SEGMENT REPORTING AND IND AS 108 GOLDI KUMARI

of Segmentation: A diversified company may")

• INTRODUCTION • BRIEF • OBJECTIVES • NEEDS • BENEFITS")

Revenue •")

")

Ø Meaning Ø Scope (Segment Reporting) Ø Objectives(Segment Reporting) Ø Ind")

108 (OPERATING SEGMENT) An entity shall disclose information to")

IAS 14 Segment Reporting requires reporting of financial")

- Slides: 47

SEGMENT REPORTING AND IND AS 108 GOLDI KUMARI YADAV, DIWAS JASLEEN KAUR , HARSHVEER, ANJALI, MANIKA JAIN

SEGMENT REPORTING • The concept of segment reporting is applicable to a diversified enterprise. A diversified company may be defined as a company which has diversified operations, i. e. , activity or operations in different industries and/or foreign operations and sales where those activities (or operations) are significant in terms of sales revenue, profit or losses generated or assets employed. • It is also true that segmentation along industry and geographical lines subject to different profitability, different risks and different growth prospects are likely to be found in most diversified companies. The diversified companies and their operations indifferent industries, activities and geograph ical areas raise questions as to whether modifications are necessary to the existing framework of corporate accountability and financial reporting practices.

NEED FOR SEGMENT REPORTING Diversified companies present a peculiar and special problem for investment decision-making. The progress and success of a diversified company are composites of the progress and success of its several segments. 1. Segment Disclosure and Investment Decision-Making: They will be able to predict more accurately a firm’s future earnings and cash flows than can be done by using consolidated data alone. Investor uncertainty about company prospects will thus be reduced, share prices will be set more accurately, and a more efficient allocation of resources will be promoted. 2. Segments Disclosure and Other Users (Other than Investors): Besides the investors, it has been suggested that segmental reports are likely to be useful to employees and trade unions, consumers, the general public, government and also for the purpose of promoting managerial efficiency. Employees and trade unions are interested in the performance and prospects of the firm from the standpoint of wage negotiations and job security and hence, segmental reports may be just as relevant to them as to investors.

DIFFICULTIES IN SEGMENT REPORTING 1. Base (or Bases) of Segmentation: A diversified company may be divided for segment reporting purposes in terms of organization division, industry, market, customer product, etc. Each base of segmentation may create segments that differ significantly in profitability, growth and risk and each implies a different basis for identifying segments. Unless the base (or bases) selected actually represent the company and the way it operates, unless they reflect the difference within the company regarding rate of profit, degree of risk, and potential for growth, reports of operating data by segments are unlikely to be of any real use. 2. Allocation of Common Costs: In a business enterprise producing more than one product or engaged in different activities, there are likely to be costs which are common to two or more of the products. Examples of common costs are general administrative and selling expenses, legal expenses, general advertising etc. Because these costs are common to more than one segment, they cannot be associated in entirety with a single segment.

3. Pricing Inter-segment Transactions: There are different methods for inter segment transfers such as cost, cost plus, market price, and negotiated price. The basic purpose (in selecting a method of transfer pricing) is to motivate employees, and to actually measure the success of the several segments as accurately as possible. Different methods results in different operating results for the segments. For a meaningful segment reporting, there is a need for selecting a reasoned method for inter segment transfers. 4. Costs of Segment Disclosure: Another important cost argument relates to the increased competition that may result from segmental disclosures. It is argued that the disclosure of profitable segments will attract competitors, whilst loss making segments may become the subject of take over bids or put pressure on management to sell them off, with the purpose of improving profits in the short term and to take on less risky projects. A competitive disadvantage may also occur where foreign companies are not required to provide segmental reports.

5. Management Conservatism: Another argument is that, where there is no regulatory provision to disclose segmental reports, voluntary disclosures are likely to be perceived by managements to be beneficial only in certain instances; for example, where management believes that the company’s attractiveness to investors will be enhanced and the costs of finance reduced. Few companies are likely to take voluntary action that may benefit their competitors or reveal weaknesses.

CONTENTS (AS-17) • INTRODUCTION • BRIEF • OBJECTIVES • NEEDS • BENEFITS

INTRODUCTION In today's competitive market a businessman does not deal in any particular product or market but it want to serve in multiple products/services and operates in different geographical areas. So it can cover wide area and face cut through competition when a business firm function in multiple products/services and in different market it need to properly anticipate and analyze risks and opportunities. All these information must be recorded in proper reports which is known as SEGMENT REPORTING.

