Review and Summary BoxJenkins models Stationary Time series

, MA(q), ARMA(p, q)")

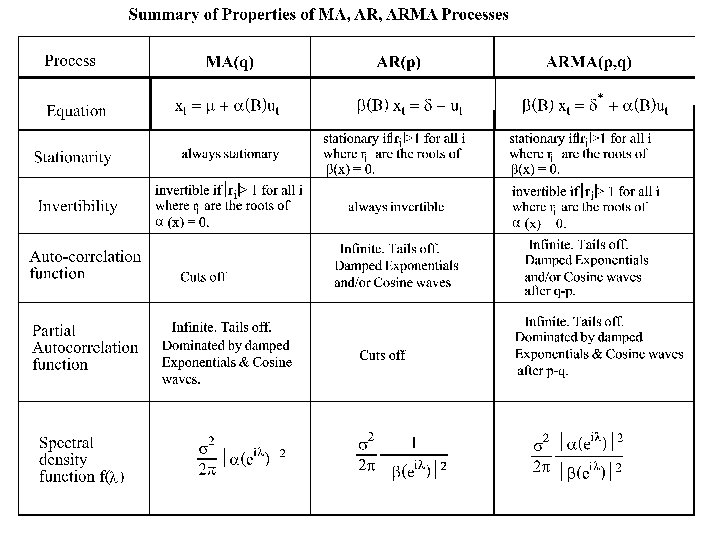

Review and Summary Box-Jenkins models Stationary Time series AR(p), MA(q), ARMA(p, q)

Models for Stationary Time Series.

is a Moving Average time")

The Moving Average Time series of order q, MA(q) is a Moving Average time series of order q. MA(q) if it satisfies the equation: where variance s 2. is a white noise time series with

time series The autocorrelation function for")

The mean The autocovariance function for an MA(q) time series The autocorrelation function for an MA(q) time series

{xt|t T} is called a Autoregressive")

The Autoregressive Time series of order p, AR(p) {xt|t T} is called a Autoregressive time series of order p. AR(p) if it satisfies the equation: where {ut|t T} is a white noise time series with variance s 2.

series The Autocovariance function s(h) of a")

The mean value of a stationary AR(p) series The Autocovariance function s(h) of a stationary AR(p) series Satisfies the equations:

of a stationary AR(p) series Satisfies the equations: with for")

The Autocorrelation function r(h) of a stationary AR(p) series Satisfies the equations: with for h > p and

or: where r 1, r 2, … , rp are the roots of the polynomial and c 1, c 2, … , cp are determined by using the starting values of the sequence r(h).

time series: consider the polynomial with roots r 1, r 2 ,")

Stationarity AR(p) time series: consider the polynomial with roots r 1, r 2 , … , rp 1. then {xt|t T} is stationary if |ri| > 1 for all i. 2. If |ri| < 1 for at least one i then {xt|t T} exhibits deterministic behaviour. 3. If |ri| ≥ 1 and |ri| = 1 for at least one i then {xt|t T} exhibits non-stationary random behaviour.

A Mixed")

The Mixed Autoregressive Moving Average Time Series of order p, ARMA(p, q) A Mixed Autoregressive- Moving Average time series - ARMA(p, q) series {xt: t T} satisfies the equation: where {ut|t T} is a white noise time series with variance s 2,

series Stationary of an ARMA(p, q)")

The mean value of a stationary ARMA(p, q) series Stationary of an ARMA(p, q) series Consider the polynomial with roots r 1, r 2 , … , rp 1. then {xt|t T} is stationary if |ri| > 1 for all i. 2. If |ri| < 1 for at least one i then {xt|t T} exhibits deterministic behaviour. 3. If |ri| ≥ 1 and |ri| = 1 for at least one i then {xt|t T} exhibits non-stationary random behaviour.

satisfies: For h = 0, 1. … , q: for")

