Retirement Income Alternative What if When what you

")

Transferring away from you unknowingly and unnecessarily.")

- Slides: 25

Retirement Income Alternative

What if When what you would thought you want to be to true know? wasn’t true?

Life Insurance as an Asset

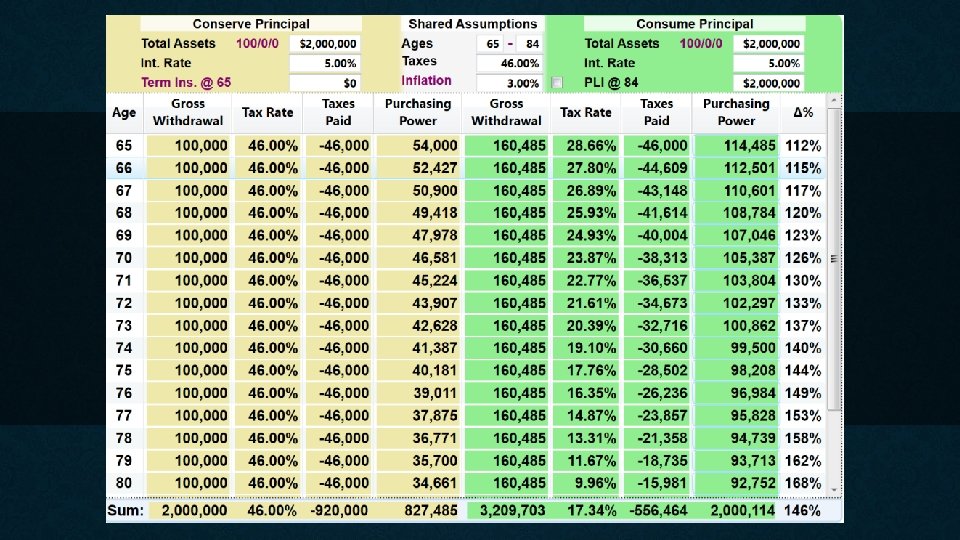

Three Kinds of Money

Three Kinds of Money A

Three Kinds of Money L

Decisions

Decisions – NEEDS vs. WANTS

Three Kinds of Money T

Three Kinds of Money T Transferred ($)

Three Kinds of Money T Transferred ($) Transferring away from you unknowingly and unnecessarily.

Kinds of Transfers T • • • Credit Card Taxes Term Insurance Costs Deductibles Mortgage Payments Loan Investment Final Expenses RRSPs Claw Backs on Government Benefits

The Ideal Investment • • Tax Deferred Growth Tax Free Distributions Competitive Return High Contributions Limits Additional Benefits ( WP ) Collateral Opportunities Safe Harbor

The Ideal Investment • • • No Loss Provisions Guaranteed Loan Options Unstructured Loan Payments Liquidity , Use, and Control By Pass Estate

Human Life Value This is the estimated lump sum needed to replace a lifetime income and services you provide for your family based on a multiple of your income

Client profile • • Need / Want life insurance Have assets they will not use in their lifetime Are ready for a long-term strategy Want to diversify Non –Registered assets growing with tax Alternative retirement strategy Like Dividend performing stocks

Tax-advantaged growth Non-registered investments • Tax-exposed Registered investments • Tax-deferred • Then taxable Participating life insurance • Tax-advantaged • Then tax-free to named beneficiary

Tax-advantaged growth

Stable performance, low risk • Dividends reflect stable performance, low risk – Investment performance – Smoothed returns – Effects of mortality, expenses, taxes • How investments contribute to dividends

Access to Total cash value Cash values • Guaranteed • Dividends • Accumulate over time Access • Policy loans • Withdrawals • Leveraging

Additional deposit option Reasons to pay more than the basic premium • Optimize tax-advantaged growth within policy • Reduce annual taxes on growth of assets outside policy • Accelerate accumulation of cash values • Increase guaranteed values • Increase payment flexibility

Eroding Factors $500, 000 b d. O e n n es Tax on ti Infla T o echn cal logi cen s e l so ce Pla nge a h C t Los me y to nsit e p Pro tun r o p osts C ty i Op su Con te Ra t s e ter t. R arke isk M nd r Inte es sa e g r a t Ch ns a o L In nes i l c De

THANK YOU Questions?