q Receivables are amount owed to the firm

q Receivables are amount owed to the firm by outsiders in the form of regular account or written promissory note to be collected in the future. q Classification of Receivable 1. Account Receivable (A/R) A/Rs are amount owed to the firm by customer which create from selling merchandise or services on credit

NARs are amount owed the firm wich are not")

2. Non Account Receivable (NAR) NARs are amount owed the firm wich are not created from selling merchandise or services on credit Examples of non account receivable: Interest Receivable Taxes Receivable Employess Receivable Devidend Receivable

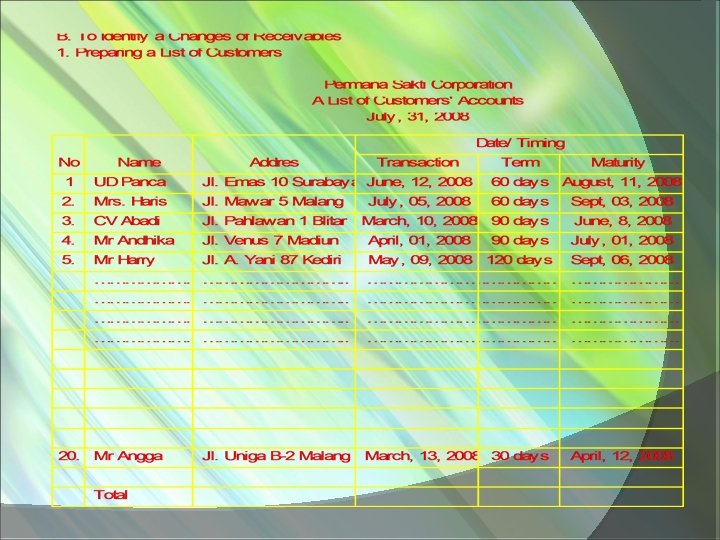

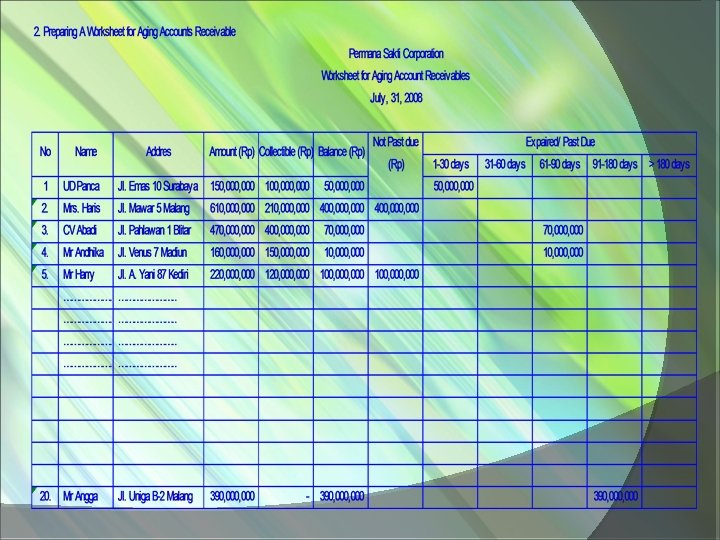

Handling of Receivables To prepare list of receivables. It consists of the name of costumers, balance of receivables, customers address, transaction date, maturity date of account, and term of credit. To prepare bill of account To prepare copy of experied/matured and attach to bill of account To send bill of account to custumers

Recording Changes / Collectible of Receivables Posting to subsidiary ledger and ledger Three methods to journalize and posting receivables a. Posting from journal to the subsidiary ledger Sales invoice Sales journal General Ledger Subsidary Ledger

b. Posting to subsidiary ledger from business transaction Sales journal Sales invoice Subsidary Ledger c. Ledgerless Bookepiry Sales journal Sales invoice Notes: Notes General Ledger - General Ledger = Control Account of Account Receivable - Subsidary Ledger = Customer account

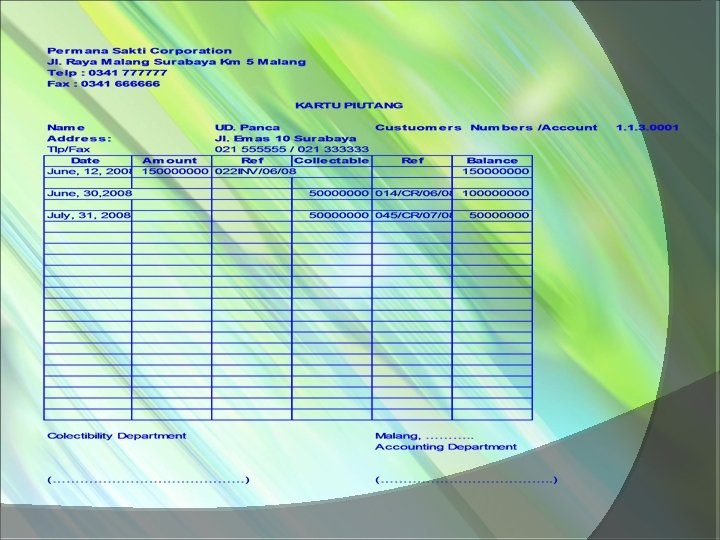

d. Recording/ posting collectibility of Account Receivables Cash Receipt General journal Control Account of Receivable Costumer Account

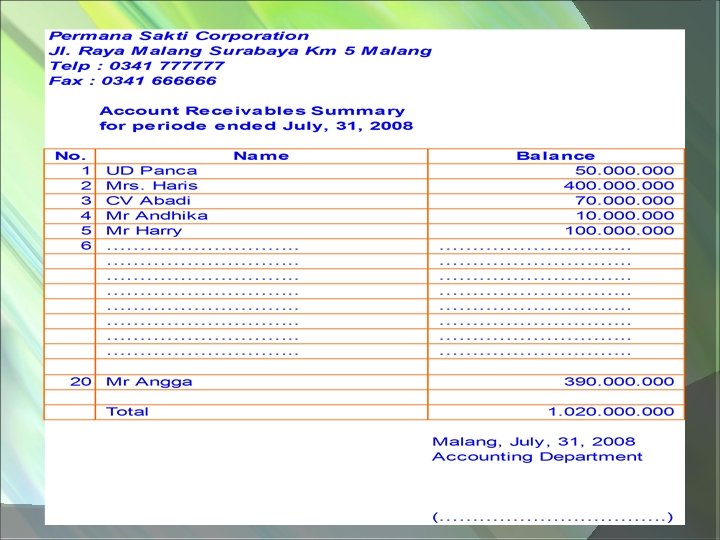

Confirmity Account Receible Balance Posting Collectibillity Account Receivable Control Account Ledger a. 100. 0 Account 00 b. 210. 0 Receivables 00 c. 400. 0 00 d. 150. 0 00 e. 120. 0 00 Subsidary UD. Panc aa. 100. 0 150. 000 Mrs. Haris 00 b. 210. 000. 0 610. 000 00 CV. Abadi c. 400. 0 470. 000 Mr. 00 Andh d. 160. 000 ika 150. 000. 0 00 Mr. Harry e. 120. 000. 0 220. 000 00

- Slides: 12