Prices Chapter 6 Lesson 1 How Prices Work

• Prices are flexible in a market economy • Think")

• Prices are familiar and easily understood • Mommy “I")

• Rationing: • System where the government decides • •")

- Slides: 34

Prices Chapter 6

Lesson 1: How Prices Work • Essential Question: • How do prices help determine What, How, and For Whom to produce?

Price • The monetary value of a product as established by supply and demand • Signals: • High prices: producers to produce more and for buyers to buy less • Low prices: producers to produce less and for buyers to buy more

Advantages of Prices • help decide: WHAT, HOW, AND FOR WHOM • Prices are neutral in a competitive market economy • Result of competition b/w buyers and sellers: • More competitive = more efficient price adjustment process

Advantages of Prices (cont) • Prices are flexible in a market economy • Think about computers THEN and NOW • Allows for the “SHOCK” of unforeseen events and changes in the market • Prices have no administration cost (Efficiency) • Competitive markets find their own prices w/out interference • Prices change from one level to another gradually

Advantages of Prices (cont) • Prices are familiar and easily understood • Mommy “I want a candy bar!” • You “Can I purchase that TV? ” • No ambiguity: if it is $1 then you know you will pay $1 (plus tax in some states) • Make quick decisions • Minimum effort

discussion • Think of a simple service that you could perform after school to earn income; for example, babysitting, pet care, lawn mowing, or computer repair • How would you go about setting an hourly price for your service in order to be competitive? • Think of changing conditions that might affect the price.

Allocations Without Prices • Help us make economic decisions that “allocate” scarce resources and the product made from them • What if the PRICE SYSTEM did not exist? • Like command economies • Use another system right?

Allocations Without Prices (cont) • Rationing: • System where the government decides • • • everyone’s “FAIR” share RATION COUPON: • Obtain a certain allotted amount • Widely used during wartime Questions of Fairness? High Administrative cost Diminishes incentives Abuse and Misuse

Price as a System • Economists favor the price system • Serve as signals that help allocate resources between markets • Oil ($5 to $40 a barrel in 1970’s) • Oil is inelastic • Higher energy cost = less money to spend elsewhere • 1 ST affected full size automobiles • Gave rebates: a partial refund of the original price of the product • Closed plants, laid off workers, started to change to small production

Price as a System • Higher prices on oil = shift in productive resources • Prices help buyers and sellers allocate resources b/w markets • Economist think of the price as a system • Part of an informational network • Links all markets in the economy

Copy and answer the following questions for lesson 1 1. What are the four advantages of prices? 2. What is rationing? 3. What are the four problems with rationing? 4. How do prices help us make decisions? 5. How do prices connect markets in an economy?

Lesson 2: The Effects of Prices? • Essential Question: • What factors affect prices?

The Price Adjustment Process • Appealing feature of a Competitive Market Economy • EVERYONE who participates has a hand determining PRICES • Makes prices neutral and impartial

Cont. • Buyers and sellers have exactly the OPPOSITE hopes and desire • Buyers = find good buys at low price • Sellers = high prices and large profits • Neither can get what they WANT so adjustments must be made

The Price Adjustment Process • Compromise needs to benefit BOTH parties • DEMAND and SUPPLY make a complete picture of the market • Price adjustments help a competitive market reach market equilibrium, with fairly equal supply and demand

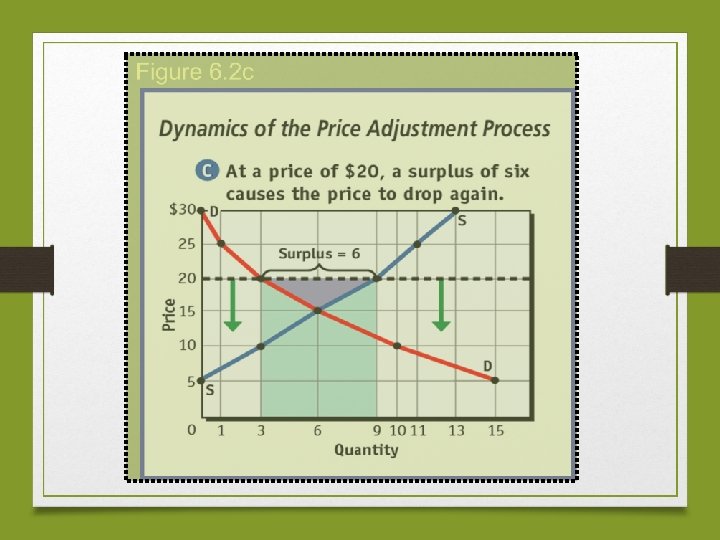

Surplus • Shows up as UNSOLD products on suppliers shelves • • Takes up space Know that the price is TOO high NEED to LOWER the price to attract buyers PRICES tend to go DOWN when there is a surplus

Shortage • Suppliers have no more product to SELL • Wished they would have charged a higher price • Result = BOTH price and quantity supplied will go UP • We do not know how much PRICE will go up

EQUILIBRUIM PRICE = occurs when supply MEETS demand

Make a Demand Supply curve using the following information Price Quantity Demanded Quantity Supplies Surplus/ shortage 11 0 52 52 9 4 44 40 7 12 36 24 5 24 24 0 3 40 12 -28 1 60 0 -60

Equilibrium Price • “Clears the market” neither a surplus nor a shortage at the end of the trading period • Economic Model of the market • CANNOT know how long it will take to reach • Price is set TOO HIGH the surplus will tend to force price down • Price is set TOO LOW the shortage will ten to force price up

Explaining and Predicting Prices • A change in price is the result of a • Change in Supply • Change in Demand • Or BOTH • Elasticity of Demand is also important when predicting prices

Explaining and Predicting Prices: Importance of Elasticity • Demand curve is MORE elastic • When a given change in supply occurs with an INELASTIC demand curve • PRICES change dramatically

Continued • When a change in supply occurs with an ELASTIC demand curve • Price change is smaller • BOTH supply and demand are INELASTIC = wider change in price • BOTH supply and demand are ELASTIC = less change in price

Explaining and Predicting Prices: Change in Demand • Changes in income, taxes, prices of related goods, expectations, and number of consumers • Example: GOLD

The Competitive Price Theory • The theory of competitive pricing represents a set of ideal conditions and outcomes; it serves as a model to measure market performance • Competitive market allocates resources efficiently

The Competitive Price Theory • To be competitive: • Sellers are forced to lower prices • Find ways to keep cost down • Competition among buyers keeps prices from falling TOO far

Complete Lesson 2 questions on handout

Lesson 3: Social Goals. Prices, and Market Efficiency Essential Question: What factors affect prices?

Controlling Prices • Government may set prices at socially desirable levels to achieve social goals • Prices not allowed to adjust to their equilibrium levels

Controlling Prices • Prices not allowed to adjust to their equilibrium levels • Price ceiling: a maximum legal price that can be charged for a product (Ex. rent controls in NYC) • Price floor: lowest legal price that can be paid for a good or service (Ex. minimum wage)

When Markets Talk • Markets send signals when prices change in response to events. . • Markets bring buyers and sellers together • Markets are said to “talk” when prices in them move up or down significantly in reaction to events that take place elsewhere in the economy. • Stock markets, for example, react quickly to interest rate changes made by the Federal Reserve.

Complete Supply and Demand curve activity and complete questions – turn in for a grade. 1. If government sets a price ceiling what will happen? Price floor? 2. Name three ways the market speaks to economist?