Rental Royalty Income Rental Income A real property

• Rental use is at least one day & personal use")

• Interest $18000 Expense")

• Utilities $")

• Utilities $")

• Utilities $")

• Utilities $")

![Applicable Percentage Depletion Rates Statutory Percentage Natural Resources (Partial list) 5 percent [§ 613(b)(6)]](https://slidetodoc.com/presentation_image/06466d41e28b21f9d6b1e544ef1cf531/image-95.jpg "Applicable Percentage Depletion Rates Statutory Percentage Natural Resources (Partial list) 5 percent [§ 613(b)(6)]")

![Applicable Percentage Depletion Rates Statutory Percentage Natural Resources (Partial list) 5 percent [§ 613(b)(6)]](https://slidetodoc.com/presentation_image/06466d41e28b21f9d6b1e544ef1cf531/image-98.jpg "Applicable Percentage Depletion Rates Statutory Percentage Natural Resources (Partial list) 5 percent [§ 613(b)(6)]")

- Slides: 104

Rental & Royalty Income

Rental Income • A real property trade or business involves the development, redevelopment, construction, reconstruction, acquisition, conversion, rental, operation, management, leasing, or brokering of real property.

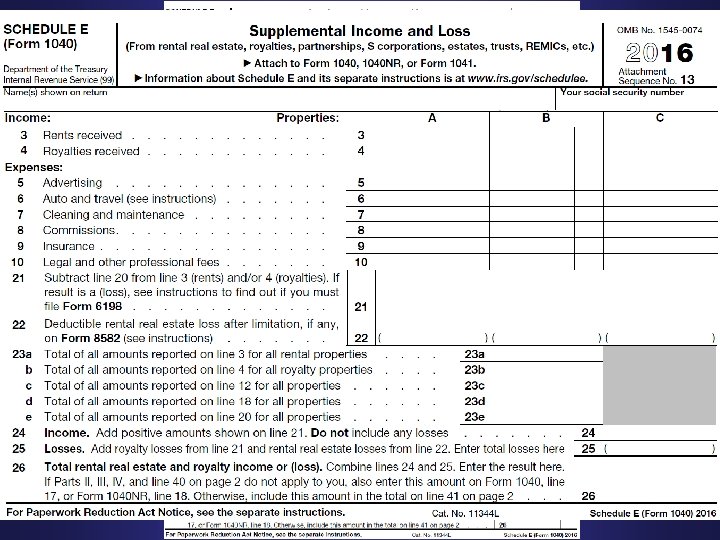

Rental Income falls under the examples of taxable income. Tab B D Table A page D-1, Income Tab, Publication 4012

Rental Income Royalty Income Tab. BI Tab Rental Income is not considered earned income.

Dwelling Unit • Property that provides a place suitable for people to occupy (live or sleep). • For tax purposes it includes: – – – House Condominium Mobile Home Boat Other similar property

Classification of a Dwelling Unit • Dwelling unit can be classified as: – Principal Residence – Residence (not principal) or – Nonresidence (rental property) Note: A taxpayer can have only one principal residence in a tax year, but the residence could change from year to year

Dwelling Unit May be used: – Solely for personal use, – Some mixture of personal & rental use – Solely for rental use • Each year the dwelling unit is classified as either a residence or nonresidence (rental property based on how the unit is used)

Determining whether a dwelling unit is a residence or not • Calculate the number of days the unit was used for personal use during the year & • Calculate the number of days the unit was rented out during the year

Dwelling Unit Considered to be a personal residence if the taxpayer’s number of personal use days of the home is more than the greater of: – 14 days or – 10% of the number of rental days during the year

Rules for Determining the Days of Personal Use Include days when: • Taxpayer or any other owner of the home stay in the home • A relative of an owner stays in the home • A non-owner stays in the home under a vacation home exchange or swap arrangement • The taxpayer rents out the property for less than FMV

Rules for Determining the Days of Rental Use Include: • Days when the taxpayer rents out the property at FMV • Days spent repairing or maintaining the home for rental use

Days Not in Use • Days when the home is available for rent, but not rented out, do not count as either personal or rental days

Principal Residence When a dwelling unit is determined to be a residence, taxpayer must decide if it will be their principal residence in order to determine certain tax consequences

What makes a residence a Principal Residence When a taxpayer lives in more than one residence during the year, the determination of which residence is the principal residence depends facts and circumstances such as: – Amount of time taxpayer spends at each residence – The proximity of each residence to the taxpayers place of employment – The principal place of abode (living or sleeping) of the taxpayer’s immediate family – The taxpayer’s mailing address for bills & correspondence • The taxpayer can have only one principal residence during a particular year but may change it from year to year

Rental Use of Home Tax consequences of owning a second home depends on whether the home qualifies as a residence and on the number of days the taxpayer rents out the home • The home is categorized in one of three ways: – Residence with minimal rental use (rents home for 14 or fewer days) – Residence with significant rental use (rents home for 15 or more days) – Non-residence

