Recap Accounting Process Prepared by Mubashar majeed Introduction

Recap Accounting Process Prepared by Mubashar majeed

Introduction to Financial Statements • Companies prepare interim financial statements • and annual financial statements.

Introduction to Financial Statements Balance Sheet Income Statement of Cash Flows Three primary financial statements. We will use a corporation to describe these statements.

Introduction to Financial Statements Balance Sheet Income Statement of Cash Flows Describes where the enterprise stands at a specific date. Depicts the revenue and expenses for a designated period of time. Mc. Graw-Hill/Irwin © The Mc. Graw-Hill Companies, Inc. , 2002

The Concept of the Business Entity Vagabond Travel Agency A business entity is separate from the personal affairs of its owner.

Assets and Liabilities • Assets are economic resources that are owned by the business and are expected to provide positive future cash flows. • Liabilities are debts that represent negative future cash flows for the enterprise. • Owners’ equity represents the owner’s claim to the assets of the business.

The Accounting Equation Assets = Liabilities + Owners’ Equity $300, 000 = $80, 000 + $220, 000

Debit and Credit Rules Debits and credits affect accounts as follows: A = L + OE ASSETS LIABILITIES EQUITIES Debit Credit for Increase Debit Credit for Decrease Increase

Double Entry Accounting The Equality of Debits and Credits A = L + OE = Debit balances Credit balances In the double-entry accounting system, every transaction is recorded by equal dollar amounts of debits and credits.

¶ May 1: Jill Jones and her family invested $8, 000 in JJ’s Lawn Care Service and received 800 shares of stock. Will Cash increase or decrease? Will Capital Stock increase or decrease?

¶ May 1: Jill Jones and her family invested $8, 000 in JJ’s Lawn Care Service and received 800 shares of stock. Cash increases $8, 000 with a debit. Capital Stock increases $8, 000 with a credit.

· May 2: JJ’s purchased a riding lawn mower for $2, 500 cash. Will Cash increase or decrease? Will Tools & Equipment increase or decrease?

· May 2: JJ’s purchased a riding lawn mower for $2, 500 cash. Cash decreases $2, 500 with a credit. Tools & Equipment increases $2, 500 with a debit.

¸ May 8: JJ’s purchased a $15, 000 truck. JJ’s paid $2, 000 down in cash and issued a note payable for the remaining $13, 000. Will Truck increase or decrease? Will Cash and Notes Payable increase or decrease?

¸ May 8: JJ’s purchased a $15, 000 truck. JJ’s paid $2, 000 down in cash and issued a note payable for the remaining $13, 000. Truck increases $15, 000 with a debit. Cash decreases $2, 000 with a credit. Notes Payable increases $13, 000 with a credit.

The Journal In an actual accounting system, transactions are initially recorded in the journal.

Posting Journal Entries to the Ledger Accounts Posting involves copying information from the journal to the ledger accounts.

The Ledger Cash Accounts Payable Capital Stock Accounts are individual records showing increases and decreases. The entire group of accounts is kept together in an accounting record called a ledger.

The Use of Accounts Increases are recorded on one side of the Taccount, and decreases are recorded on the other side. Title of Account Left or Debit Side Right or Credit Side

Debit and Credit Entries Receipts are on the debit side. Payments are on the credit side. The balance is the difference between the debit and credit entries in the account.

Posting Journal Entries to the Ledger Accounts

Posting Journal Entries to the Ledger Accounts

Ledger Accounts After Posting This ledger format is referred to as a running balance (as opposed to simple T accounts).

What is Net Income? Net income is not an asset it’s an increase in owners’ equity from profits of the business. A = L + OE Increase Decrease Either (or both) of these effects occur as net income is earned. . . Increase . . . but this is what “net income” really means.

Retained Earnings A = L + OE Capital Stock Retained Earnings The balance in the Retained Earnings account represents the total net income of the corporation over the entire lifetime of the business, less all amounts which have been distributed to the stockholders as dividends.

Revenue and Expenses The price for goods sold and services rendered during a given accounting period. The costs of goods and services used up in the process of earning revenue. Increases owner’s equity. Decreases owner’s equity.

The Realization Principle: When To Record Revenue Realization Principle Revenue should be recognized at the time goods are sold and services are rendered.

The Matching Principle: When To Record Expenses Matching Principle Expenses should be recorded in the period in which they are used up.

Debits and Credits for Revenue and Expenses decrease owner’s equity. EQUITIES Debit Credit for Decrease Increase Revenues increase owner’s equity. EXPENSES REVENUES Debit Credit for Increase Debit Credit for Decrease Increase

Let’s analyze the revenue, and expense transactions for JJ’s Lawn Care Service for the month of May. We will also analyze a dividend transaction.

½ May 29: JJ’s provided lawn care services for a client and received $750 in cash. Will Cash increase or decrease? Will Sales Revenue increase or decrease?

