PRESENTED BY Shaik Ilanga salman Kaushal What is

PRESENTED BY: Shaik Ilanga salman Kaushal

What is Microfinance ? • Microfinance is a general term to describe financial services to low income individuals or to those who do not have access to typical banking services. • Microfinance Definition: According to International Labor Organization (ILO), “Microfinance is an economic development approach that involves providing financial services through institutions to low income clients.

Features of Microfinance Ø Ø Ø Ø Ø Credit To Rural Poor Loans are of small amount – micro loans Short duration loans Loans are generally taken for income generation purpose Poverty Alleviation Women Empowerment It basically caters to the poor households. It is more service oriented and less profit oriented. It is meant to assist small entrepreneur and producers.

CHANNELS OF MICRO FINANCE v SELF HELP GROUP -Bank Linkage Programme: ü ü ü Group Formation Savings Lending Meetings Record

JOINT LIABILITY GROUP Ø group comprising 4 10 individuals. Ø For the purpose of availing bank loan against mutual guarantee. Ø JLG members to engage in similar type of economic activities either in Farm & Non farm sector. Ø Simple management with little or no financial administration within the group.

JLG – SHG Difference FACTORS JLG SHG Group size 4 10 members 05 20 members per SHG Type of members Exclusively of Farmers, Oral Lessees, Share croppers, artisans, entrepreneurs Only very poor members Savings A Credit Group Savings optional Savings cum Credit Groups

Factor Loaning JLG Either Singly or Jointly")

SHG – JLG Difference (Contd. . ) Factor Loaning JLG Either Singly or Jointly by JLG by financing bank SHG Only to SHG by financing bank Maximum Restricted to Rs. 50, 000/ per loan Individual amount No such upper limit since linked to total savings etc. Of group SB A/c Group Bank A/c of SHG JLG members to be encouraged to open INDIVIDUAL ‘No Frill Accounts’

v MICRO FINANCE INSTITUITION: MFIs include NGOs, trusts, social and economic entrepreneurs, these lend small, sized loans to individuals or SHGs. They also provide other services like capacity building, training, marketing of products etc. MFIS OPERATE UNDER FOLLOWING MODELS Ø Bank Partnership Model Ø Banking Facilitators

was established as")

About NABARD Ø National Bank for Agriculture and Rural Development (NABARD) was established as an apex rural development bank in the year 1982, through an Act of Parliament. Ø Role and Function of NABARD: ü Providing Refinance to lending institutions in rural areas. ü Evaluating, monitoring and inspecting the client banks. ü Providing support to NGOs through a variety of schemes. ü asking model projects / development schemes for banks and farmers ü It prepares, on annual basis, rural credit plans for all districts in the country.

TOP 25 MFI’S: • • • • Adhikar Microfinance Pvt Ltd ASA International India Pvt Ltd Belstar Investment & Finance Pvt Ltd Chaitanya India Fin Credit Pvt Ltd Future Financial Services Ltd Growing Opportunity Finance (India) Pvt Ltd Humana People to People India IDF Financial Services Pvt Ltd Indian Cooperative Network for Women Ltd M Power Micro Finance Pvt Ltd Mahasemam Trust Margdarshak Financial Services Ltd Pahal Financial Services Pvt Ltd Rashtriya Seva Samithi Sahara Utsarga Welfare Society • • • Sahayog Microfinance Ltd Saija Finance Pvt Ltd Samhita Community Development Services Sanghamitra Rural Financial Services Sarala Women Welfare Society Shikhar Microfinance Pvt Ltd Uttrayan Financial Services Pvt Ltd Vedika Credit Capital Ltd Village Financial Services Pvt Ltd YVU Financial Services Pvt Ltd

PRODUCTS OF MICRO FINANCE: Ø MICRO SAVING Ø MICRO CREDIT Ø MICRO INSURANCE Ø REMITTANCES

• Microcredit: It is a small amount of money loaned to a client by a bank or other institution. Microcredit can be offered, often without collateral, to an individual or through group lending. • Micro savings: These are deposit services that allow one to save small amounts of money for future use. Often without minimum balance requirements. Micro insurance: It is a system by which people, businesses and other organizations make a payment to share risk. Developing their businesses while mitigating other risks affecting property, health or the ability to work. • • Remittances: These are transfer of funds from people in one place to people in another, usually across borders to family and friends.

