ongoing compatibility between internal skills and resources of the organization, and the changing external environment within which it operates” (Viljoen and Dann, 2003) in The Nature and Scope of Strategic Management.

Wells (1998) in Choosing the Future: “Strategy is like search")

Definition of Strategy (Continued) Wells (1998) in Choosing the Future: “Strategy is like search of the holy grail; it is like the continual asking of the question, what is the meaning of life? ”

WHAT IS STRATEGY LOOK LIKE? Strategy is set of managerial decisions and actions that determines the long-run performance of a firm.

DEFINISI MANAJEMEN STRATEGI ØAn art and a science of formulating, implementing, and evaluating cross-functional decisions that enable an organization to achieve its future objectives. (Fred R. David). ØProses yang digunakan para manajer untuk memilih dan mengimplementasikan atau menyesuaikan serangkaian strategi bagi suatu organisasi guna mewujudkan misi dan visinya. (Hunger & Wheelen)

DEFINISI MANAJEMEN STRATEGI ØProses menganalisis kondisi lingkungan, baik sekarang maupun masa datang, menetapkan tujuan organisasi, merumuskan dan menerapkan strategi, serta mengendalikan keputusan-keputusan yang difokuskan untuk mencapai tujuan organisasi tersebut, baik pada kondisi lingkungan yang sekarang maupun yang akan datang. (Smith, Arnold & Bizzell, 1988) ØProses yang digunakan para manajer untuk menetapkan arah jangka panjang suatu organisasi, menetapkan tujuan kinerja, mengembangkan strategi, guna mencapai tujuan-tujuan dimaksud, berdasarkan kondisi lingkungan internal dan eksternal yang relevan, serta melaksanakan rencana tindakan yang telah dipilih. (Thompson & Strickland, 1987)

DEFINISI MANAJEMEN STRATEGI Strategic Management is defined as the set of decisions and actions that result in the formulation and implementation of plans designed to achieve a company’s objectives. • Strategic Management is a process that involves planning, directing, organizing, and controlling of a company’s strategy-related decisions and actions. (Pearce & Robinson)

Simple Process Of Strategic Management Where is the organization now? ¯Where are we now? How is our company position? ¯If no changes are made, where will we be in the future? Where do we want to go? What kind of business we want to be in and which market position we want to stakeout? Which buyer needs and groups we want to serve? What is outcomes we want to achieve? How will we get there? What specific actions should management undertake? What are the risks and payoffs involved?

Strategic Management: What it is • Strategic is a process (“on going and interrelated activities. . , is a living, evolving process that does not finish once the strategy is written”) • Requires different time lines (time horizons which is affected by market factors, human factors, performance factors). • Concerns organizational context at all levels (corporate level, competitive or business level and operational or functional level). • Is interface between organization and its environment. • Is the management of organizational scope. Source: Viljoen and Dann S 2003, “The Nature and Scope of Strategic Management” in Strategic Management Chapter 1.

The Strategy is actually about: • Developing competitive positioning, plan, pattern, ploy • It is about focusing your business resources and activities. • It is about leveraging, balancing and amalgamating the approach, process and resources. • It is about linking the key function and process. • It is about aligning the formulation and implementation. • It is about understanding the risk • It is about managing the paradox • It has to be systemic • It entails both analytical and intuitive approach.

Where (the organization intent")

Strategy basically tells about: Why (the organization needs to exist) Where (the organization intent to go) What (to achieve or attain) Who (are going to be considered and going to implement) • How (to get it done) • When (it is to be accomplished) • •

What does Strategic Management do? • Strategic Management improve organizational effectiveness. • Creates organizational flexibility. • Utilizes the core competencies of an organization. • Determine the organizational risk profile • Creates the sustainable competencies Source: Viljoen and Dann S 2003, “The Nature and Scope of Strategic Management” in Strategic Management Chapter 1.

What it requires? • • It needs innovation It needs broad knowledge Requires senior managers’ involvement Requires strong leadership Source: Viljoen and Dann S 2003, “The Nature and Scope of Strategic Management” in Strategic Management Chapter 1.