The autocovariance function s(h) satisfies: For h = 0, 1. … , q: for h > q:

")

h 0 -1 -2 -3 sux(h)

The partial auto correlation function at lag k is defined to be: Using Cramer’s Rule

A recursive formula for Fkk: Starting with F 11 = r 1 and

")

Spectral density function f(l)

and")

Let {xt: t T} denote a time series with auto covariance function s(h) and let f(l) satisfy: then f(l) is called the spectral density function of the time series {xt: t T}

Linear Filters

Let {xt : t T} be any time series and suppose that the time series {yt : t T} is constructed as follows: : The time series {yt : t T} is said to be constructed from {xt : t T} by means of a Linear Filter. input xt Linear Filter as output yt

Spectral theory for Linear Filters if {yt : t T} is obtained from {xt : t T} by the linear filter:

since")

Applications: The Moving Average Time series of order q, MA(q) since

since")

The Autoregressive Time series of order p, AR(p) since

Time series of order p, q where {zt |t T} is")

The ARMA(p, q) Time series of order p, q where {zt |t T} is a MA(q) time series. since

xt")

Three Important Forms of a Non-Stationary Time Series The Difference equation Form: b(B) xt = d + a(B)ut or xt = b 1 xt-1 + b 2 xt-2 +. . . +bpxt-p + d + ut +a 1 ut-1 + a 2 ut-2 +. . . +aqut-q

ut or xt = m + ut +y")

The Random Shock Form: xt = m+y(B)ut or xt = m + ut +y 1 ut-1 + y 2 ut-2 +y 3 ut-3 +. . . where y(B) = [b(B)]-1 a(B) = = I + y 1 B + y 2 B 2 +y 3 B 3 +. . . m = [b(B)]-1 d = d/(1 - b 2 -. . . - bp) and

xt = t + ut or xt = p 1 xt-1")

The Inverted Form: p(B)xt = t + ut or xt = p 1 xt-1 + p 2 xt-2 +p 3 x 3+. . . + t + ut where p(B) = [a(B)]-1[b(B)] = I - p 1 B - p 2 B 2 - p 3 B 3 -. . .

time series")

Models for Non-Stationary Time Series The ARIMA(p, d, q) time series

An important fact: Most Non-stationary time series have changes that are stationary Recall the time series {xt : t T} defined by the following equation: xt = b 1 xt-1 + ut Then 1) if |b 1| < 1 then the time series {xt : t T} is a stationary time series. 2) if |b 1| = 1 then the time series {xt : t T} is a non stationary time series. 3) if |b 1| > 1 then the time series {xt : t T} is a deterministic time series in nature.

In fact if b 1 = 1 then this equation becomes: xt = xt-1 + ut This is the equation of a well known non stationary time series (called a Random Walk. ) Note: xt - xt-1 = (I - B)xt= Dxt = ut where D = I - B Thus by the simple transformation of computing first differences we can convert the time series {xt : t T} into a stationary time series.

xt")

Now consider the time series, {xt : t T}, defined by the equation: f(B)xt = d + a(B)ut where f(B) = I - f 1 B - f 2 B 2 -. . . - fp+d Bp+d. Let r 1, r 2, . . . , rp+d are the roots of the polynomial f(x) where: f(x) = 1 - f 1 x - f 2 x 2 -. . . - fp+dxp+d.

if |ri| > 1 for i = 1, 2, . . .")

Then 1) if |ri| > 1 for i = 1, 2, . . . , p+d the time series {xt : t T} is a stationary time series. 2) if |ri| = 1 for at least one i (i = 1, 2, . . . , p) and |ri| > 1 for the remaining values of i then the time series {xt : t T} is a non stationary time series. 3) if |ri| < 1 for at least one i (i = 1, 2, . . . , p) then the time series {xt : t T} is a deterministic time series in nature.

are equal to unity then f(x)")

Suppose that d roots of the polynomial f(x) are equal to unity then f(x) can be written: f(B) = (1 - b 1 x - b 2 x 2 -. . . - bpxp)(1 -x)d. and f(B) could be written: f(B) = (I - b 1 B - b 2 B 2 -. . . - bp. Bp)(I-B)d= b(B)Dd. In this case the equation for the time series becomes: f(B)xt = d + a(B)ut or b(B)Dd xt = d + a(B)ut. .