Start Was the home used for personal purposes for more than the greater of (1) 14 days or (2) 10% of the total rental days? No Yes Was home rented for 15 days or more? No Residence with Minimal Rental Use Yes Residence with Significant Rental Use Non-residence

Residence with Minimal Rental Use • Taxpayer lives in the home at least 15 days and rents it for 14 days or fewer. – Excludes all rental income – Cannot deduct rental expenses – Allowed to deduct qualified residence interest and real property taxes on second home as itemized deductions

Residence with Significant Rental Use • Rental use is 15 days or more & personal use exceeds the greater of – 14 days or – 10% of rental days • Rental revenue is included in gross income • Deduct direct rental expenses such as advertising and realtor commission • Interest and taxes allocated to personal use deducted as itemized deductions and all other expenses allocated to personal use not deductible • When the gross rental revenue exceeds the sum of the direct rental expenses and the expenses are allocated to the rental use of the home, the taxpayer is allowed to deduct the expenses in full

Residence with Significant Rental Use • When expenses exceed the rental revenue the deductibility of expenses is limited • In these situations, taxpayers divide the rental expenses into one of three categories or Tiers

Rental Income by Tier & Deduction Sequence • Tier 1 – (expenses to obtain tenants & mortgage interest & real property taxes allocated to rental use) Full deductible • Tier 2 – (all other expenses allocated to the rental activity other than depreciation expense including payments for utilities, maintenance, & other direct expenses) limited to gross rental revenue in excess of tier 1 expenses. – Any Tier 2 expenses not deducted are carried forward to the next year • Tier 3 – (depreciation expense) limited to gross rental revenue in excess of tier 1 and tier 2 expenses – Any Tier 3 expenses not deducted are carried forward to the next year

Nonresidence (Rental Property) • Rental use is at least one day & personal use is no more than the greater of – 14 days or – 10% of rental days • Taxpayer includes all revenue • Allocate expenses to rental & personal use • Taxpayers deduct all rental expenses allocated to the rental use of the property as for AGI deductions (on Schedule E) • Rental deduction in excess of rental income are deductible subject to passive loss limitation rules • Interest expense allocated to personal use not deductible

Allocation Method to Rental Use • Expenses associated with the rental use of the home must be allocated between rental use and personal use of the home • These expenses are general allocated to rental use based on the ratio of the number of days of rental use to the total number of days the property was used for rental and personal use • All expenses not allocated to rental use are allocated to personal use and are non-deductible

Allocation Method to Rental Use • The only exception to the general rule involves the allocation of mortgage interest expense and real property taxes. • IRS & Tax Court disagree on the allocation of these expenses • The Tax Court allocates interest and taxes to rental use based on the ratio of days that the property was rented over the number of days in the year • The tax court justifies the approach on the basis that interest and property taxes accrue over the entire year regardless of the level of personal or rental use.

Tax Court vs. IRS Method of Allocating Expenses Rental Allocation IRS Method Tax Court Method Mortgage Interest & Property Taxes Expense x (Total rental days ÷ 365) All other expenses Expense x (Total rental days ÷ Total days used)

Rental Income U. S. citizens and resident aliens must report rental income, regardless of whether the rental property is located in the U. S. or in a foreign country

Rental Income Gross rental income may include other payments in addition to the normal and ordinary rents received, such as: – Advanced rent – Security deposits – Payments for breaking a lease – Expenses paid by the tenant – Fair market value of property or services received in exchange for rental payments

Rental Income The taxpayer’s method of accounting affects when the rental income is reported. – the cash method reports income when received and expenses when paid; – the accrual method reports income when earned and expenses when incurred

Security Deposits • The security deposit is not included in income when the taxpayer plans on returning the deposit at the end of the lease. • However, if the security deposit is intended to serve as the last month’s rent, then it should be included in income when received

Rental Income Taxpayers who do not use the rental home as their residence should: – Include the rent as income & – Deduct all of the rental expenses, even if they exceed income

Reporting Rental Income • Income from Rental Income may be reported on Box 1 of Form 1099 -Misc. This total is the amount of rent received during the year. • Most often rental income is not reported on this form. Any rents received whether in the form of cash, services or property must be included as income.

What are other deductible rental expenses? • • • Advertising Auto and travel expenses to check on the property Cleaning and maintenance Commissions paid for collecting rental income Insurance premiums Property taxes Mortgage interest and points Legal and professional fees Property management fees Repairs Utilities paid for the tenant Other rental-related expenses, such as rental of equipment, long distance phone calls, and condominium/ cooperative maintenance fees

What about Advertising? • Advertising is a direct expense of the rental so it is fully deductible against rental revenue

What about mortgage interest and property taxes? • Mortgage interest and property taxes are deductible as rental expenses. • If the residence (or a portion of the residence) was used as rental property for any part of the year, • the taxpayer must allocate the property tax & mortgage interest deductions between Schedule A and Schedule E.