Strategic Management is complex because: • Multidimensional • Based on partial ignorance (manager can never be sure of the nature and significance of their organizations’ environment and future trends) • High risk (as it requires substantial amount of resources over long period of time). • Contextual (internally and externally) • Requires innovation Source: Viljoen and Dann S 2003, “The Nature and Scope of Strategic Management” in Strategic Management Chapter 1.

What is the nature of strategic decisions? • Concerned with organizations activities and boundaries • Relates to the matching of organization’s activities with opportunity of its substantive environment • Require matching of org. activities with its resources • Have major implications to organizations • Influenced by values and expectations • Affects organizations long term directions • Complex in nature • Least systematic in nature (Wilson 2000)

Manajemen Strategis v Perencanaan Strategis Manajemen Strategis dijumpai di dunia akademis Perencanaan Strategis merujuk di daam dunia bisnis Merujuk pada perumusan, Merujuk lebih pada perumusan implementasi dan evaluasi strategi Tujuannya untuk mengeksploitasi Tujuannya untuk mngoptimalkan dan menciptakan berbagai peluang tren dewasa ini untuk masa mendatang Steph Subanidja 17

Tahapan Manajemen Strategis Environmental Scanning Strategy Formulation Strategy Implementation Evaluation and Control

Strategic Management Model, Fred David, 2009 Environmental Scanning External Societal Environment General Forces Task Environment Industry Analysis Internal Structure Chain of Command Culture Beliefs, Expectations, Values Strategy Formulation Strategy Implementation Evaluation and Control Mission Reason for existence Objectives What results to accomplish by when Strategies Plan to achieve the mission & objectives Policies Broad guidelines for decision making Programs Activities needed to accomplish a plan Resources Assets, Skills Competencies, Knowledge Budgets Cost of the programs Procedures Sequence of steps needed to do the job Feedback/Learning Process to monitor performance and take corrective action Performance

Tingkatan Strategi • Strategi tingkat korporasi: berupaya untuk menentukan bisnis apa yang seharusnya dilakukan oleh perusahaan • Strategi tingkat bisnis: berupaya untuk menentukan bagaimana seharusnya suatu perusahaan bersaing dalam setiap bisnisnya • Unit bisnis strategi: bisnis tunggal atau kumpulan bisnis yang berdiri sendiri dan merumuskan strateginya sendiri • Strategi tingkat fungsional: berupaya menentukan cara mendukung strategi tingkat bisnis Steph Subanidja 20

Proses Manajemen Strategis Mengidentifikasi Misi, Tujuan, Sasaran Formulasi Strategi Menganalisis Lingkungan Mengidentifikasi peluang & ancaman Menganalisis Sumberdaya Perusahaan Mengidendifikasi kekuatan & kelemahan Steph Subanidja Implementasi Strategi Evaluasi Strategi 21

Strategic Management Model, Fred David, 2009 Environmental Scanning External Societal Environment General Forces Task Environment Industry Analysis Internal Structure Chain of Command Culture Beliefs, Expectations, Values Strategy Formulation Strategy Implementation Evaluation and Control Mission Reason for existence Objectives What results to accomplish by when Strategies Plan to achieve the mission & objectives Policies Broad guidelines for decision making Programs Activities needed to accomplish a plan Resources Assets, Skills Competencies, Knowledge Budgets Cost of the programs Procedures Sequence of steps needed to do the job Feedback/Learning Process to monitor performance and take corrective action Performance

A LEADER Seseorang tidak akan bisa memimpin individu tanpa bisa membangun kejelasan masa depan bagi mereka. Sebab pemimpin adalah penjelas masa depan” (Napoleon)

Jika kita tahu dimana kita berada dan bagaimana kita akan mencapai tujuan kita, kita mungkin dapat melihat arah kita berjalan- dan jika hasil yang terlihat tidak sesuai, maka buatlah perubahan segera ( Abraham Lincoln)

Jika seseorang tidak memikirkan apa yang jauh di depan, ia akan menemukan kesedihan di dekatnya. Ia yang tidak kawatir tentang apa yang akan terjadi di masa depan, segera akan meemukan sesuatu yang lebih buruk daripada kekawatiran itu sendiri

MINDSET OUT OF THE BOX

garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas")

Buatlah 5 (lima) garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas

garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas")

Buatlah 4 (empat) garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas

garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas")