Thus if we let wt = Ddxt then the equation for {wt : t T} becomes: b(B)wt = d + a(B)ut Since the roots of b(B) are all greater than 1 in absolute value then the time series {wt: t T} is a stationary ARMA(p, q) time series. The original time series , {xt : t T}, is called an ARIMA(p, d, q) time series or Integrated Moving Average Autoregressive time series. The reason for this terminology is that in the case that d = 1 then {xt: t T} can be expressed in terms of {wt: t T} as follows: xt = D-1 wt = (I - B)-1 wt = (I + B 2 + B 3 + B 4+. . . )wt = wt + wt-1 + wt-2 + wt-3 + wt-4+. . .

=b(B)Dd is called the generalized autoregressive operator. 2. The")

Comments: 1. The operator f(B) =b(B)Dd is called the generalized autoregressive operator. 2. The operator b(B) is called the autoregressive operator. 3. The operator a(B) is called moving average operator. 4. If d = 0 then t the process is stationary and the level of the process is constant. 5. If d = 1 then the level of the process is randomly changing. 6. If d = 2 thern the slope of the process is randomly changing.

xt = d + a(B)ut")

b(B)xt = d + a(B)ut

Dxt = d + a(B)ut")

b(B)Dxt = d + a(B)ut

D 2 xt = d + a(B)ut")

b(B)D 2 xt = d + a(B)ut

Time Series")

Forecasting for ARIMA(p, d, q) Time Series

Consider the m+n random variables x 1, x 2, . . . , xm, y 1, y 2, . . . , yn with joint density function f(x 1, x 2, . . . , xm, y 1, y 2, . . . , yn) = f(x, y) where x = (x 1, x 2, . . . , xm) and y = (y 1, y 2, . . . , yn).

Then the conditional density of x = (x 1, x 2, . . . , xm) given y = (y 1, y 2, . . . , yn) is defined to be:

= g(x 1, x 2, . .")

In addition the conditional expectation of g(x) = g(x 1, x 2, . . . , xm) given y = (y 1, y 2, . . . , yn) is defined to be:

Prediction

Again consider the m+n random variables x 1, . . . , xm, y 1, . . . , yn. Suppose we are interested in predicting g(x 1, . . . , xm) = g(x) given y = (y 1, y 2, . . . , yn). Let t(y 1, y 2, . . . , yn) = t(y) denote any predictor of g(x 1, x 2, . . . , xm) = g(x) given the information in the observations y = (y 1, y 2, . . . , yn). Then the Mean square error of t(y) in predicting g(x) using t(y) is defined to be MSE[t(y)] = E[{t(y)-g(x)}2 |y]

![It can be shown that the choice of t(y) that minimizes MSE[t(y)] is t(y)](http://slidetodoc.com/presentation_image_h2/21350a7cbda54c8e1d16a39d7a40bec8/image-45.jpg "It can be shown that the choice of t(y) that minimizes MSE[t(y)] is t(y)")

It can be shown that the choice of t(y) that minimizes MSE[t(y)] is t(y) = E[g(x) |y]. Proof: Let v(t) = E{[t-g(x)]2 |y } = E[t 2 -2 tg(x)+g 2(x) |y] = t 2 -2 t. E[g(x)|y]+E[g 2(x) |y]. Then v'(t) = 2 t -2 E[g(x)|y] = 0 when t = E[g(x)|y].