ACCOUNTING STANDARD -17 • AS 17 , segment reporting issued by the council of the institute of chartered accountants of India. Segment report may be defined as financial report of diversified enterprise engaged in diversified operation i. e. activity or operations in different industries and with foreign operations. It is applicable to level 1 Enterprises and not to level 2 and level 3 enterprises in their entirely. LEVEL 1 ENTERPRISE: Enterprises whose turnover exceeds 50 crores , enterprises having borrowings in excess of 10 crores. LEVEL 2 ENTERPRISE: Enterprises whose turnover exceeds 40 lakhs but does not exceed 50 crores and having borrowings in excess of 1 crore but not in excess of 10 crores. LEVEL 3 ENTERPRISE: Enterprises which are not covered under level 1 and level 2.

OBJECTIVES OF SEGMENT REPORTING ☆Identify business opportunities. ☆Provides Financial information to various users of financial statements. ☆Better assess risks and returns.

NEED FOR SEGMENT REPORTING ☆ Segment Disclosure for investment decision making. ☆ Profitability, risk and opportunities. ☆ Segment Disclosure for other users. ☆ Employees, consumers , general public, government.

BENEFIT OF SEGMENT REPORTING ☆Allocation of resources. ☆Investment decisions. ☆Equilibrium in share prices. ☆True and fair view.

LIMITATIONS OF SEGMENT REPORTING ☆Base of segmentation. ☆Allocation problem. ☆inter segment transaction. ☆Difficulty in providing data.

REPORTABLE SEGMENT An entity shall report separately information about each operating segment. It has 3 limits : Limit 1 - Segment revenue is 10% or more of total segment revenue. Limit 2 - Segment result is 10% or more of total segment profit or total segment loss whichever is higher. Limit 3 - Segment asset are 10% or more of total segment assets. If any limit is satisfied, segment becomes reportable.

DISCLOSURE • Primary Reporting Format • Secondary Reporting Format • Other Disclosure

PRIMARY REPORTING FORMAT • Segment Revenue: Classified into external revenue and inter segment revenue. • Segment asset: Total carrying amount of segment assets. • Segment Liabilities: Total amount of segment liabilities. • Addition to fixed assets: Tangilble Or intangilble fixed assets. • Depreciation and non cash expenditure: Total amount of depreciation and non cash expenditure included in the expenses.

SECONDARY REPORTING FORMAT • Secondary Reporting Format consist information about • a) Revenue • b) Assets • c) Capital expenditure

OTHER DISCLOSURE • Under this disclosure such as : • Changes in accounting policies adopted for segment reporting that have a material effect on segment information should be disclosed. • Changes in the method of depreciation should be disclosed.

SEGMENT REPORTING(IND AS-108)

CONTENTS (IND AS-108) Ø Meaning Ø Scope (Segment Reporting) Ø Objectives(Segment Reporting) Ø Ind AS-108 (Operating Segment) Ø Operating Segment (Meaning) Ø Scope ( Operating Segment Ind AS-108 ) Ø Reportable Segment Ø Disclosure

MEANING OF SEGMENT REPORTING. Component of an entity whose activities represent a separate major line of business or class of customer. A segment may be in the form of a subsidiary or division or a department, and in some cases a joint venture.

OBJECTIVES OF SEGMENT REPORTING. The performance of a diversified company can be judged from the performance of all several segments. The success of diversified company depends on success of all segments that is why segmental disclosures in company’s annual reports are more useful to investors and other user groups. Helpful for the users in many ways: (i)Users of financial statements can better understand the performance of an enterprise. (ii) Users can better assess the risks and return of an enterprise. (iii) Users can make more informed judgment about the enterprise as a whole. (iv) Users can benefit from an enhanced degree of comparability with other enterprises.

USERS GROUPS OF SEGMENT REPORTING. 1. Investors: 2. Employees: Segment reporting provides investor’s information about profitability risk and growth of various segments of enterprises operations. Employees and trade unions are also interested in the performance and prospects of the enterprise from the stand point of wage negotiations and job security.