Buatlah 3 (tiga) garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas

garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas")

Buatlah 2 (dua) garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas

garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas")

Buatlah 5 (lima) garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas

garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas")

Buatlah 1(satu) garis lurus tanpa putus yang menutup 9 (sembilan) titik di atas

OTAK KIRI OTAK KANAN MANA YANG DOMINAN

Dominan Otak Kiri Dominan Otak Kanan Menggunakan logika Menggunakan perasaan Berorientasi detail Berorientasi secara keseluruhan Melihat fakta Melihat imajinasi Kata-kata dan bahasa Simbol dan gambaran Hari ini dan masa lalu Hari ini dan masa depan Matematika dan ilmu pengetahuan Filosofi dan religi Mengetahui Memahami Mengetahui Mempercayai Mengakui Mengapresiasi Mempersepsi urutan/pola Mempersepsi secara spasial/ruang Mengetahui nama objek Mengetahui kegunaan objek Berdasar pada realita Berdasar pada fantasi Menyusun strategi Berdasar pada apa yang terjadi Praktis Terburu-buru/tidak sabar Bermain aman Mengambil resiko

Stage 1: The Input Stage External")

Strategy-Formulation Analytical Framework Internal Factor Evaluation Matrix (IFE) Stage 1: The Input Stage External Factor Evaluation Matrix (EFE) Competitive Profile Matrix (CPM)

Weight Internal Factors Strengths 1 Weighted Score Rating 2")

Internal Factor Analysis Summary (IFAS) Weight Internal Factors Strengths 1 Weighted Score Rating 2 3 Comments 4 5 Weaknesses Total Weighted Score 1. 00 Notes: 1. List opportunities and threats (5– 10 each) in column 1. 2. Weight each factor from 1. 0 (Most Important) to 0. 0 (Not Important) in Column 2 based on that factor’s probable impact on the company’s strategic position. The total weights must sum to 1. 00. 3. Rate each factor from 5 (Outstanding) to 1 (Poor) in Column 3 based on the company’s response to that factor. 4. Multiply each factor’s weight times its rating to obtain each factor’s weighted score in Column 4. 5. Use Column 5 (comments) for rationale used for each factor. 6. Add the weighted scores to obtain the total weighted score for the company in Column 4. This tells how well the company is responding to the strategic factors in its external environment. Source: T. L. Wheelen and J. D. Hunger, “External Strategic Factors Analysis Summary (EFAS). ” Copyright © 1991 by Wheelen and Hunger Associates. Reprinted by permission.

: Maytag as Example Weight Internal Factors Strengths 1 Weighted")

Internal Factor Analysis Summary (IFAS): Maytag as Example Weight Internal Factors Strengths 1 Weighted Score Rating 2 3 Comments 4 5 . 15. 05. 10. 05. 15 5 4 4 3 3 . 75. 20. 40. 15. 45 Quality key to success Know appliances Dedicated factories Good, but deteriorating Hoover name in cleaners • Process-oriented R&D • Distribution channels . 05 2 2 . 10 • Financial position • Global positioning . 15. 20 2 2 . 30. 40 • Manufacturing facilities . 05 4 . 20 Slow on new products Superstores replacing small dealers High debt load Hoover weak outside the United Kingdom and Australia Investing now • • • Quality Maytag culture Experienced top management Vertical integration Employee relations Hoover’s international orientation Weaknesses Total Weighted Score 1. 00 3. 05

Critical External Factors Weight Rating Weighted")

EFE Matrix atau EFAS (External Factor Analysis Summary) Critical External Factors Weight Rating Weighted Score Opportunities a. b. c. d. Threats a. b. c. Total 9/26/2020 1, 00 Copyright I. Hardhy Winarta, 2006 ? 40