Ddxt =")

Three Important Forms of a Non-Stationary Time Series The Difference equation Form: b(B)Ddxt = d + a(B)ut or f(B)xt = d + a(B)ut or xt = f 1 xt-1 + f 2 xt-2 +. . . +fp+dxt-p-d + ut +a 1 ut-1 + a 2 ut-2 +. . . +aqut-q

+y(B)ut or xt = m(t) + ut")

The Random Shock Form: xt = m(t) +y(B)ut or xt = m(t) + ut +y 1 ut-1 + y 2 ut-2 +y 3 ut-3 +. . . where y(B) = [f(B)]-1 a(B) = [b(B)Dd]-1 a(B) = I + y 1 B + y 2 B 2 +y 3 B 3 +. . . m = [b(B)]-1 d= d/(1 - b 2 -. . . - bp) and m(t) = D-dm

= m i. e. the dth order differences are constant. This implies")

Note: Ddm(t) = m i. e. the dth order differences are constant. This implies that m(t) is a polynomial of degree d.

Ddxt = d + a(B)ut or f(B)xt = d")

Consider The Difference equation Form: b(B)Ddxt = d + a(B)ut or f(B)xt = d + a(B)ut

-1 To get f(B)-1 f(B)xt = f(B)-1 d + f(B)-1")

Multiply both sides by f(B)-1 To get f(B)-1 f(B)xt = f(B)-1 d + f(B)-1 a(B)ut or xt = f(B)-1 d + f(B)-1 a(B)ut

xt = t + ut or xt = p 1 xt-1")

The Inverted Form: p(B)xt = t + ut or xt = p 1 xt-1 + p 2 xt-2 +p 3 x 3+. . . + t + ut where p(B) = [a(B)]-1 f(B) = [a(B)]-1[b(B)Dd] = I - p 1 B - p 2 B 2 - p 3 B 3 -. . .

xt = d + a(B)ut Multiply both sides")

Again Consider The Difference equation Form: f(B)xt = d + a(B)ut Multiply both sides by a(B)-1 To get a(B)-1 f(B)xt = a(B)-1 d + a(B)-1 a(B)ut or p(B) xt = t + ut

Time Series • Let PT denote {…, x. T-2,")

Forecasting an ARIMA(p, d, q) Time Series • Let PT denote {…, x. T-2, x. T-1, x. T} = the “past” til time T. • Then the optimal forecast of x. T+l given PT is denoted by: • This forecast minimizes the mean square error

Three different forms of the forecast 1. Random Shock Form 2. Inverted Form 3. Difference Equation Form Note:

+ ut +y 1")

Random Shock Form of the forecast Recall xt = m(t) + ut +y 1 ut-1 + y 2 ut-2 +y 3 ut-3 +. . . or x. T+l = m(T + l) + u. T+l +y 1 u. T+l-1 + y 2 u. T+l-2 +y 3 u. T+l-3 +. . . Taking expectations of both sides and using

To compute this forecast we need to compute {…, u. T-2, u. T-1, u. T} from {…, x. T-2, x. T-1, x. T}. Note: xt = m(t) + ut +y 1 ut-1 + y 2 ut-2 +y 3 ut-3 +. . . Thus and Which can be calculated recursively

The Error in the forecast: The Mean Sqare Error in the Forecast Hence

100% confidence limits for x. T+l")

Prediction Limits forecasts (1 – a)100% confidence limits for x. T+l

xt = t + ut or xt = p 1 xt-1")

The Inverted Form: p(B)xt = t + ut or xt = p 1 xt-1 + p 2 xt-2 +p 3 x 3+. . . + t + ut where p(B) = [a(B)]-1 f(B) = [a(B)]-1[b(B)Dd] = I - p 1 B - p 2 B 2 - p 3 B 3 -. . .