What about property insurance? • The property insurance that taxpayers pay on their residence is deductible as a rental expense for the time it is considered rental property • Insurance premiums paid more than one year in advance cannot be deducted in one year. • All taxpayers must prorate advanced premium payments over the period covered by the policy.

Can auto and travel expenses be deducted as rental expenses? Taxpayers can deduct ordinary and necessary travel and transportation expenses attributable to the production of rental income. • Taxpayers should substantiate the pleasure vs business portions of the trip and allocate the expenses accordingly • Taxpayers who use their personal automobile for rentalrelated trips may use either the standard mileage rate or the actual expense method for business mileage.

Are repairs and improvements deductible? • A repair keeps the property in good operating condition; the cost is a current-year deduction. • An improvement adds to the life or material value of the property, or adapts it to new uses; the cost must be depreciated over the recovery period for the improvement. • The total cost of an improvement includes material, labor, and installation.

Examples of Repairs & Improvements

How do I handle rental property that the taxpayer also uses? • When the rental property is a portion of the taxpayer’s residence, the rental income and expenses must be allocated separately from the taxpayer’s personal expenses. • Expenses that apply to only the rental part of a property are direct business expenses and should be reported in full on Schedule E. • Expenses that benefit the entire property (indirect expenses) must be divided between rental use and personal use; the rental portion is reported on Schedule E

How should taxpayers report rental expenses that exceed their rental income when they live in the home for part of the year? • If taxpayers rented out a dwelling unit that they also used for personal purposes during the year, they may not be able to deduct all the expenses for the rental part. • Dwelling unit (the unit) means a house, apartment, condominium, or similar property.

Personal Use of Rental Property A day of personal use is any day, or part of a day, that the unit was used by: – The taxpayer for personal purposes – Any other person for personal purposes, if that person owns part of the unit (unless rented to that person under a “shared equity” financing agreement) – Anyone in the taxpayer’s family (or in the family of someone else who owns part of the unit), unless the unit is rented at a fair rental price to that person as his or her main home – Anyone who pays less than a fair rental price for the unit – Anyone under an agreement that lets the taxpayer use some other unit

Exceptions • Taxpayers who used a dwelling unit as their main home may not have to count all that time as “days of personal use. ” • Do not count as personal use any day the taxpayer: – Spends working substantially full time repairing and maintaining the unit, even if a family member used it for recreational purposes on that day or – Used the unit as the taxpayer’s main home before or after renting it or offering it for rent, if the taxpayer rented or tried to rent it for at least 12 consecutive months (or for a period of less than 12 consecutive months at the end of which the taxpayer sold or exchanged the home)

Limitations • There are limitations based on whether the taxpayer used the dwelling unit as a home. • The taxpayer uses the dwelling unit as a home if the taxpayer meets the personal use test: • On Schedule E, question 2, relates to the days the property was use for personal, rental use of the property, or as a qualified joint venture

How do I handle rental losses? • Rental losses are not always fully deductible. • There are two restrictions on how much a loss can offset other sources of income: – At-risk rule – Passive activity law

What is the at-risk rule? • The at-risk rule places a limitation on the amount the taxpayer can deduct as losses from activities often described as tax shelters. • Generally, any loss from an activity subject to the at-risk rules is allowed only to the extent of the total amount the taxpayer has at risk in the activity at the end of the tax year.

What is the passive activity law? • The passive activity law states that passive activity losses can be deducted only from passive activity income. • Passive income does not include salary, dividends, or investments but is generally attributed to such things as rental income. • Therefore, losses that exceed rental income (the passive activity) are not deductible.

Passive vs. Active • The limits on deducting rental losses are affected by the degree to which renting out the property is a passive activity or involves active participation: – Passive rental activity means receiving income mainly from the use of property rather than for services. – Active participation means making significant management decisions, such as approving rental terms, repairs, expenditures, and new tenants. • Taxpayers who use a leasing agent or property manager could be considered active participants if they retain final management rights.

Passive Activities Passive activities - taxpayer does not materially participate or rental activity. ◦ Rental activity considered active if classified as “real property trade or business. ” Active income - material participation (wages or active business income).

Exception • Rental activities are generally considered passive activities. Rental losses are not fully deductible. • However, an exception to the passive activity rule provides that taxpayers who actively participate in the rental activity can use up to $25, 000 of their rental losses to offset any other non-passive income ($12, 500 for married taxpayers filing separately and living apart for the entire year). • Examples of non-passive income are salaries, wages, commissions, tips, self-employment income, interest, dividends, annuities, and some royalties.

What is active participation? • It is considered active participation when taxpayers own at least 10% of the rental property and makes management decisions in a significant and bona fide sense. • Management decisions include approving new tenants, deciding on rental terms, approving expenditure, and similar decisions.