Copyright 2007 Prentice Hall Ch 3 -41

Strategic Factor Analysis Summary SFAS Strategic Factors Weight Rating Weighted score ST IT LT Comments S 1 Quality Maytag culture 0. 10 5. 0 0. 50 X Quality key to success S 5 Hover international orientation 0. 10 2. 8 0. 28 X X Name recognition W 3 Financial position 0. 10 2. 0 0. 20 X X High debt W 4 Global positioning 0. 15 2. 2 0. 33 O 1 Eco. Integration of EU 0. 10 4. 1 0. 41 O 2 Demographic favor quality 0. 10 5. 0 0. 50 O 5 Trend to super stores 0. 10 1. 8 0. 18 X Weak in this channel T 3 Whirlpool and Electrolux 0. 15 3. 0 0. 45 X Dominate industry T 5 Japanese Appliance companies 0. 10 1. 6 0. 16 Total Scores 1. 00 Only in UK and AUS X X Acquisition of hover Maytag quality X Asian presence

Gateway Critical Success Factors Apple Dell Weight Rating")

Industry Analysis: Competitive Profile Matrix (CPM) Gateway Critical Success Factors Apple Dell Weight Rating Wt’d Score Market share 0. 15 3 0. 45 2 0. 30 4 0. 60 Inventory sys 0. 08 2 0. 16 4 0. 32 Fin position 0. 10 2 0. 20 3 0. 30 Prod. Quality 0. 08 3 0. 24 4 0. 32 3 0. 24 Cons. Loyalty 0. 02 3 0. 06 4 0. 08 Sales Distr 0. 10 3 0. 30 2 0. 20 3 0. 30 Global Exp. 0. 15 3 0. 45 2 0. 30 4 0. 60 Org. Structure Prod. Capacity 0. 05 0. 04 3 3 0. 15 0. 12 E-commerce 0. 10 3 0. 30 Customer Serv 0. 10 3 0. 30 2 0. 20 4 0. 40 Price competitive 0. 02 4 0. 08 1 0. 02 3 0. 06 Mgt. experience 0. 01 2 0. 02 4 0. 04 2 0. 02 Total 1. 00 Copyright 2007 Prentice Hall 2. 83 2. 47 3. 49 Ch 3 -43