The Inverted form of the forecast Note: xt = p 1 xt-1 + p 2 xt-2 +. . . + t + ut and for t = T+l x. T+l = p 1 x. T+l-1 + p 2 x. T+l-2 +. . . + t + u. T+l Taking conditional Expectations

The Difference equation form of the forecast x. T+l = f 1 x. T+l-1 + f 2 x. T+l-2 +. . . + fp+dx. T+l-p-d + u. T+l +a 1 u. T+l-1 + a 2 u. T+l-2 +. . . + aqu. T+l-q Taking conditional Expectations

+ ut +")

Example: The Model: xt - xt-1 = b 1(xt-1 - xt-2) + ut + a 1 ut + a 2 ut or xt = (1 + b 1)xt-1 - b 1 xt-2 + ut + a 1 ut + a 2 ut or f(B)xt = b(B)(I-B)xt = a(B)ut where f(x) = 1 - (1 + b 1)x + b 1 x 2 = (1 - b 1 x)(1 -x) and a(x) = 1 + a 1 x + a 2 x 2.

![The Random Shock form of the model: xt =y(B)ut where y(B) = [b(B)(I-B)]-1 a(B)](http://slidetodoc.com/presentation_image_h2/21350a7cbda54c8e1d16a39d7a40bec8/image-63.jpg "The Random Shock form of the model: xt =y(B)ut where y(B) = [b(B)(I-B)]-1 a(B)")

The Random Shock form of the model: xt =y(B)ut where y(B) = [b(B)(I-B)]-1 a(B) = [y(B)]-1 a(B) i. e. y(B) [f(B)] = a(B). Thus (I + y 1 B + y 2 B 2 + y 3 B 3 + y 4 B 4 +. . . )(I - (1 + b 1)B + b 1 B 2) = I + a 1 B + a 2 B 2 Hence a 1 = y 1 - (1 + b 1) or y 1 = 1 + a 1 + b 1. a 2 = y 2 - y 1(1 + b 1) + b 1 or y 2 =y 1(1 + b 1) - b 1 + a 2. 0 = yh - yh-1(1 + b 1) + yh-2 b 1 or yh = yh-1(1 + b 1) - yh-2 b 1 for h ≥ 3.

![The Inverted form of the model: p(B) xt = ut where p(B) = [a(B)]-1](http://slidetodoc.com/presentation_image_h2/21350a7cbda54c8e1d16a39d7a40bec8/image-64.jpg "The Inverted form of the model: p(B) xt = ut where p(B) = [a(B)]-1")

The Inverted form of the model: p(B) xt = ut where p(B) = [a(B)]-1 b(B)(I-B) = [a(B)]-1 f(B) i. e. p(B) [a(B)] = f(B). Thus (I - p 1 B - p 2 B 2 - p 3 B 3 - p 4 B 4 -. . . )(I + a 1 B + a 2 B 2) = I - (1 + b 1)B + b 1 B 2 Hence -(1 + b 1) = a 1 - p 1 or p 1 = 1 + a 1 + b 1 = -p 2 - p 1 a 1 + a 2 or p 2 = -p 1 a 1 - b 1 + a 2. 0 = -ph - ph-1 a 1 - ph-2 a 2 or ph = -(ph-1 a 1 + ph-2 a 2) for h ≥ 3.

Now suppose that b 1 = 0. 80, a 1 = 0. 60 and a 2 = 0. 40 then the Random Shock Form coefficients and the Inverted Form coefficients can easily be computed and are tabled below:

The Forecast Equations

The Difference Form of the Forecast Equation

Computation of the Random Shock Series, Onestep Forecasts One-step Forecasts Random Shock Computations

Computation of the Mean Square Error of the Forecasts and Prediction Limits Mean Square Error of the Forecasts Prediction Limits

Table: MSE of Forecasts to lead time l = 12 (s 2 = 2. 56)

Raw Observations, One-step Ahead Forecasts, Estimated error , Error

Forecasts with 95% and 66. 7% prediction Limits

Graph: Forecasts with 95% and 66. 7% Prediction Limits

Next Topic – Modelling Seasonal Time series

- Slides: 74