½ May 29: JJ’s provided lawn care services for a client and received $750 in cash. Cash increases $750 with a debit. Sales Revenue increases $750 with a credit.

¾ May 31: JJ’s purchased gasoline for the lawn mower and the truck for $50 cash. Will Cash increase or decrease? Will Gasoline Expense increase or decrease?

¾ May 31: JJ’s purchased gasoline for the lawn mower and the truck for $50 cash. Cash decreases $50 with a credit. Gasoline Expense increases $50 with a debit.

¿ May 31: JJ’s Lawn Care paid Jill Jones and her family a $200 dividend. Will Cash increase or decrease? Will Dividends increase or decrease?

¿ May 31: JJ’s Lawn Care paid Jill Jones and her family a $200 dividend. Cash decreases $200 with a credit. Dividends increase $200 with a debit.

Now, let’s look at the Trial Balance for JJ’s Lawn Care Service for the month of May.

All balances are taken from the ledger accounts on May 31 after considering all of JJ’s transactions for the month. Proves equality of debits and credits.

The Accounting Cycle Journalize transactions. Post entries to the ledger accounts. Prepare trial balance. Prepare after closing Journalize and post closing trial balance. entries. Prepare financial statements. Make end-ofyear adjustments. Prepare adjusted trial balance.

Adjusting Entries • THE ACCOUNTING CYCLE: • Accruals and Deferrals

At the end of the period, we need to make adjusting entries to get the accounts up to date for the financial statements.

Adjusting Entries Adjusting entries are needed whenever revenue or expenses affect more than one accounting period. Every adjusting entry involves a change in either a revenue or expense and an asset or liability.

Types of adjustment • Two types of adjustment • 1 - Deferrals • Result from prepayments made or received • E. g. Payment of six month rent paid or received • 2 - Accrual • These are items are unrecorded , unpaid or not yet received • E. g. Salaries payable, Services revenue receivable

Adjustment Deferral Prepaid Expense ………. Prepaid Accrual Depreciation Expense Unearned Revenue Dep. Exp. Accumulated Dep. Unearned Revenue Accrued Expenses Payable Accrued Revenue A/R Revenue

Rules for Adjusting Entries • Affect 1 Income statement account • Affect 1 balance sheet account • Cash account is never be involved

Converting Assets to Expenses $2, 400 Insurance Policy Coverage for 12 Months $200 Monthly Insurance Expense Jan. 1 Dec. 31 On January 1, Webb Co. purchased a oneyear insurance policy for $2, 400.

Converting Assets to Expenses Initially, costs that benefit more than one accounting period are recorded as assets.

Converting Assets to Expenses The costs are expensed as they are used to generate revenue.

Converting Assets to Expenses Balance Sheet Income Statement Cost of assets that benefit future periods. Cost of assets used this period to generate revenue.

The Concept of Depreciation Depreciable assets are physical objects that retain their size and shape but lose their economic usefulness over time. Depreciation is the systematic allocation of the cost of a depreciable asset to expense.

Depreciation Is Only an Estimate On May 2, 2003, JJ’s Lawn Care Service purchased a lawn mower with a useful life of 50 months for $2, 500 cash. Using the straight-line method, calculate the monthly depreciation expense. Depreciation Cost of the asset expense (per = Estimated useful life period) $50 = $2, 500 50

Depreciation Is Only an Estimate JJ’s Lawn Care Service would make the following adjusting entry. Contra-asset

Depreciation Is Only an Estimate JJ’s $15, 000 truck is depreciated over 60 months as follows: $15, 000 60 months = $250 per month

Accumulated depreciation would appear on the balance sheet as follows:

Converting Liabilities to Revenue End of Current Period Prior Periods Transaction Collected from customers in advance (creates a liability). Current Period Future Periods Adjusting Entry ŒRecognize portion earned as revenue, and Reduce balance of liability account.

Converting Liabilities to Revenue Examples Include: Airline Ticket Sales Sports Teams’ Sales of Season Tickets

Converting Liabilities to Revenue $6, 000 Rental Contract Coverage for 12 Months $500 Monthly Rental Revenue Jan. 1 Dec. 31 On January 1, Webb Co. received $6, 000 in advance for a one-year rental contract.

Converting Liabilities to Revenue Initially, revenues that benefit more than one accounting period are recorded as liabilities.

Converting Liabilities to Revenue Over time, the revenue is recognized as it is earned.

Converting Liabilities to Revenue Balance Sheet Income Statement Liability for future periods. Revenue earned this period.

Accruing Unpaid Expenses End of Current Period Prior Periods Current Period Adjusting Entry ŒRecognize expense incurred, and Record liability for future payment. Future Periods Transaction Liability will be paid.

Accruing Unpaid Expenses Hey, when do we get paid? Examples Include: Interest Wages and Salaries Property Taxes

Accruing Unpaid Expenses $3, 000 Wages Expense Monday, May 29 Wednesday, May 31 Friday, June 2 On May 31, Webb Co. owes wages of $3, 000. Pay day is Friday, June 2.