3. Management: Segment reporting is also helpful to the management while taking various important managerial decisions. 4. Government Agencies: 5. Consumers: Government agencies at national and international level in the case of multinational companies, are becoming more concerned by the activities of large companies. The Interests of consumers and the General public may also be promoted by segmental disclosures.

INDIAN ACCOUNTING STANDARD (IND AS) 108 (OPERATING SEGMENT) An entity shall disclose information to enable users of its financial statements to evaluate the nature and financial effects of the business activities in which it engages and the economic environments in which it operates.

MEANING AND BRIEF ABOUT OPERATING SEGMENT. An operating segment is a component of an entity: Whose operating results are analyzed by operation decision maker to make decisions about resource allocation. That engages in business activities from which it may earn revenues and incur expenses. For which discrete financial information is available.

SCOPE OF OPERATING SEGMENT IND AS-108. ~This Accounting Standard shall apply to companies to which Indian Accounting Standards (Ind AS) notified under the Companies Act apply. ~ If an entity that is not required to apply this Indian Accounting Standard chooses to disclose information about segments that does not comply with this Indian Accounting Standard, it shall not describe the information as segment information. ~ If a financial report contains both the consolidated financial statements of a parent that is within the scope of this Indian Accounting Standard as well as the parent’s separate financial statements, segment information is required only in the consolidated financial statements.

DISCLOSURE An entity shall disclose information to enable users of its financial statements to evaluate the nature and financial effects of the business activities in which it engages and the economic environments in which it operates.

AN ENTITY SHALL DISCLOSE THE FOLLOWING FOR EACH PERIOD FOR WHICH A STATEMENT OF PROFIT AND LOSS IS PRESENTED: • Information about reported segment profit or loss, including specified revenues and expenses included in reported segment profit or loss, segment assets, segment liabilities and the basis of measurement. • Reconciliations of the totals of segment revenues, reported segment profit or loss, segment assets, segment liabilities and other material segment items to corresponding entity amounts.

IND. AS 108 VS AS 17 Ind. As 108 is known as Operating Segments as against As 17 is known as Segmental reporting. The latter deals with two kinds of /types of segments – 1. Business segments and 2. Geographical Segments But, as has been spelt out earlier, in Ind. ASs 108 'Management approach' is the kernel that determines and gives the road map to decide on 'operating segments' known as components of the entity that management monitors in making decisions on operating matters.

IND AS 108 OBJECTIVES – • Disclose information to enable users of its financial statements to analyze the nature and financial effects of the different business activities in which it engages and the economic environments in which it operates. • Where an entity with a matrix organizational structure is unable to clear it identify operating segments, it is required to look to the core principle in determining the appropriate basis of segmentation. SCOPE – IND AS 108 applies to the separate or individual financial statements of an entity : • Whose debt or equity instruments are traded in a public market or • that files, or is in the process of filing, its financial statements with a securities commission or other regulatory organization for the purpose of issuing any class of instruments in a public market.

IND AS 108: TYPES OF SEGMENTS In case of Business Segment: Business segments are components of business, having separate risk and rewards which are engaged in production of goods, rendering services. These are based on: • Products: consumer products, food etc. • Production process: khadi gram Udyog • Types of consumers: industrial, domestic • Distribution process: agency business, owned shops In case of Geographical Segment: Geographical Segment means components of business having separate risk and rewards engaged in doing business in particular economic environment. • Location of assets • Location of customers

STEPS TO IMPLEMENT IND AS 108 • Applicability of segment reporting • Identification of segments • Fulfillment aggregation criteria • Quantitative threshold • Identification of new segment • Development of format for disclosures • Development of reconciliation format

ACCOUNTING STANDARD – AS 17 The objective of this Standard is to establish principles for reporting financial information, about the different types of products and services an enterprise produces and the different geographical areas in which it operates. Such information helps users of financial statements: (a) better understand the performance of the enterprise; (b) better assess the risks and returns of the enterprise; and (c) make more informed judgements about the enterprise as a whole. Many enterprises provide groups of products and services or operate in geographical areas that are subject to differing rates of profitability, opportunities for growth, future prospects, and risks. Information about different types of products and services of an enterprise and its operations in different geographical areas – often called segment information – is relevant to assessing the risks and returns of a diversified or multi locational enterprise but may not be determinable from the aggregated data. Therefore, reporting of segment information is widely regarded as necessary for meeting the needs of users of financial statements.