Taxpayers Material Participation – Need only satisfy one of the follow requirements to be active participant • participation is greater than 500 hours/year • participation constitutes almost all the participation in activity • participates for more than 100 hours & it is more than anyone else’s participation • has a total of 500 hours combined in several activities • materially participated in 5 of the preceding 10 years • materially participated in a personal service activity for any 3 years prior • participates on a regular, continuous, and substantial basis based on facts and circumstances

Phase-Out of Offset The amount allowed to offset non-passive income is: – Reduced once the taxpayer’s Adjusted Gross Income (AGI) exceeds $100, 000 ($50, 000 for Married Filing Separately) – Completely phased out when AGI exceeds $150, 000 ($75, 000 for Married Filing Separately)

How are passive rental losses reported? • Taxpayers use Form 8582 to figure the amount of any passive activity loss allowed for the current tax year. • Form 8582 summarizes losses and income from all passive activities. • Generally, taxpayers are not required to file Form 8582 if they have: – Only one passive loss generated from a rental activity and – An AGI of less than $100, 000

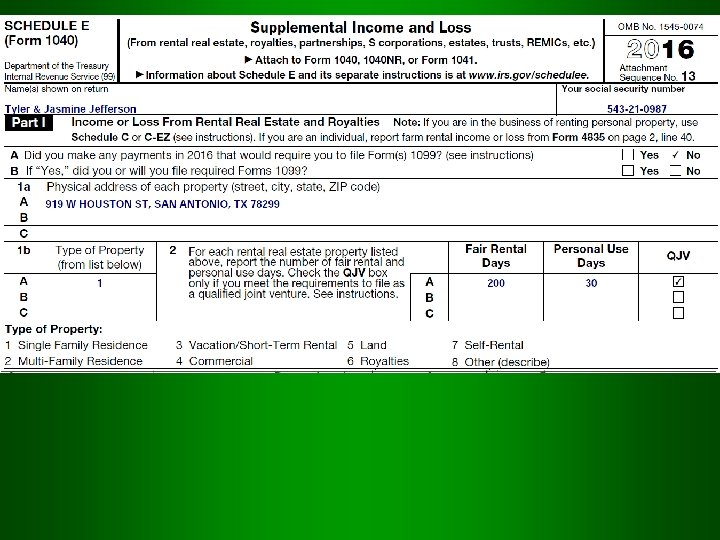

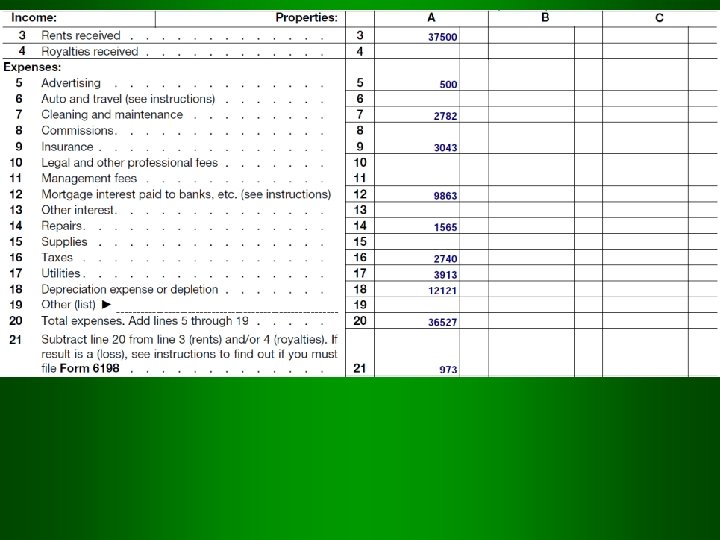

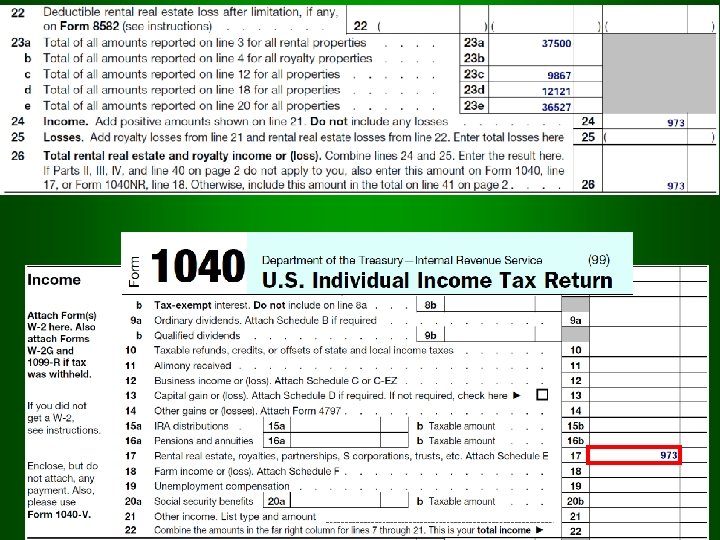

Rental Income • At the beginning of 2016, the Jefferson’s purchased a vacation home in Scottsdale Arizona, for $400, 000. • They paid $100, 000 down and financed the remaining $300, 000 with a 6% mortgage secured by the home. • During the year, the Jefferson’s used the home for personal purposes for 30 days and rented the home for 200 days. • They received $37, 500 of rental revenue and incurred $500 of rental advertising costs.

