Profit and Investment Centres Transfer Pricing Transfer Pricing

- Slides: 11

Profit and Investment Centres Transfer Pricing

Transfer Pricing • The fundamental principle is that the transfer price should be similar to the price that would be charged if the product were sold to outside customers or purchased from outside vendors.

Transfer Pricing: Important Decisions • Should the company produce the product inside the company or purchase it from an outside vendor? This is the sourcing decision. • If produced inside. At what price should the product be transferred between profit centres? This is the pricing decision.

Market Based Pricing • • • Market Price Information Freedom to source Full Information Negotiation Constraints

Cost Based Pricing • How to define cost? – Actual cost – Standard cost • How to calculate profit mark-up? – Percentage of cost – Percentage of investment

Transfer Pricing and Upstream Fixed Cost and Profits • The profit center that finally sells to the outside customer may not be aware of the amount of upstream fixed costs and profit included in the price. • Even if they are aware: They may be reluctant to reduce the profits. How to mitigate this problem?

Transfer Pricing and Upstream Fixed Cost and Profits • Agreement among the business units • Two-step pricing • Profit sharing

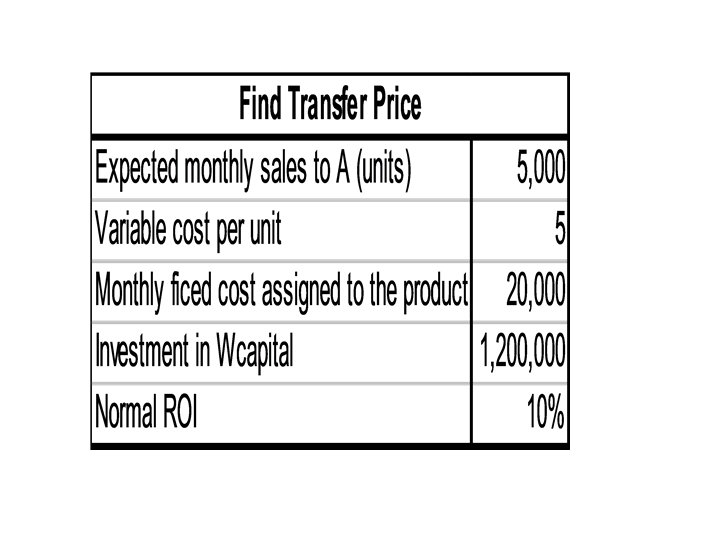

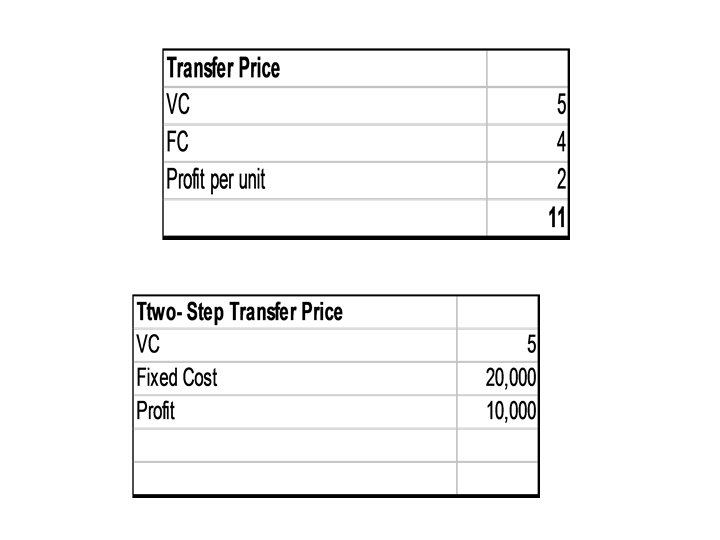

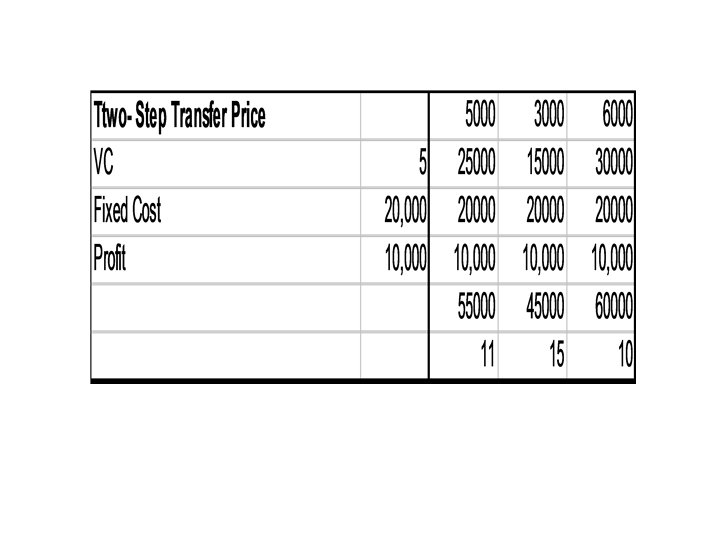

Two-step pricing • Establish a TP that include two charges: • Product Charge: Standard variable cost of production • Periodic charge: Fixed costs associated with the facilities reserved for the buying unit. • Profit may be included in the above.