COMPARISON OF IND 108 WITH AS 17 PARTICULARS IND AS 108 AS 17 IDENTIFICATION OF SEGMENTS Is based on management approach Requires identification of 2 types of segment primary and secondary segments BASIS OF MEASUREMENT FOR AMOUNTS TO BE REPORTED IN SEGMENTS Shall be measured on the same basis as used by the chief operating decision maker for the purposes of allocating resources to segment and assessing its performance Requires segment information to be prepared in conformity with the accounting policies adopted for preparing and presenting financial statements AGGREGATION CRITERIA Specifies aggregation for 2 or more segments that have similar long term financial performance Silent

PARTICULARS IND AS 108 IND AS 17 SINGLE REPORTABLE SEGMENT Requires certain disclosure even in case of entities have single reportable segment Segment information not required INTEREST EXPENSE Requires separate disclosures about interest revenue and expense for each reportable segment Definition of segment expense excluded interest DISCLOSURES Requires disclosures of revenue from external Disclosures are based on customers of each product and service. With classification of segments as regard to geographical information , it requires primary and secondary segments the disclosure of revenues from customers in the country of domicile and in all foreign countries , non current assets in the country of domicile and in all foreign countries

AGGREGATION CRITERIA Two or more Operating Segments may be aggregated into a single operating segment if the segments have similar economic characteristics and segments are similar in each of the following respects: • the nature of the products and services; • the nature of the production processes; • the type or class of customer for their products and services; • the methods used to distribute their products or provide their services; and • if applicable, the nature of the regulatory environment, for e. g. , banking, insurance or public utilities.

INFORMATION TO BE INCLUDED IN SEGMENT REPORTING • The factors used to identify reportable segments • The types of products and services sold by each segment • The basis of organization (such as being organized around a geographic region, product line, and so forth) • Revenues • Interest expense • Depreciation and amortization • Material expense items • Equity method interests in other entities • Income tax expense or income • Other material non cash items • Profit or loss

IFRS 8 - OPERATING SEGMENTS IFRS 8 Operating Segments requires particular classes of entities (essentially those with publicly traded securities) to disclose information about their operating segments, products and services, the geographical areas in which they operate, and their major customers. Information is based on internal management reports, both in the identification of operating segments and measurement of disclosed segment information. DEFINITION IFRS 8 defines an operating segment as follows. An operating segment is a component of an entity: • that engages in business activities from which it may earn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same entity) • whose operating results are reviewed regularly by the entity's chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance and • for which discrete financial information is available

SCOPE OF IFRS 8 • IFRS 8 applies to the separate or individual financial statements of an entity (and to the consolidated financial statements of a group with a parent): • whose debt or equity instruments are traded in a public market or • that files, or is in the process of filing, its (consolidated) financial statements with a securities commission or other regulatory organisation for the purpose of issuing any class of instruments in a public market

IAS 14 - SEGMENT REPORTING (SUPERSEDED) IAS 14 Segment Reporting requires reporting of financial information by business or geographical area. It requires disclosures for 'primary' and 'secondary' segment reporting formats, with the primary format based on whether the entity's risks and returns are affected predominantly by the products and services it produces or by the fact that it operates in different geographical areas. Objective of IAS 14 • The objective of IAS 14 (Revised 1997) is to establish principles for reporting financial information by line of business and by geographical area. It applies to entities whose equity or debt securities are publicly traded and to entities in the process of issuing securities to the public. In addition, any entity voluntarily providing segment information should comply with the requirements of the Standard. • Applicability • IAS 14 must be applied by entities whose debt or equity securities are publicly traded and those in the process of issuing such securities in public securities markets. • If an entity that is not publicly traded chooses to report segment information and claims that its financial statements conform to IFRSs, then it must follow IAS 14 in full. • Segment information need not be presented in the separate financial statements of a (a) parent, (b) subsidiary, (c) equity method associate, • equity method joint venture that are presented in the same report as the consolidated statements.