AREA COMMERCIAL BANKS MICRO FINANCE INSTITUTION Focus Profitability , Market Share , All segment of customer A sustainable credit system for economically disadvantaged people. Customer Acquisition Banks mostly enroll customer through MFIs have stage-wise strategybranches. village meetings, formal groups, training of member of groups on financial management and then providing credit-line. Products Banks have a basket of retail product that cover savings, credit remittance etc. Credit from banks for BPL-like families is predominantly of INR 25, 000 and above; other features are varied rate of interest and varied repayment period. MFIs specialize in credit. The product is predominantly a graduated credit line with recovery by 50 week EMI. MFI credit is predominantly an average of INR 15, 000 minimum of INR 3, 000 to maximum of INR 50, 000 (housing loan up to INR 1. 25 lacs. )

Cost of Capital Average cost of Capital for Average cost of capital for Bank is 8 percent MFIs is 14 % Nature of Institution Financial Institution Service Institution Financial Goal Profit maximization Surplus to sustain

Comparison of loans and insurance in microfinance

Bhandhan loan

ANNAPURNA MICRO FINANCE

GROUP TERM LIFE INSURANCE

TATKAL BIMA

• Minimum Entry Age: 18, Maximum Entry Age: 65 • Minimum Policy Term: 5 years, Maximum Policy Term: up to 70 years of age

ü")

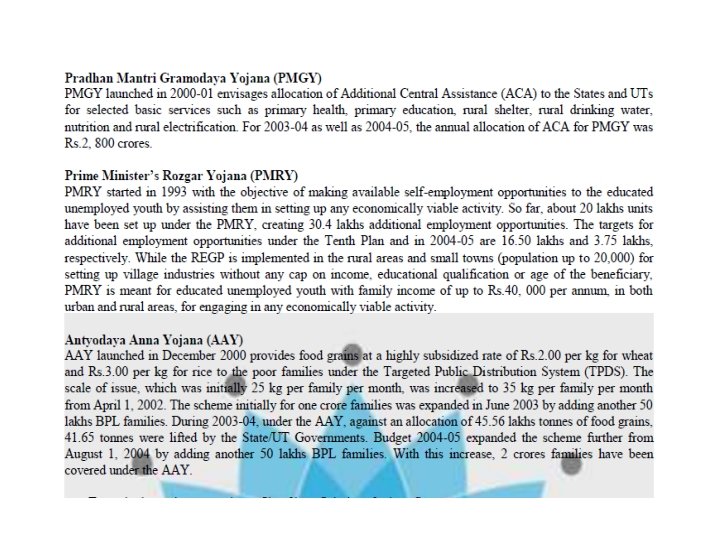

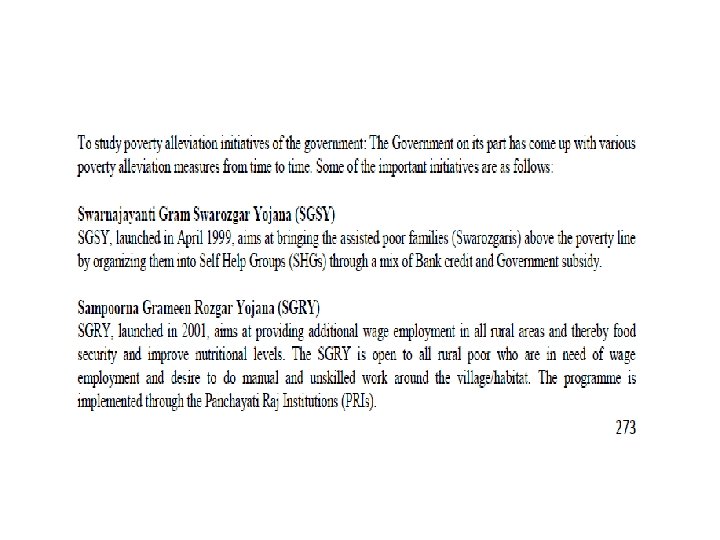

Government schemes Under micro finance in India ü Swarnajayanti Gram Swarozgar Yojana (SGSY) ü Sampoorna Grameen Rozgar Yojana (SGRY) ü Pradhan Mantri Gramodaya Yojana (PMGY) ü Prime Minister’s Rozgar Yojana (PMRY) ü Antyodaya Anna Yojana (AAY) ü Pradhan mantri jandan yojana (pmjy)

PERFORMACE:

Legal Forms of MFIs in India:

/Housing loan Loan for women Consumer")

PRODUCTS • • • Rural loan Business loan Home(Improvement)/Housing loan Loan for women Consumer loan

Procedures • PHASE 1: CLIENT RECRUITMENT & APPLICATION • PHASE 2: COMPULSORY GROUP TRAINING & GROUP RECOGNITION TEST • PHASE 3: GROUP LOAN APPROVAL • PHASE 4: DISBURSEMENT & CUSTOMER SERVICE • PHASE 5: COLLECTIONS & RECOVERY

• PHASE DESCRIPTION • The group lending process begins with marketing and promotion to potential clients. Interested clients meet with a loan officer, during which time the loan officer provides a brief overview of the institution, product features, and basic terms and conditions. Based on this information, clients form groups. The loan officer completes the application form (customer details), checks identity proofs for validation, and conducts a preliminary assessment to ascertain eligibility of clients.

")

• In this phase, the group members participate in Compulsory Group Training (CGT) followed by Group Recognition Test (GRT). The process consists of the following steps: 1) Clients learn how to sign their names and are informed of the “Client Pledge”; 2) Clients learn more about the credit products, loan terms, and conditions; 3) Members elect group and center leaders who are trained on their roles and responsibilities; 4) Credit staff visit each client home to assess income and assets (clients’ ability to repay) and collect necessary documents to meet regulatory requirements; 5) Credit staff conducts the Group Recognition Test (GRT) of clients’ understanding of the concepts taught during CGT.

• Once the group clears the GRT, loan applications are assessed and approved by the group are forwarded to the Branch Office or Regional office. The office enters the application information into the management information system (MIS) and runs a first round of checks related with customer verification (e. g. check for existing loans). After clearance from the MIS, the institution prepares for loan disbursement.

• If the loan is approved, the loan officer informs the client about the loan approval, disbursement date and other require ments. The branch office prepares disbursement documents and cash. Once the client or groups arrive at the branch, a brief disbursement speech is made. The loan amount is handed over to the customer after taking her signature on all the necessary documents. A similar process is followed by institutions that disburse loans in the field at center meetings. In this case, the loan officer carries cash and all documents to the field, makes disbursements of loans through the group and center leaders and receives signatures.

• In this phase, the loan officer collects on time repayments from clients at center meetings. In case of non repayment at the center meetings, groups are counseled and the group guarantee mechanism is reiterated. In case repayments are not received, the institution follows their escalation matrix or delinquency management process. A good escalation

Interest • • • • Justification of commercialization of microfinance Interest rates charged by money lenders are overwhelmingly higher than MFI rates. Money lenders charge an interest rate of over 10% per month. A standard money lending loan in the Philippines is the “ 5/6 loan” – for every five persons borrowed in the morning, six must be repaid in the evening. This amounts to a daily interest rate of 20%. Poor borrowers/entrepreneur can generate greater benefit from additional units of capital than a highly capitalised business can. A vegetable vendor in India can buy vegetables from a wholesaler at Rs. 2 per kg and sell the same to retail customers at Rs. 12 per kg, earning 500% income a day! For a poor micro entrepreneur, the cost of micro credit loan represents a small portion of her total business cost. A Rs. 1000 micro loan repayable in 3 months with 6% interest per month, calculated on a declining balance, costs a client only Rs. 122, which is a very tiny amount as a percentage of her total costs. When women SHG members lend to each other, they can lend on whatever terms they wish. When such arrangement prevails, the women commonly charge each other an interest rate that is substantially higher than what MFI charges to its borrowers. MFIs charging very high interest rates almost always find that demand for loans outstrips their ability to supply it. Many poor people take repeated loans. This demonstrates that loans allow them to earn more than the interest they have to pay.

• • • There is a vast amount of literature on the Internet consisting mainly of conference proceedings and discussion groups. It advocates charging market based (high) interest rate. There are no instances that a microfinance programme ran into trouble by driving away clients with interest rates that are too high. Range of investment opportunity available to rural poor is endless. When a poor woman receives Rs. 1000/ loan, she will look through her range of investment possibilities and spend her money on the one that offers highest rate of return (for example, vegetable selling can yield 500% returns in a day). A large corporate house cannot pay as high an interest rate as a poor micro entrepreneur, because they already have a lot of capital and have already “used up” most of the profitable investment options available to it. A micro entrepreneur on the other hand can derive greater relative benefit from additional units of capital, simply because she has so little capital. So she can pay a higher interest rate and still come out ahead. The access to finance to poor is a much more important issue than the cost of finance. When a poor women needs Rs. 1000/ for treatment of her ailing son, the timely availability of credit alone is important for her, not the interest rate.