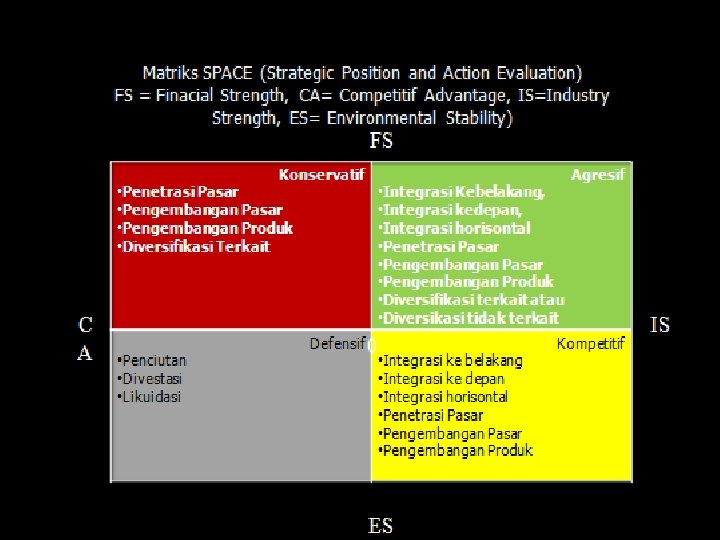

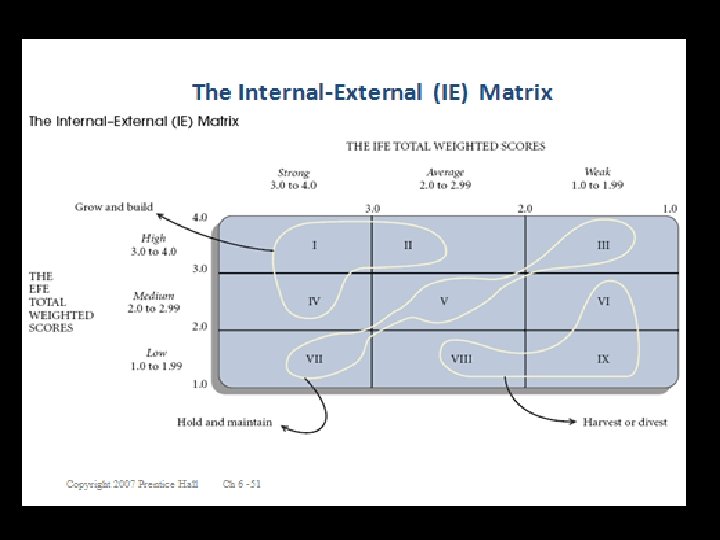

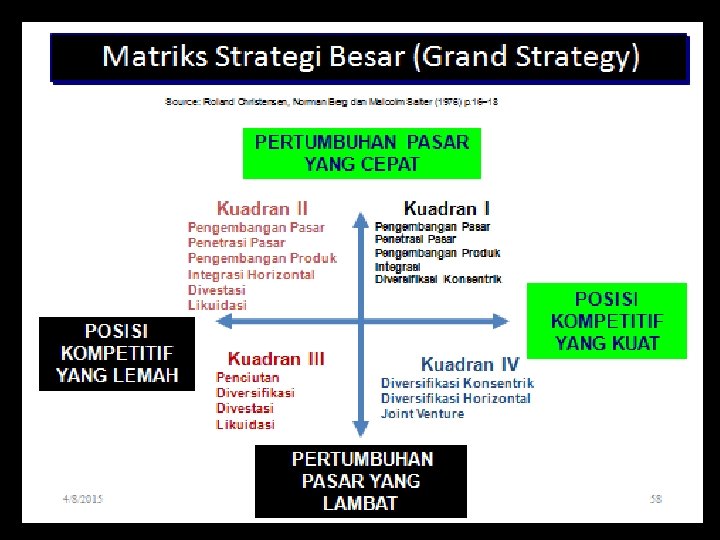

Strategy-Formulation Analytical Framework SWOT Matrix SPACE Matrix Stage 2: The Matching Stage BCG Matrix IE Matrix Grand Strategy Matrix Copyright 2007 Prentice Hall

Maytag strengths S 1 – S 5")

TOWS Matrix for Maytag Example Strength (S) Maytag strengths S 1 – S 5 Weakness (W) Maytag weaknesses W 1 – W 5 Opportunities (O) May Tag Opportunities O 1 – O 5 SO Strategies -Use worldwide Hoover distribution channels for both Hoover and Maytag major appliances -Find joint venture partners in Eastern Europe and Asia WO Strategies: - Expand Hoover presence in continental Europe by improving Hoover quality and reducing manufacturing and distribution costs. - Emphasize superstore channel for all non-Maytag brand Threats (T) May Tag Opportunities T 1 – T 5 ST Strategies: - Acquire Raytheon appliance business to increase US market share. -Merge with Japanese major home appliance company. -Sell of all non-Maytag brand WT strategies: -Sell of Dixie-Narco division to reduce debt -Emphasize cost reduction to reduce break-even point -Sell out to Raytheon or a Japanese firm

The use of SWOT analysis for Strategic Recommendation SWOT Strength Weakness Opportunity SO Strategy: use the strength to tap the opportunity. Example: Microsoft, Danone, Indofood Sukses Makmur WO strategy: overcome weakness by tapping the opportunity. Example: Modify poor technology infrastructure to enter new market Threats ST Strategy: Use strength to avoid threats Example: mergers and acquisition (look at Daimler etc), use rigorous marketing effort WT Strategy: Minimize weakness and avoid threats By divesting the resources, or liquidation

Steph Subanidja 49

Backward Integration Forward Integration Horizontal Integration Market Penetration Intensive Market Development Product Development GRAND STRATEGIES Diversification Concentric Diversification Horizontal Diversification Conglomerate Diversification Joint Venture Retrenchment Defensive 9/26/2020 Strategic Management Divestiture Combination Liquidation 52