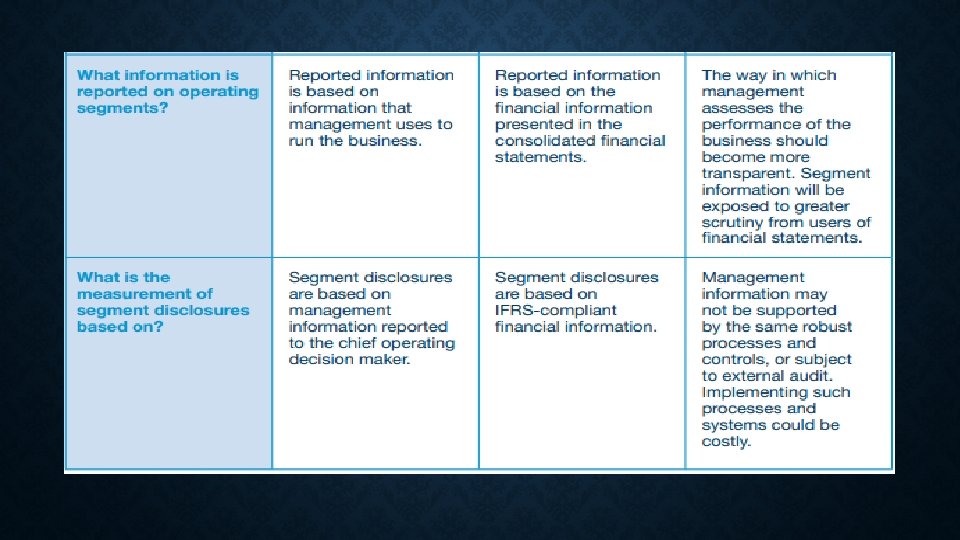

KEY DIFFERENCES BETWEEN IFRS 8 AND IAS 14

REPORTABLE SEGMENTS METHOD 1 : LIMIT METHOD 2 : CHOICE OF MANAGEMENT METHOD 3 : COMPARATIVE METHOD

Case Study Carnegie Case 70 • 2 companies operating in similar regions Ø Malaysia Airlines System Berhad (Malaysia Airlines) Ø Singapore Airlines • Both companies conduct business internationally • Segment reporting details were as follows: Malaysia Singapore Business segment details • airline operations • cargo • airline operations • airport terminal services Geographical segment details • segment revenue only • no segment profit, as it was neither practical nor meaningful to allocate costs on that basis • no segment assets or liabilities as planes are used internationally • segment revenue only • assets (flight and ground equipment) are mainly located in Singapore. Therefore no analysis of assets was provided

QUESTIONS Ques 1: Compare the disclosures of the 2 companies and comment on the comparability. Answer: With respect to segment disclosures, the quality of the two companies’ disclosures is quite similar. In relation to business segments, a reasonable level of disclosure was provided (i. e. segment revenue, results, assets, and liabilities), but under two rather general headings: • airline operations and cargo services’ for Malaysia, and • airline operations and airport terminal services’ for Singapore In relation to geographical segments, a more detailed breakdown of regions was provided, but only minimal disclosure (i. e. details of segment revenue) Ques 2: Evaluate the explanations given by the 2 companies. Answer: The explanation provided gives rise to several issues: • Some companies genuinely believe it is not possible or feasible to segregate parts of the business, based on the nature of the business and the manner in which it operates • Other companies may use this as a convenient excuse to avoid disclosure of such information • Importantly, the approach to disclosure (i. e. minimal v extensive disclosure) taken by one company in a particular industry, may have a strong influence on the approach to disclosure taken by other companies in that industry • For example, some companies in a particular industry may set the benchmark for a high level of transparency and disclosure, which may subsequently influence other companies in that industry to take a similar approach. Other companies (or industries) may establish a benchmark for a low level of

CONCLUSION • Segment reporting requires companies especially those which are multi product and multi location to disclose their segment wise operations in their annual reports as well as in their quarterly reports. • The users of financial statements have different utilities for the financial information. The users of accounting information are the stakeholders and they are mainly concerned with financial information of various segments of business. • The concept of segment reporting in a formalized form is almost 32 years old. It was proposed in 1974 when the Financial Accounting Standard Board (FASB) of USA issued Statement of Financial Accounting Standards (SFAS) 14. After, this International Accounting Standards Committee issued IAS 14 reporting financial information by segment in 1981. • Both SFAS 14 and IAS 14 were revised to make segment reporting more informative. SFAS 14 was revised by the FASB with the issue of SFAS 131 in 1997, whereas IAS 14 was revised in 1998. • Now, several countries through the standards issued by their respective national institutions have made the segment reporting mandatory. • AS 17 in India mandates listed and other companies to report their financial information by segments.