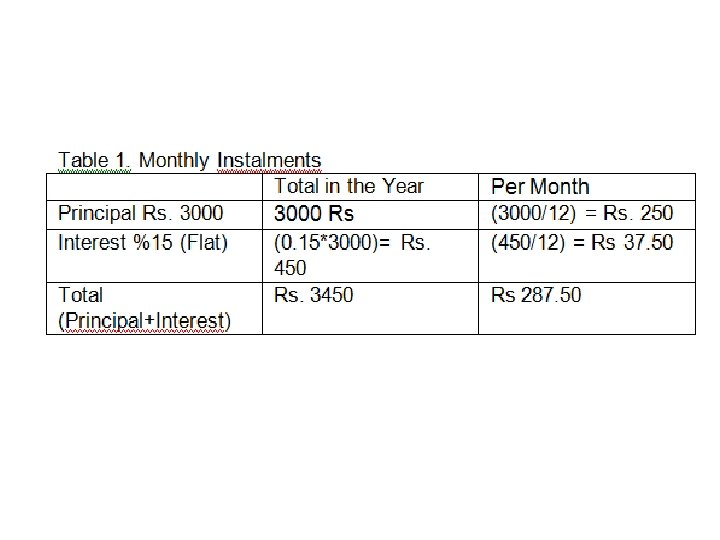

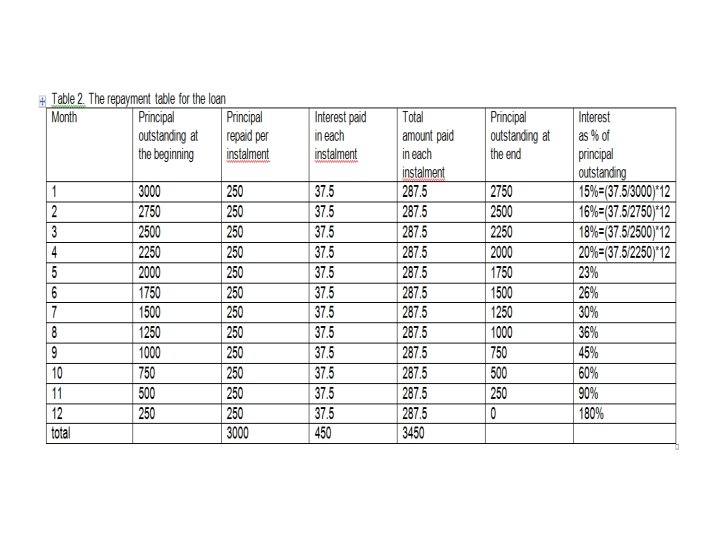

Use of Flat Rates of Interest • When flat rate of interest method is used, the interest is charged on the original face value of loan for the entire period • of loan. Though the balance loan amount of the micro finance borrower reduces with each weekly instalment payment, • the borrowers are made to pay interest on full sanctioned amount. Let us have a look on how much interest is charged • by an MFI with a stated 15% flat rate of interest per annum. Consider a simple example of a Rs. 3000/ loan given at a • flat rate of 15% interest per annum repayable at 12 monthly instalments at the end of each month. The monthly • repayment schedule is given in Table 1 and Table 2. • It can be seen from the table 2 that principal outstanding at the beginning of month 1 is Rs. 3000 and interest for the • month is Rs. 37. 50. Thus the annualised rate of interest for month 1 works out to 37. 50/3000*12= 15%; 37. 50/2750*12=16%. .

FINDING • Providing microfinance may lead to high NPA. • The most common method of availing microfinance is through forming SHG. • The normal rate of interest is higher on loan provided by MFI. • It helps in eliminating poverty and helps poor households to meet basic needs.

Recommendation • Try to get education loan from MFI as the rate of interest is low. • The product of MFI cannot be directed to any person particularly as it depends upon the need of the person. • There should be a interest rate cap to avoid high interest rate. • There is huge demand supply gap in money demand by the poor and supply by the MFI so they need to be an active participation by private sector industries.

THANKYOU

- Slides: 41