Expenses for 2016 • • Advertising Interest Real Estate Taxes Utilities Repairs Insurance Maintenance Depreciation $ 500 $18000 $ 5000 $ 4500 $ 1800 $ 3500 $ 3200 $13939

Rental Use of Home Tax consequences of owning a second home depends on whether the home qualifies as a residence and on the number of days the taxpayer rents out the home • The home is categorized in one of three ways: – Residence with minimal rental use – Residence with significant rental use – Nonresidence

Rental Income During the year, the Jefferson’s used the home for personal purposes for 30 days and rented the home for 200 days.

Start During the year, the Jefferson’s used the home for personal purposes for 30 days and rented the home for 200 days Was the home used for personal purposes for more than the greater of (1) 14 days or (2) 10% of the total rental days? 30 ÷ 200 = 15% of Total rental days No Yes Was home rented for 15 days or more? No Residence with Minimal Rental Use Yes Residence with Significant Rental Use Non-residence

Residence with Significant Rental Use • Rental use is 15 days or more & personal use exceeds the greater of – 14 days or – 10% of rental days • Rental revenue is included in gross income • Deduct direct rental expenses such as advertising and realtor commission • Interest and taxes allocated to personal use deducted as itemized deductions and all other expenses allocated to personal use not deductible • When the gross rental revenue exceeds the sum of the direct rental expenses and the expenses are allocated to the rental use of the home, the taxpayer is allowed to deduct the expenses in full

Tax Court vs. IRS Method of Allocating Expenses Rental Allocation IRS Method Tax Court Method Mortgage Interest & Property Taxes Expense x (Total rental days ÷ 365) All other expenses Expense x (Total rental days ÷ Total days used)

Expenses • • Advertising Interest Real Estate Taxes Utilities Repairs Insurance Maintenance Depreciation $ 500* $18000 $ 5000 $ 4500 $ 1800 $ 3500 $ 3200 $13939 *Advertising is a direct expense of the rental so it is fully deductible against rental revenue

Tax Court Method Expense x (Total rental days ÷ 365) • Interest $18000 Expense x (Total rental days ÷ 365) $18, 000 x ( 200 ÷ 365) = $9, 863 • Real Estate Taxes $ 5000 Expense x (Total rental days ÷ 365) $5, 000 x ( 200 ÷ 365) = $2, 740 During the year, the Jefferson’s used the home for personal purposes for 30 days and rented the home for 200 days

Expenses • • Expense Amount Rental Expense Advertising $ 500 Interest $18000 $ 9863 Real Estate Taxes $ 5000 $ 2740 Utilities $ 4500 Repairs $ 1800 Insurance $ 3500 Maintenance $ 3200 Depreciation $13939

IRS Method Expense x (Total rental days ÷ Total days used) • Utilities $ 4500 Expense x (Total rental days ÷ Total days used)

Rental Income • At the beginning of 2016, the Jefferson’s purchased a vacation home in Scottsdale Arizona, for $400, 000. • They paid $100, 000 down and financed the remaining $300, 000 with a 6% mortgage secured by the home. • During the year, the Jefferson’s used the home for personal purposes for 30 days and rented the home for 200 days. • They received $37, 500 of rental revenue and incurred $500 of rental advertising costs.

IRS Method Expense x (Total rental days ÷ Total days used) • Utilities $ 4500 Expense x (Total rental days ÷ Total days used) Total Rental Days = 200 Personal Use Days = 30 Total Days Used = 230

IRS Method Expense x (Total rental days ÷ Total days used) • Utilities $ 4500 Expense x (Total rental days ÷ Total days used) $4500 x (200 ÷ 230) = $3, 913

IRS Method Expense x (Total rental days ÷ Total days used) • Utilities $ 4500 Expense x (Total rental days ÷ Total days used) $4500 x (200 ÷ 230) = $3, 913 • Repairs $ 1800 Expense x (Total rental days ÷ Total days used) $1800 x (200 ÷ 230) = $1, 565 • Insurance $ 3500 Expense x (Total rental days ÷ Total days used) $3500 x (200 ÷ 230) = $3, 043 Maintenance $ 3200 Expense x (Total rental days ÷ Total days used) $3200 x (200 ÷ 230) = $2, 782 Depreciation $13939 Expense x (Total rental days ÷ Total days used) $13939 x (200 ÷ 230) = $12, 121