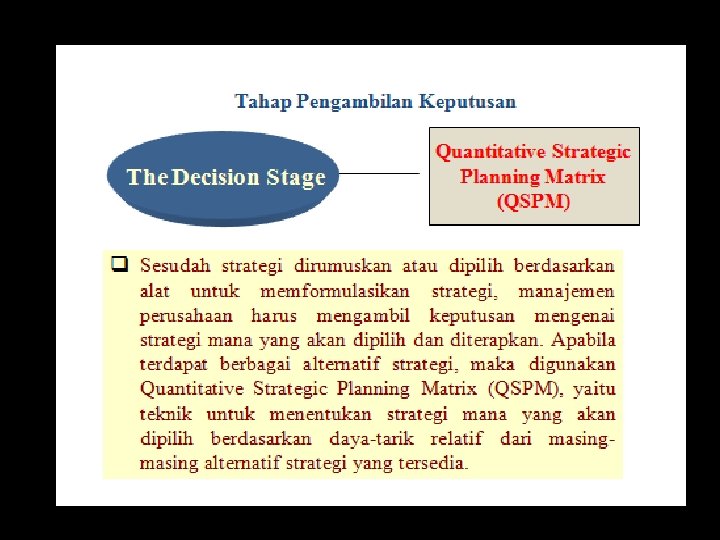

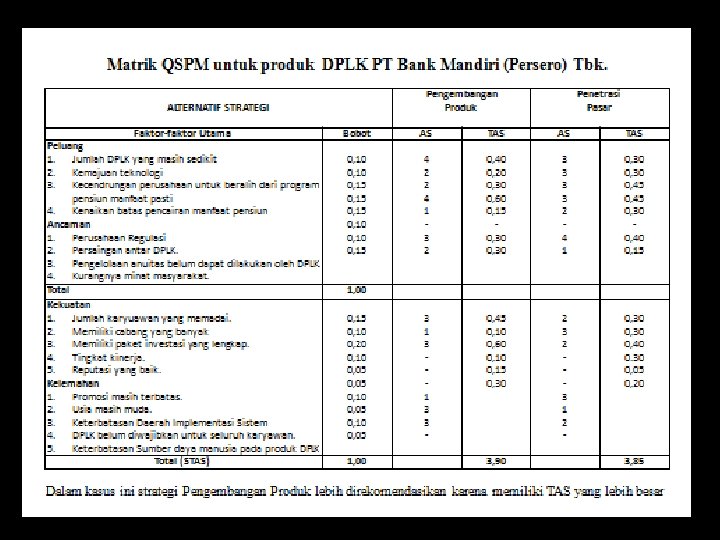

q")

Strategy-Formulation Analytical Framework Stage 3: The Decision Stage Quantitative Strategic Planning Matrix (QSPM) q Technique designed to determine the relative attractiveness of feasible alternative actions

–Tipe 1 o Biaya rendah")

Tiga Strategi Generik Porter 1. Keunggulan/kepeimpinan biaya (cost leadership) –Tipe 1 o Biaya rendah (low cost) – Tipe 2 o Nilai terbaik (best value)-Tipe 3 2. Pembedaan/diferensiasi-Tipe 4 3. Fokus-Tipe 5

Strategi Generik • Strategi kepemimpinan biaya: strategi yang diikuti oleh organisasi ketika organisasi ingin menjadi produsen dengan biaya terendah di dalam industri • Strategi diferensiasi: strategi yang diikuti perusahaan ketika perusahaan ingin menjadi unik di dalam industri sehingga dihargai secara luas oleh konsumennya • Strategi fokus: strategi yang diikuti perusahaan ketika perusahaan mengejar keunggulan biaya atau diferensiasi dalam segmen industri yang fokus • Jika tidak mampu menjalankan satu diantara tiga ini disebut stuck in the middle, sulit mencapi sukses di masa mendatang Steph Subanidja 58

Market Size-Strategi Generik Kepemimpinan Biaya Ukuran Pasar Besar Kecil Tipe 1 Tipe 2 - Diferensiasi Fokus Tipe 3 - Tipe 3 Tipe 4 Tipe 5

Balanced Score Card A new approach to strategic management was developed in the early 1990's by Drs. Robert Kaplan (Harvard Business School) and David Norton (Balanced Scorecard Collaborative). They named this system the 'balanced scorecard'. Recognizing some of the weaknesses and vagueness of previous management approaches, the balanced scorecard approach provides a clear prescription as to what companies should measure in order to 'balance' the financial perspective. 9/26/2020 60

Balanced Score Card • Kaplan and Norton describe the innovation of the balanced scorecard as follows: “The balanced scorecard retains traditional financial measures. But financial measures tell the story of past events, an adequate story for industrial age companies for which investments in long-term capabilities and customer relation-ships were not critical for success. These financial measures are inadequate, however, for guiding and evaluating the journey that information age companies must make to create future value through investment in customers, suppliers, employees, processes, technology, and innovation. " 9/26/2020 61

