RECEIVABLES MANAGEMENT COSTS OF RECEIVABLES MANAGEMENT OPPORTUNITY COST

RECEIVABLES MANAGEMENT

COSTS OF RECEIVABLES MANAGEMENT � OPPORTUNITY COST � COLLECTION COST � BAD DEBTS � INCREASED SALES � INCREASE IN MARKET SHARE � INCREASE IN PROFITS

COVERAGE • Terms of Payment • Credit Policy Variables • Credit Evaluation • Credit Granting Decision • Control of Accounts Receivable • Credit Management in India

TERMS OF PAYMENT • Cash Mode • Open Account • Bill of Exchange • Letter of Credit • Consignment

CREDIT POLICY VARIABLES The important dimensions of a firm’s credit policy are: • Credit standards • Credit period • Cash discount • Collection effort

CREDIT STANDARDS Liberal Stiff • Sales Higher Lower • Bad debt loss Higher Lower • Investment in receivables Larger Smaller • Collection costs Higher Lower

![IMPACT ON RESIDUAL INCOME OF RELAXATION P = [ S(1 – V) - Sbn]](http://slidetodoc.com/presentation_image_h/bae4a52f794ddc0fd46ce915427e5909/image-7.jpg "IMPACT ON RESIDUAL INCOME OF RELAXATION P = [ S(1 – V) - Sbn]")

IMPACT ON RESIDUAL INCOME OF RELAXATION P = [ S(1 – V) - Sbn] (1 – t ) – k I where P = change in Profit S = increase in sales V = ratio if variable costs to sales bn = bad debt loss ratio on new sales t = corporate tax rate I = increase in receivables investment

Q. PSD Ltd. is considering relaxing its credit standards. S = Rs. 15 million, bn = 0. 10, V = 0. 80, ACP = 40 days, k = 0. 10, t = 0. 4 P = [15, 000 (1 – 0. 80) – 15, 000 x 0. 10] (1 – 0. 4) – 0. 10 x 15, 000 360 = Rs. 766, 667 x 40 x 0. 80

CREDIT PERIOD Longer Shorter • Sales Higher Lower • Investment in Larger Smaller Higher Lower receivables • Bad debts

")

IMPACT ON RESIDUAL INCOME OF LONGER CREDIT PERIOD P = [ S(1 – V) - Sbn] (1 – t ) – k I

where: I S 0")

INCREASE IN RECEIVABLES INVESTMENT I = (ACPn – ACP 0) where: I S 0 360 S + V (ACPn) 360 = increase in receivables investment ACPn = new average collection period (after lengthening the credit period) ACP 0 = old average collection period V S = ratio of variable cost to sales = increase in sales

Q. X Limited is considering extending its credit period from 30 to 60 days. S = Rs. 50 million, S = Rs. 5 million, V = 0. 85, bn = 0. 08, k = 0. 10, t = 0. 40 P = [5, 000 x 0. 15 – 5, 000 x 0. 08] (0. 6) 50, 000 5, 000 – 0. 10 (60 – 30) x + 0. 85 x 60 x 360 = [750, 000 – 400, 000] (0. 6) – 0. 10 [4, 166, 667 + 708, 333] = – 277, 500

![LIBERALISING THE CASH DISCOUNT POLICY P = [ S(1 – V) - DIS] (1](http://slidetodoc.com/presentation_image_h/bae4a52f794ddc0fd46ce915427e5909/image-13.jpg "LIBERALISING THE CASH DISCOUNT POLICY P = [ S(1 – V) - DIS] (1")

LIBERALISING THE CASH DISCOUNT POLICY P = [ S(1 – V) - DIS] (1 – t ) + k I

![DECREASING THE RIGOUR OF COLLECTION PROGRAMME RI = [ S(1 – V) - BD]](http://slidetodoc.com/presentation_image_h/bae4a52f794ddc0fd46ce915427e5909/image-14.jpg "DECREASING THE RIGOUR OF COLLECTION PROGRAMME RI = [ S(1 – V) - BD]")

DECREASING THE RIGOUR OF COLLECTION PROGRAMME RI = [ S(1 – V) - BD] (1 – t ) – k I

TRADITIONAL CREDIT ANALYSIS Five Cs of Credit Character : The willingness of the customer to honour his obligations Capacity : The operating cash flows of the customer Capital : The financial reserves of the customer Collateral : The security offered by the customer Conditions : The general economic conditions that affect the customer Case History : Checking customers past transaction to extend credit to the customer

• AGEING")

MONITORING OF ACCOUNTS RECEIVABLES • RECEIVABLES TURNOVER • AVERAGE COLLECTION PERIOD (ACP) • AGEING SCHEDULE • COLLECTION MATRIX

RECEIVABLES TURNOVER � How quickly RECEIVABLES are CONVERTED in to CASH Receivables Turnover Rate = Total Net Sales Avg. Debtors* (*including Bills Receivables)

� � Time (no. of Days) the Credit Sales are")

AVERAGE COLLECTION PERIOD (ACP) � � Time (no. of Days) the Credit Sales are converted In to Cash ACP= 365/ Receivables Turnover

AGEING SCHEDULE � � Statement showing AGE WISE GROUPING OF DEBTORS OR � � � Breaking up of Debtors according to the LENGTH OF TIME for which they have been OUTSTANDING

Amount Outstanding (Rs. ) Percentage of Debtors to Total Debtors")

Age Group (in Days) Amount Outstanding (Rs. ) Percentage of Debtors to Total Debtors Less Than 30 40, 000 40 31 -45 20, 000 20 46 -60 30, 000 30 Above 60 10, 000 10 Total 1, 00, 000 100

for the CREDIT SALES")

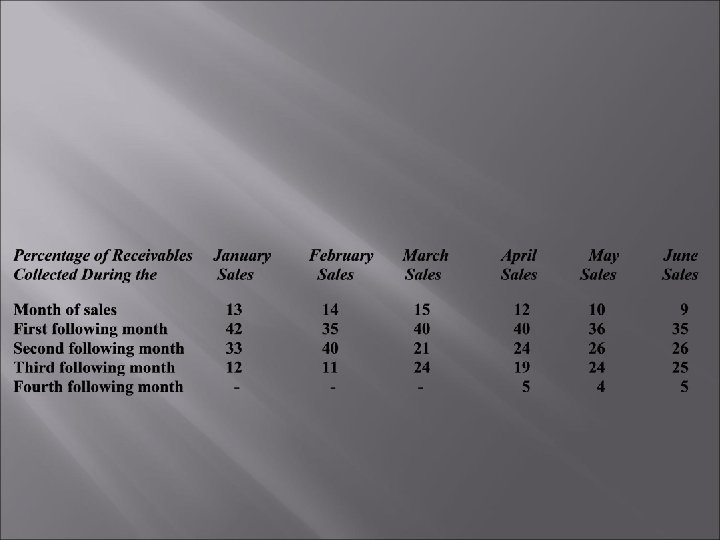

COLLECTION MATRIX � � Shows the collection pattern (in months) for the CREDIT SALES made in a month

- Slides: 22