Expenses • • Expense Amount Rental Expense Advertising $ 500 Interest $18000 $ 9863 Real Estate Taxes $ 5000 $ 2740 Utilities $ 4500 $ 3913 Repairs $ 1800 $ 1565 Insurance $ 3500 $ 3043 Maintenance $ 3200 $ 2782 Depreciation $13939 $12121

Expenses • • Expense Rental Expense Advertising $ 500 Interest $ 9863 Real Estate Taxes $ 2740 Utilities $ 3913 Repairs $ 1565 Insurance $ 3043 Maintenance $ 2782 Depreciation $12121 Tier 1 1 1 2 2 3

Tax Info • Tyler Jefferson • Jasmine Jefferson 543 -21 -0987 564 -11 -1234 • Rental Property Address: – 919 W Houston – San Antonio, TX 78299 • Single Family Residence • Not required to file Form 1099

Rental Income • At the beginning of 2016, the Jefferson’s purchased a vacation home in Scottsdale Arizona, for $400, 000. • They paid $100, 000 down and financed the remaining $300, 000 with a 6% mortgage secured by the home. • During the year, the Jefferson’s used the home for personal purposes for 30 days and rented the home for 200 days. • They received $37, 500 of rental revenue and incurred $500 of rental advertising costs.

Expenses • • Expense Rental Expense Advertising $ 500 Interest $ 9863 Real Estate Taxes $ 2740 Utilities $ 3913 Repairs $ 1565 Insurance $ 3043 Maintenance $ 2782 Depreciation $12121 Tier 1 1 1 2 2 3

Royalty Income

Royalty Income • Royalties from copyrights, patents, and oil, gas, and mineral properties are taxable as ordinary income.

Copyrights and patents • Royalties from copyrights on literary, musical, or artistic works, and similar property, or from patents on inventions, are amounts paid for the right to use work over a specified period of time. • Royalties generally are based on the number of units sold, such as the number of books, tickets to a performance, or machines sold.

Oil, gas, and minerals • Royalty income from oil, gas, and mineral properties is the amount received when natural resources are extracted from property. • The royalties are based on units, such as barrels, tons, etc. , and are paid by a person or company that leases the property.

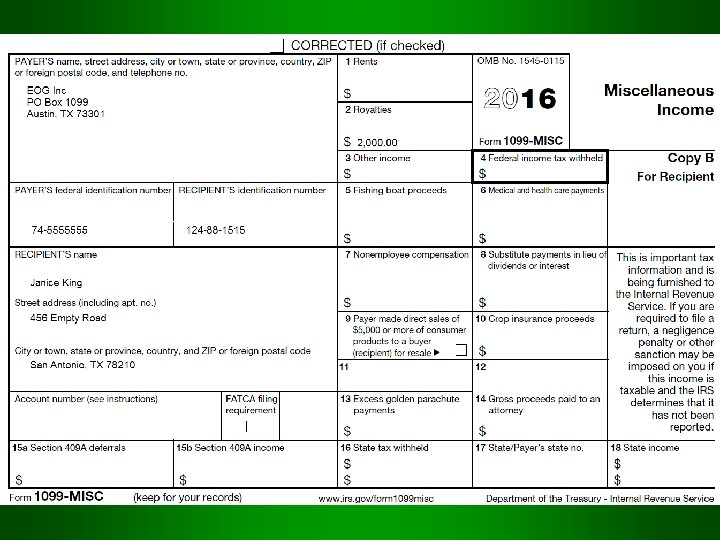

Reporting Royalty Income • Income from Royalties will be reported on Box 2 of Form 1099 -Misc. This amount may be gross or net of any taxes paid on the property.