Diffusion of a New Idea • “The Balanced Scorecard: Measures that Drive Performance” (Robert S. Kaplan and David P. Norton, Harvard Business Review, February 1992) • About 35% of Fortune 2000 firms have adopted a balanced scorecard, 55% of those firms are very satisfied with it. (R. D. Banker, C. Konstans and S. Janakiraman; January 2000) 9/26/2020 62

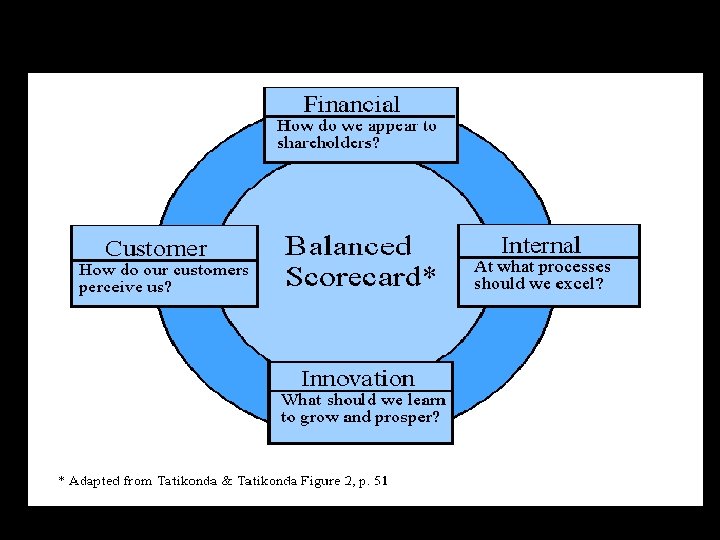

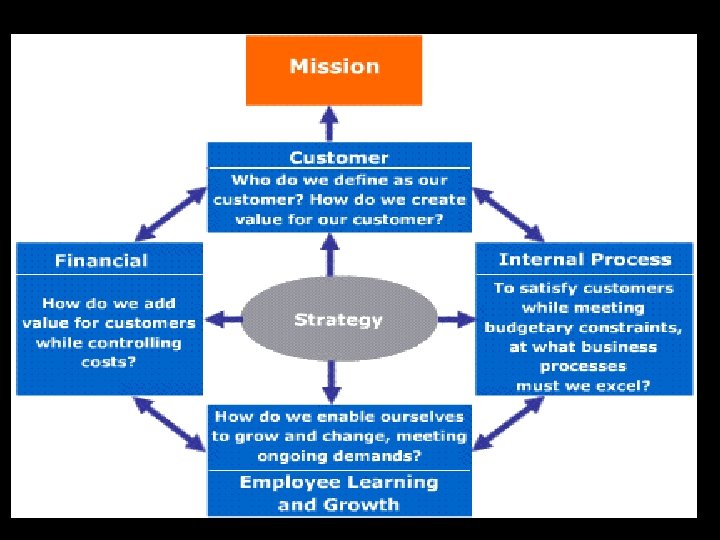

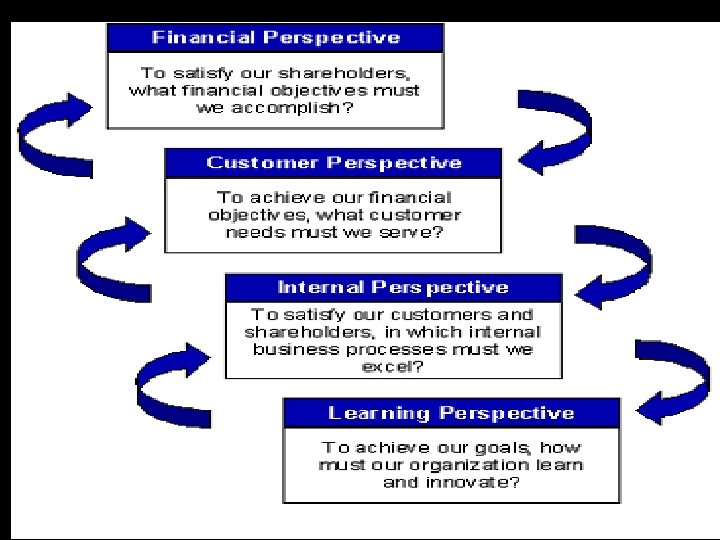

Balanced Scorecard FINANCIAL To succeed financially, how should we appear to our shareholders? CUSTOMER To succeed financially, how should we appear to our shareholders? Vision and Strategy INTERNAL BUSINESS PROCESS To satisfy our shareholders and customers, what businesses must we excel at? LEARNING AND GROWTH To succeed financially, how should we appear to our shareholders? Source: Kaplan, Robert S. and David P. Norton. 1996. Using the Balanced Scorecard as a Strategic Management System. Harvard Business Review 74 (January-February): 76.

Balanced Scorecard Financial Perspective How do we look to our shareholders? Internal Process Perspective Customer Perspective How do we look to our customers? Vision & Strategy What business processes are the value drivers? Learning & Growth Perspective Are we able to sustain innovation, change & improvement 9/26/2020 64

Balanced Scorecard Financial Perspective Liquidity, Leverage, Activity Ratio, Profitability Ratio EVA , MVA Customer Perspective • Customer satisfaction • Customer retention • Market share Vision & Strategy Internal Process Perspective • Service quality • Product quality • Inventory management Learning & Growth Perspective • Information systems • Employee Satisfaction • Employee training 9/26/2020 I. Hardhy Winarta, 2010 65

Balance in the Scorecard • Balance between financial, customer, internal process and learning perspectives • Balance between financial and nonfinancial measures • Balance between short-term and long-term objectives Balance between hard, objective measures and softer, more subjective measures Balance between different stakeholders Balance between strategic and diagnostic measures 9/26/2020 I. Hardhy Winarta, 2010 66

