QUALITATIVE INTERNAL CONTROL COMPLIANCE MONITORING Central Services Administrator

- Slides: 12

QUALITATIVE INTERNAL CONTROL & COMPLIANCE MONITORING Central Services Administrator Meeting April 27, 2017

QUANTITATIVE VERSUS QUALITATIVE FACTORS • Quantitative • Materially measurable criteria • Financial statement elements • Performance ratios • Direct inputs • Less susceptible to subjectivity • Numeric materiality threshold for misstatements • Qualitative • Criteria usually reviewed with an answer of: Yes; No; or Substantially Acheived • More subjectivity involved • Compliance related • Environmental factors • Customer satisfaction

HOW DO I MEASURE IF NOT BY A NUMERIC VALUE & WHERE DOES THIS LEAD? • Begin with your object to achieve • Select the Qualitative criteria to measure against • Use a Quantitative factor for selection of items to review • Build a testing plan for the Qualitative factor • Perform testing • Report on compliance with Qualitative criteria and other findings

SELECT QUALITATIVE CRITERIA AND OBJECTIVE TO BE MET Lodging Rate Policies Instate: Allowance was $89 per night, without taxes and fees, unless: the area is defined as being ‘high cost’ or deviation is further justified Montana High Cost Counties Max. Amount Allowed Various cities (but allowance covers entire county): Gallatin Oct 1 – May 31 $ 89 June 1 – Sept 30 $138 Bozeman, Belgrade, Big Sky, West Yellowstone Silver Bow $93 Butte Richland/Dawson $146 Sidney, Glendive Lewis & Clark $92 Helena Missoula/Lake/Flathead Oct 1 – June 30 $ 95 July 1 – Aug 31 $136 Sept 1 – Sept 30 $ 95 Missoula, Seeley Lake, Polson, Kalispell, Whitefish Out-of-State: Allowance is GSA established rates, unless high cost justification form is submitted and approved by management

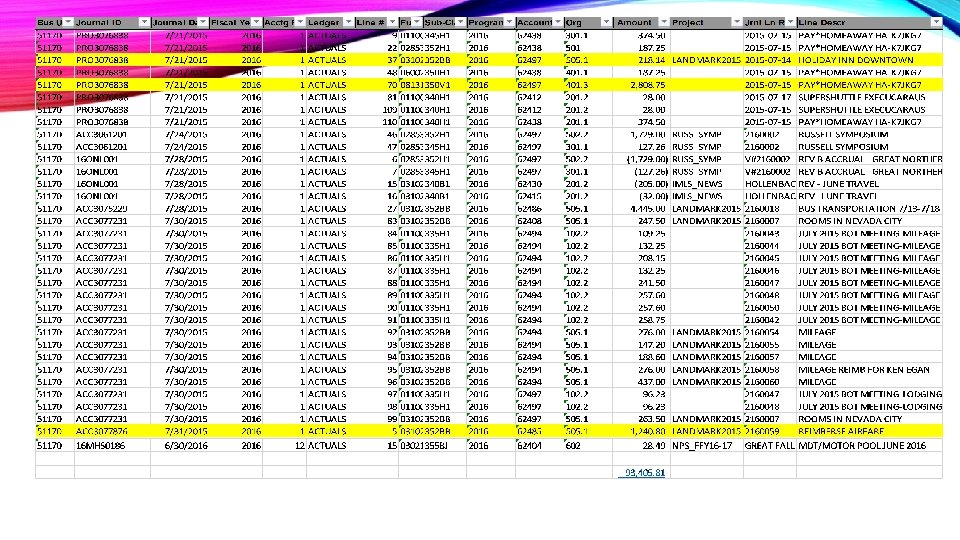

BUILD A TESTING PLAN • Select sample items to test through one of these methods: • Haphazard • Random • Judgmental

TESTING, TESTING 1, 2, 3 … • Judgmental sampling used Item appeared to be of an unusual nature Item appeared to be out of line with criteria

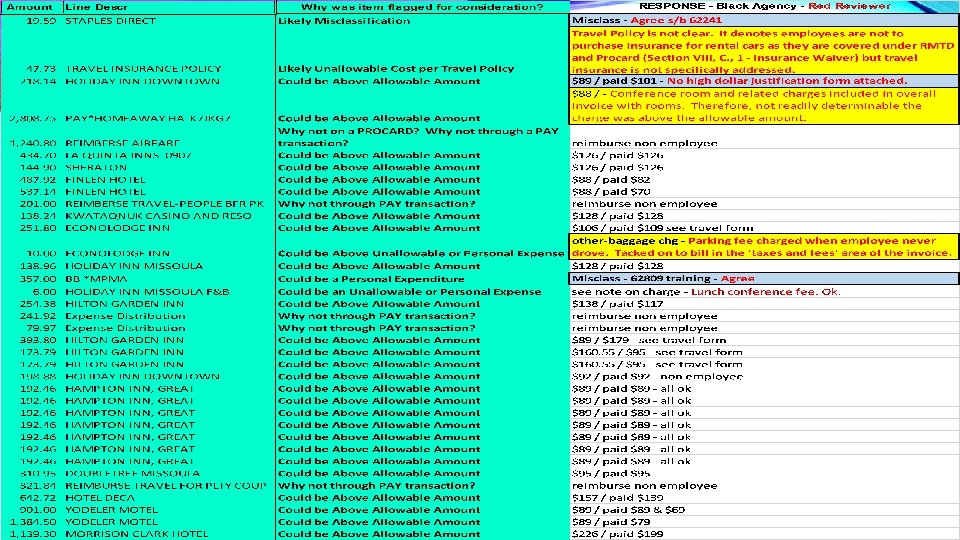

FINALLY - REPORT ON FINDINGS • After testing, review initial findings and ensure measure was not met with appropriate staff and management • Report on compliance

RESULTS FOR THE EXAMPLE • Three items selected that were of an inaccurate nature: • One Lodging Expense above Allowable Rate without Justification Form attached • Compliance Error Rate of 0. 154% • Two Expenditure Misclassifications • Total Error Rate of 0. 462% in 624 XX expenditure population • Three items of further intrigue: • One Group of Room Charges, included as a “Total Package” Conference • One Fee for Travel Insurance on Airfare • One Parking Fee when the Employee did not appear to drive • None of these are considered in either error rate noted above

Thanks for your interest and attention! COMMENTS, QUESTIONS, OR CONCERNS? Additional resources are available at: https: //sfsd. mt. gov/SAB/internalcontrols