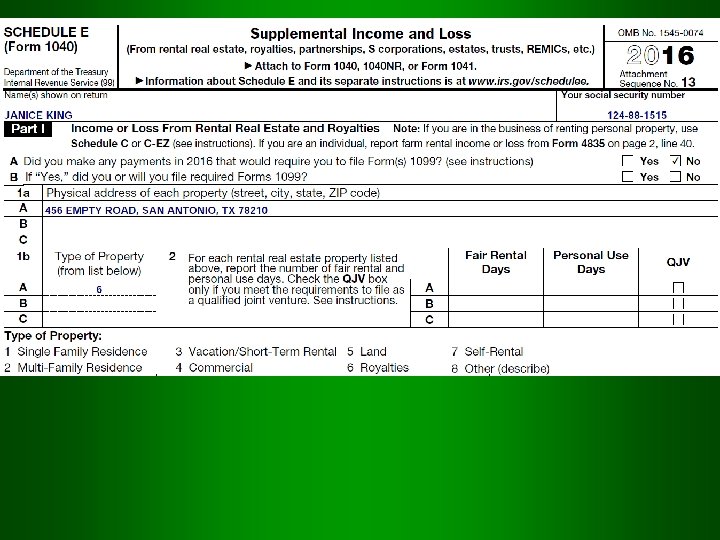

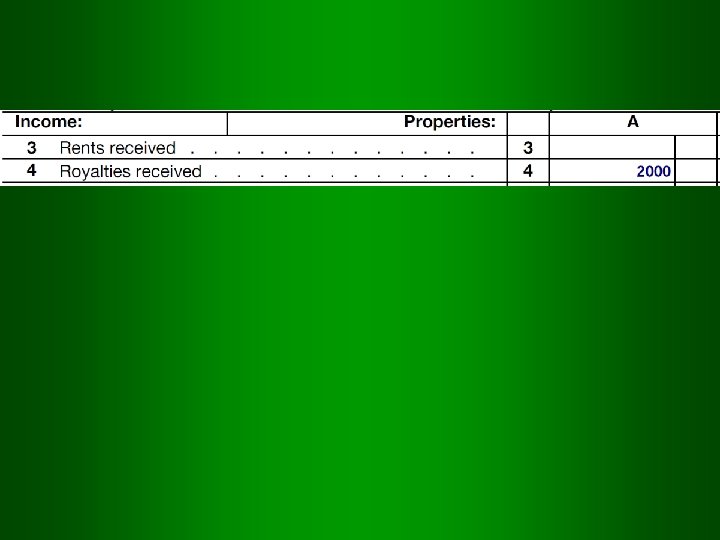

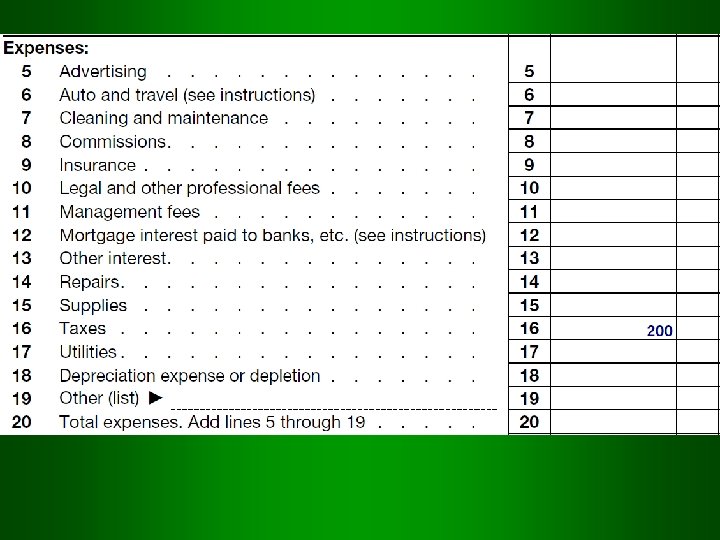

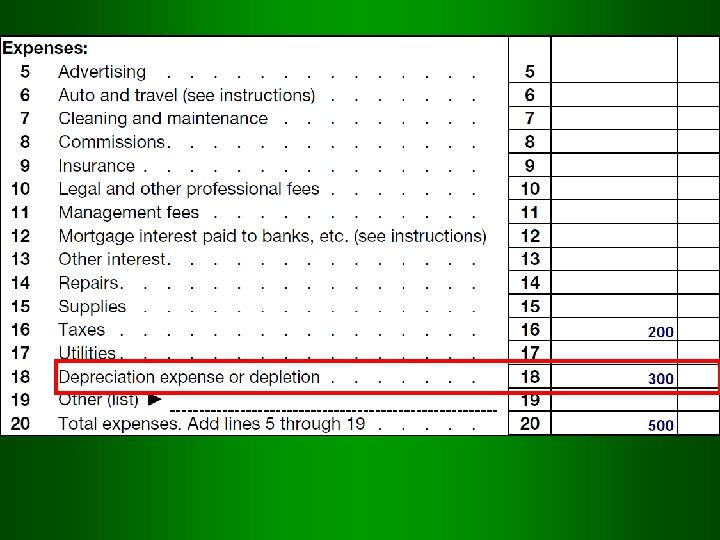

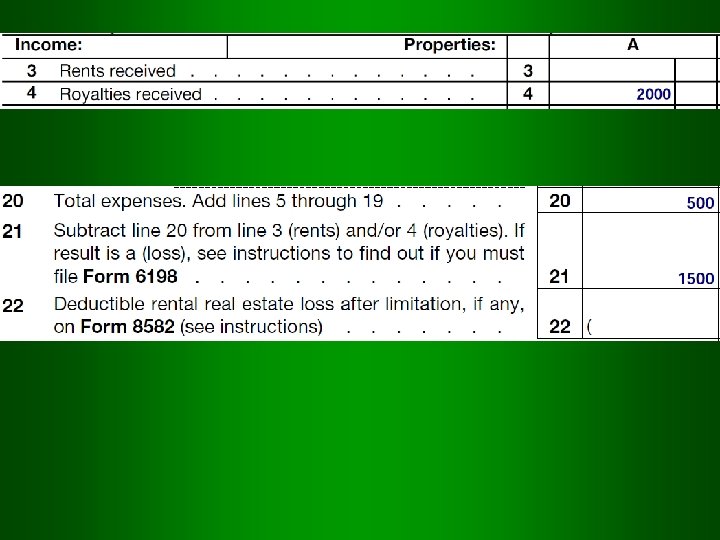

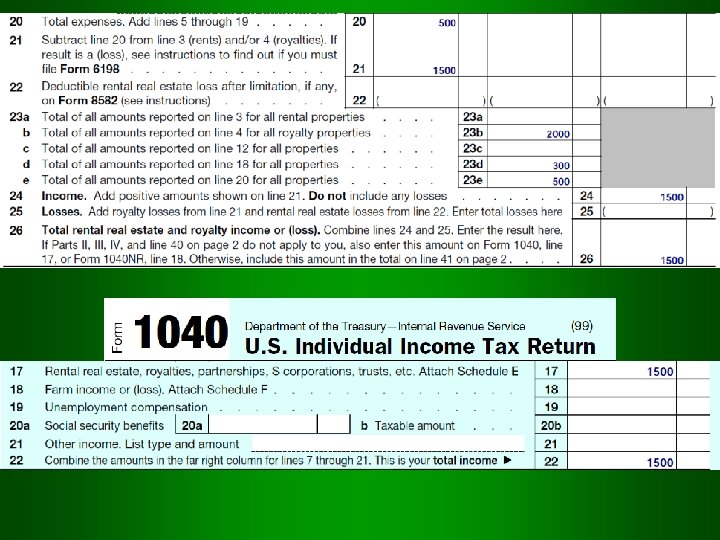

Royalty Income • In 2016, Janice King received royalty income from the excavation of oil from her property. • She receive a 1099 Misc for the royalty income she received. • She paid $200 for property taxes on this land. • She is electing percentage depletion as the cost recovery method for this transaction. • The address of this property is located on the 1099 MISC

Royalty Income • In 2016, Janice King received royalty income from the excavation of oil from her property. • She receive a 1099 Misc for the royalty income she received. • She paid $200 for property taxes on this land. • She is electing percentage depletion as the cost recovery method for this transaction. • The address of this property is located on the 1099 MISC

Royalty Income • In 2015, Janice King received royalty income from the excavation of oil from her property. • She receive a 1099 Misc for the royalty income she received. • She paid $200 for property taxes on this land. • She is electing percentage depletion as the cost recovery method for this transaction. • The address of this property is located on the 1099 MISC

Depletion

Depletion • Cost recovery method used to recover capital investment in natural resources – Examples: mining, oil & gas and forestry industries • Annual depletion is computed using one of two methods – Cost depletion – Percentage depletion • Taxpayers may expense the larger of cost or percentage depletion

Depletion – Cost Depletion • Involves estimating resources reserves and allocating a pro-rata share of basis based on the number of units extracted – Examples: tons of coal, barrels of oil, board feet of lumber