Horizontal Balanced Scorecard Investors Lenders Customers Employees Suppliers Financial Perspective Customer Perspective Internal Perspective Process Perspective Balance between different stakeholders. 9/26/2020 I. Hardhy Winarta, 2010 67

Vertical Balanced Scorecard Financial Objectives Customer Objectives Internal Process Objectives Learning and Growth Objectives 9/26/2020 68

Balanced Score Card 9/26/2020 I. Hardhy Winarta, 2010 69

A Balanced Scorecard q “Is a performance measurement system that translates an organization’s strategy into clear objectives, measures, targets, and initiatives. ” (Kaplan and Norton, Harvard Business Review, 1996). q ”A method for the organization to systematically develop a comprehensive link between its strategy and a coherent set of performance measures. ” q “A method for the organization to systematically develop a comprehensive system of planning and (Kaplan and Norton, Harvard Business Review, 1992) 9/26/2020 I. Hardhy Winarta, 2010 control”. 70

provides a framework for selecting multiple")

Balanced Score Card § The balanced scorecard (BSC) provides a framework for selecting multiple performance measures focused on critical aspects of business (Kaplan and Norton 1992). § The essence of the BSC is the articulation of linkages between performance measures and strategic objectives (Kaplan and Norton 1996). 9/26/2020 I. Hardhy Winarta, 2010 71

Translating Strategy Into Initiatives For each perspective: Strategy Key Success Factors Performance Measures Targets 9/26/2020 I. Hardhy Winarta, 2010 Initiatives 72

Balanced Scorecard • Empat Perspektif: 1. Keuangan 2. Konsumen 3. Proses bisnis 4. Pembelajaran dan pertumbuhan

Evaluation Framework I. Review Underlying Bases Differences? Yes NO III. Take Corrective Actions II. Measure Firm Performance Differences? NO Continue present course Yes

Skema Evaluasi Strategis 1. Buat Revisi Matriks IFAS 2. Bandingkan Matriks IFAS Revisi dan Sebelumnya Ada perbedaan signifikan? 1. Buat Revisi Matriks EFAS 2. Bandingkan Matriks EFAS Revisi dan Sebelumnya Ya Tidak Mengukur Kinerja Organisasi Bandingkan Pencapaian Tujuan yang Direncanakan dengan Kenyataan Ada perbedaan signifikan? Tidak Teruskan Arah Saat Ini Ya Ambil Tindakan Korektif

- Slides: 79