Accruing Unpaid Expenses Initially, an expense and a liability are recorded.

Accruing Unpaid Expenses Balance Sheet Income Statement Liability to be paid in a future period. Cost incurred this period to generate revenue.

Accruing Unpaid Expenses $5, 000 Weekly Wages $3, 000 Wages Expense Monday, May 29 $2, 000 Wages Expense Wednesday, May 31 Friday, June 2 Let’s look at the entry for June 2.

Accruing Unpaid Expenses The liability is extinguished when the debt is paid.

Accruing Uncollected Revenue End of Current Period Prior Periods Current Period Adjusting Entry ŒRecognize revenue earned but not yet recorded, and Record receivable. Future Periods Transaction Receivable will be collected.

Accruing Uncollected Revenue Examples Include: Interest Earned Work Completed But Not Yet Billed to Customer

Accruing Uncollected Revenue $170 Interest Revenue Saturday, Jan. 15 Monday, Jan. 31 Tuesday, Feb. 15 On Jan. 31, the bank owes Webb Co. interest of $170. Interest is paid on the 15 th day of each month.

Accruing Uncollected Revenue Initially, the revenue is recognized and a receivable is created.

Accruing Uncollected Revenue Balance Sheet Receivable to be collected in a future period. Income Statement Revenue earned this period.

Accruing Uncollected Revenue $320 Monthly Interest $170 Interest Revenue Saturday, Jan. 15 $150 Interest Revenue Monday, Jan. 31 Tuesday, Feb. 15 Let’s look at the entry for February 15.

Accruing Uncollected Revenue The receivable is collected in a future period.

Accruing Income Taxes Expense: The Final Adjusting Entry As a corporation earns taxable income, it incurs income taxes expense, and also a liability to governmental tax authorities.

Effects of the Adjusting Entries Journalize transactions. Post entries to the ledger accounts. Prepare trial balance. Recall from the accounting cycle discussed in Chapter 3, that after the adjusting entries are made, an adjusted trial balance is prepared. Make end-ofyear adjustments. Prepare adjusted trial balance.

THE ACCOUNTING CYCLE: Reporting Financial Results

This is the Adjusted Trial Balance for JJ’s. Now, let’s prepare the financial statements for JJ’s Lawn Care Service for May.

Net income also appears on the Statement of Owner’s Equity.

Statement of Retained Earnings This statement summarizes the increases and decreases in Retained Earnings during the period. • Business Earnings • Dividends • Business Losses

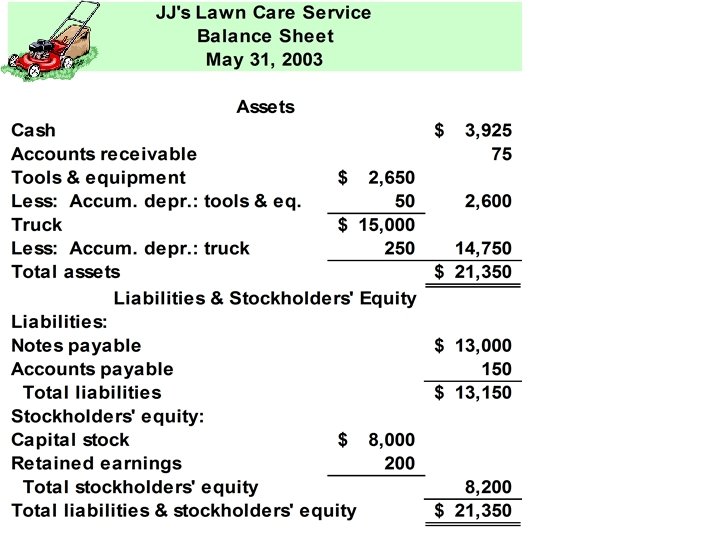

Now, let’s prepare the Balance Sheet.

Closing the Temporary Equity Accounts Œ Close Revenue accounts to Income Summary. Close Expense accounts to Income Summary. Ž Close Income Summary account to Retained Earnings. Close Dividends to Retained Earnings. The closing process gets the temporary accounts ready for the next accounting period.

Closing Entries for Revenue Accounts Since Sales Revenue has a credit balance, the closing entry requires a debit to the Sales Revenue account.

Closing Entries for Revenue Accounts

Closing Entries for Expense Accounts Since expense accounts have a debit balance, the closing entry requires a credit to the expense accounts.

Closing Entries for Expense Accounts Net Income

Closing the Income Summary Account Since Income Summary has a $400 credit balance, the closing entry requires a debit to Income Summary.

Closing the Income Summary Account The balance in Income Summary is now zero.

After all closing entries are made, JJ’s After-Closing Trial Balance looks like this.

End of Topic

- Slides: 91