Depletion – Percentage Depletion • Determined by a statutory percentage of gross income that is permitted to be expensed each year. • Different resources have different statutory percentages

Applicable Percentage Depletion Rates Statutory Percentage Natural Resources (Partial list) 5 percent [§ 613(b)(6)] Gravel, pumice, & stone 10 percent Coal, Asbestos 14 percent [§ 613(b)(3)] Asphalt rock, clay, all other metals & minerals Gold, copper, oil shale, iron ore & silver 15 percent [§ 613(b)(2)] 15 percent [§ 613 A(c)(1)] Domestic oil & gas 22 percent [§ 613(b)(1)] Platinum, sulfur, uranium, & titanium Page 10 -23

Depletion • Businesses can deduct depletion under either method until the cost basis is exhausted. • Once the cost basis is exhausted, business are allowed to continue to compute for depletion only under the percentage method • Businesses deduct percentage of depletion when they sell the natural resource and deduct cost depletion in the year they produce or extract the natural resource

Royalty Income • In 2015, Janice King received royalty income from the excavation of oil from her property. • She receive a 1099 Misc for the royalty income she received. • She paid $200 for property taxes on this land. • She is electing percentage depletion as the cost recovery method for this transaction. • The address of this property is located on the 1099 MISC

Applicable Percentage Depletion Rates Statutory Percentage Natural Resources (Partial list) 5 percent [§ 613(b)(6)] Gravel, pumice, & stone 10 percent Coal, Asbestos 14 percent [§ 613(b)(3)] Asphalt rock, clay, all other metals & minerals Gold, copper, oil shale, iron ore & silver 15 percent [§ 613(b)(2)] 15 percent [§ 613 A(c)(1)] Domestic oil & gas 22 percent [§ 613(b)(1)] Platinum, sulfur, uranium, & titanium Page 10 -23

Formula for Percentage Depletion Expense Royalties X Percentage Depletion Rate

Formula for Percentage Depletion Expense Royalties X Percentage Depletion Rate $2, 000 X 15 % = $300