Right Issue MEANING The shares of a company

- Slides: 16

Right Issue– MEANING The shares of a company are undoubtedly valuable where the issuing company has been either regularly paying handsome rate of dividend or expected to become a highly profitable one. Demands for the shares of such a company are considerably large and their market price appreciates above the issue price • Right shares are those shares which are issued to existing shareholders. Right shares must be in ratio of equity shares of existing shareholders • Shares are offered to existing shareholders in proportion to their current holdings at a price below market value. • A rights issue will raise some cash for the company and the issue costs involved in a rights issue are lower than a full issue to the public. • A rights issue will reduce the market value of the shares.

Accounting of Right issue Fred, a limited liability company, has 25, 000 $1 shares in issue and makes a rights issue of 10, 000 shares at $1. 50 per share and the issue is fully taken up. What is the double entry to record the above transaction in Fred’s financial statements? Bank Account Share Capital Account Security Premium Account Dr Cr. 15, 000 Cr. 10, 000 5, 000

Underwriting of Right Shares Sometime, company can contract with underwriter who promises that if existing shareholders will not buy, he will takeover all right shares. Underwriters and sub-underwriters may be financial institutions, stock-brokers, major shareholders of the company or other related or unrelated parties.

Slide 10. 4 Bonus shares are shares issued to existing shareholders free of charge. An alternative name often used is scrip issue. If the articles give the power, and the requisite legal formalities are observed, the following may be applied in the issuing of bonus shares: 1. The retained profits; 2. Any other revenue reserve; 3. Any capital reserve, e. g. share premium. Wood and Sangster, Frank Wood's Business Accounting Volume 2 , 13 e © Pearson Education Limited 2016

Bonus Issue Meaning of Bonus: Bonus means premium or gift which is paid normally in cash. A bonus share issue is a distribution of free shares to existing shareholders. The number of bonus shares a shareholder will receive is based on how many shares they own. Reasons for a bonus issue 1. A company has made an extraordinary profit because of good management or a successful strategy. The profit above what was expected is distributed to shareholders in the form of bonus shares. 2. A company may experience a fall in its share price once it is listed on the stock exchange. To compensate shareholders, a bonus issue of shares is distributed. This encourages shareholders to keep their shares and stay loyal to the company instead of selling their holdings and driving the price down further.

How Bonus Shares issued? • A company will issue bonus shares instead of paying a cash dividend. This means that company liquidity is not affected by a large dividend payout. • Bonus share issues are paid out of its reserves, such as retained earnings or the general reserve.

Illustration 2 The directors of Bettawirk Ltd declared a bonus share issue on the basis of one share for every twenty shares of $ 100 each. A shareholder who owns 2000 shares will receive how many bonus shares. What are the entries required: Solution: For 2000 Shares/20= 100 Bonus shares are issued as Bonus. Reserves Accounts Dr 10, 000 To Bonus to Share Holders 10, 000 (Bonus to share holders out of Reserves) Bonus to Share Holders To Share Capital Account (Bonus shares issued out of Bonus to share holders) Dr 10, 000

Illustration 3 Miralou Ltd had an extraordinary first year of trading and profit exceeded the budget. The directors decided to distribute the profit with a bonus share issue on 1 July 2011. The total cost of the issue is $100 000 and it will be paid out of retained earnings. As at 30 June 2010, retained earnings had a balance of $300 000. Solutions: Retained Earning Account Dr Bonus to Shareholders (Bonus to share holders from retained earnings) Bonus to share holders Account Dr Share Capital Account (Bonus shares issued out of bonus to shareholders 100, 000 10, 0000

Source of bonus shares The bonus shares can be issued out of profit or reserve which have been earned by the company profit or reserve should be free for the purpose of dividend as specified in company act. The reserves can not be used for issue of bonus which are not earned by company. The following is the list of reserves which can be used for issuing bonus shares by passing the journal entries under its accounting treatment. 1. Profit and loss account 2. general reserve 3. revenue reserve 4. free reserves 5. dividend equalization fund 6. capital reserve 7. sinking fund 8. debenture redemption reserve only after redemption 9. development rebate reserve 10. allowance after expiry of 8 years 11. capital redemption reserve 12. share premium or security premium if received in cash

Alternatives for Bonus Issues 1 st Case: When the partly paid up shares are converted into fully paid up shares through bonus issue. For providing the amount of bonus out of reserve , then the following journal entry will pass Capital reserve account debit General reserve account debit Revenue reserve account debit Free reserve account debit Dividend equalization fund account debit Profit and loss account debit Bonus to equity shareholders accountcredit xxxx xxxx For amount due on final call of shares ( Existing shares unpaid amount ) Share final call account Share capital account debit xxxx credit xxxx For adjustment of final call amount out of profit Bonus to shareholder account Share final call account debit xxxx credit xxxx

Alternatives for Bonus Issues 2 nd case When new fully paid up bonus shares are issued a) for providing amount of bonus Capital reserve account share premium account Capital redemption reserve account Other general reserve account Profit and loss account Bonus to shareholder account debit debit credit b) for issue of bonus Bonus to equity shareholder account debit Equity share capital account credit xxxx xxxx

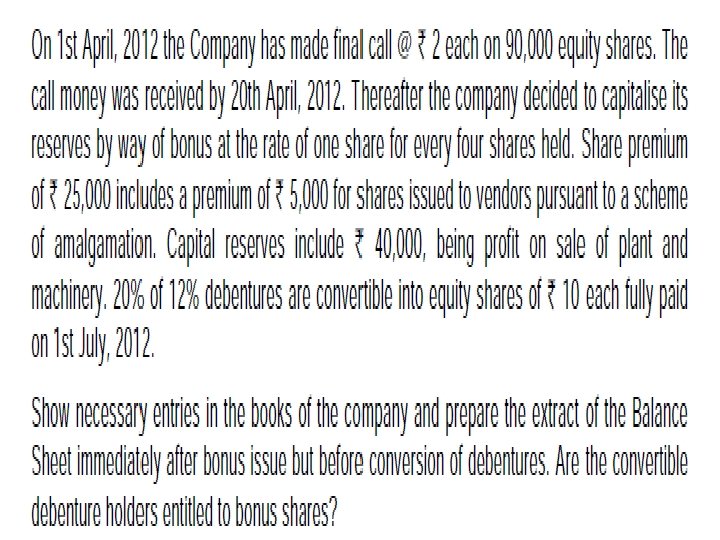

Illustration 4

Illustration 5

Solution

Solution