Put Together a Financial Plan Objectives Calculate your

Put Together a Financial Plan

Objectives Calculate your start-up costs. n Create a cash flow statement, an income statement, a balance sheet, and a personal financial statement. n

Prepare Financial Statements n Before you can approach a lender or investor about financing you business you will have to prepare financial statements.

These statements include: n a list of start up costs n cash flow statement n income statement n balance sheet n personal financial statement n

Your first four financial statements are estimates based on how you think your business will perform the first year. n Pro forma financial statements- financials based on projections n

Start-Up Costs n n n n n Start-up costs- one time only expenses paid to establish a business Common start-up costs include: equipment and supplies furniture and fixtures vehicles including delivery trucks remodeling; electrical and plumbing expenses legal and accounting fees licensing fees Most entrepreneurs need to borrow money to cover start-up costs.

Cash Flow Statement n n Cash flow statement- describes how much cash comes in and goes out of a business over a period of time Revenue- amount of cash coming into a business Expense- amount of cash going out of a business Shows how much money you have to pay your bills.

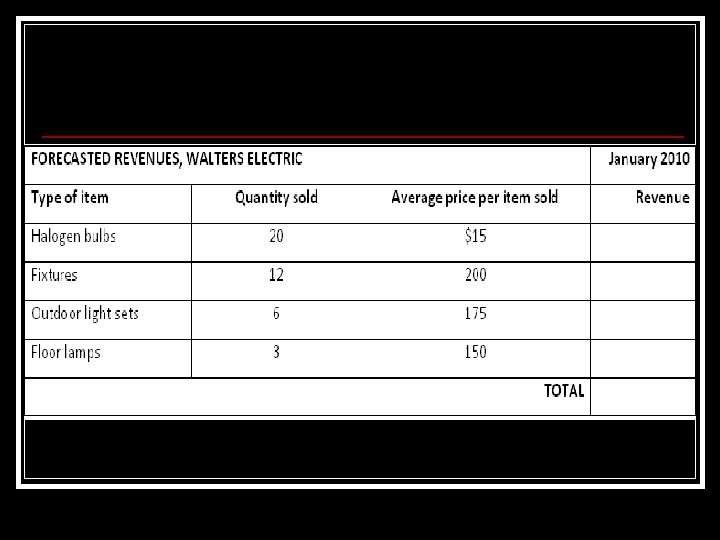

Forecast Revenues n When you forecast the amount of your revenue, you need to analyze the demand for each of your products / services and the prices you will be charging for each item.

n Example: Felicia Walters estimates that during her first month of business she will sell 20 halogen bulbs, 12 fixtures, 6 outdoor light sets, and 3 floor lamps. To calculate her total revenues, she multiplies the quantity of each item she expects to sell by the price she has set for each item.

Answer

Forecast Operating Expenses n n n n n Operating expenses- expenses incurred by a business every month May include: cost of goods rent salaries payroll taxes office supplies utilities insurance advertising

Prepare the Cash Flow Statement After making projections of revenues and expenses, you are ready to prepare your cash flow statement. n You should create monthly pro forma cash flow statements for the first year of operation and annual statements for the second and third years to give your lender an accurate picture of your cash flow over time. n

Best and Worst Case n n For a worst-case scenario, project lower revenues and higher expenses than you think you will have. Will help you identify how much cash you will need if your business does worse than expected. For a best-case scenario, project the highest revenues and the lowest expenses your business could have. Will show you how much cash you will have if your business does better than expected.

Checkpoint>> What does a cash flow statement show? n Why should you prepare both a bestcase and a worst-case pro forma cash flow statement? n

Income Statement n n Income statement- financial statement that indicates how much money a business earns or loses during a particular period Shows how much profit or loss was generated by the business Most businesses choose one year as the period represented by an income statement New businesses may create income statements as frequently as once per month

Difference from a Cash Flow Statement A cash flow statement deals with actual cash coming in and going out. It shows when you actually make a payment on an invoice or receive money from a customer. n In contrast, an income statement shows revenues you have not yet received and expenses you have not yet paid. n

Checkpoint>> n Why would a business need to prepare both a cash flow and an income statement?

Balance Sheet Balance sheet- shows the assets, liabilities, and capital of a business on a particular date n Based on the accounting equationn n assets = liabilities + owner’s equity

Assets- items of value owned by a business n Including: cash, equipment, inventory n

Liabilities- items that a business owes to others n Including: loans and outstanding invoices n

Owner’s equity- amount remaining after the value of all liabilities is subtracted from all assets n This financial statement is called the balance sheet because the accounting equation must always balance n

Types of Assets n n Fixed assets- will be used for many years Including: buildings, furniture, computers Current assets- cash, assets that can be converted to cash, and items that are used up in normal operations Including: inventory, supplies, and accounts receivable- tracks payments due for products and services provided to customers

Types of Liabilities Long-term liabilities- payable over several years n Including: bank loan n Current liabilities- payable within a short amount of time n Including: utility bills and accounts payabletracks the payments a business owes a supplier n

Uncollectible Accounts Some customers will fail to pay for merchandise they have purchased. n Allowance for uncollectible accountsshould be subtracted from asset total n

Depreciation- lowering of an asset’s value to reflect its current worth n Ensures the balance sheet shows an accurate picture of all assets n

Checkpoint>> What does the balance sheet show? n What are the two special adjustments commonly made on the balance sheet? n

Personal Financial Statement Banks are usually interested in the personal financial status of the people to whom they lend money. n Personal financial statement- balance sheet of your personal holdings n

Assignment Thinking Critically n #1 -4 n

- Slides: 29