PRESENTATION TOPIC APPOINTMENT OF AUDITOR SUBMITTED TO SUBMITTED

PRESENTATION TOPIC - APPOINTMENT OF AUDITOR SUBMITTED TO SUBMITTED BY

WHO IS AN AUDITOR A person appointed and authorized to examine accounts and accounting records, compare the charges with the vouchers, verify balance sheet and income items, and state the result. OR Any individual trained to review and verify accounting data and recognized as a Chartered Accountant (CA) under the Chartered Accountant Act 1949 is deemed to be an auditor.

PURPOSE FOR THE APPOINTMENT OF THE AUDITOR ØThe purpose of the auditors in the company is to protect the interests of the shareholders. ØThe auditor is obligated by law to examine the accounts maintained by the directors and inform them of the true financial position of the company. Ø Auditor gives his independent opinion to the owners or shareholders of the company to protect and keep the company in a safe financial condition

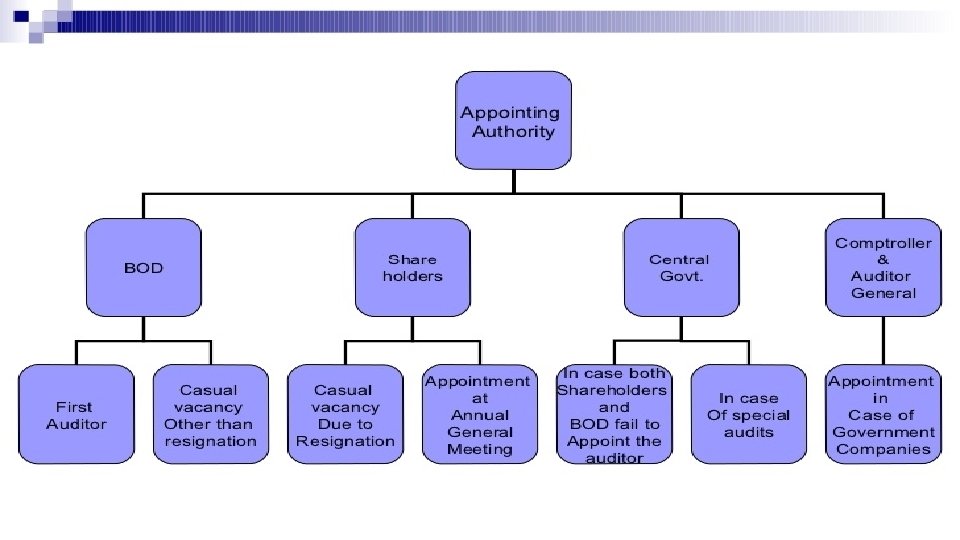

APPOINTMENT OF AUDITOR BY BOD IN CASE OF FIRST AUDITOR 1. BOD should appoints an individual or a firm as the first auditor of the company Within thirty days from the date of the registration of the Company. 2. As per provision to section 142(1) remuneration of the first auditor can be decided by the Board. 3. However, in a case where the Board of Directors fails to appoint the first auditors of the company they shall inform the members of the Company. Thus, the members shall appoint the first auditors of the company within 90 days at an extraordinary general meeting. 4. The First auditors may remain in office until the conclusion of the First Annual General Meeting

APPOINTMENT OF AUDITOR BY BOD IN CASE OF CASUAL VACANCY OTHER THAN RESIGNATION If a Casual Vacancy arises due to casual vacancy other then resignation then Board of Directors of Company has the power to appoint Auditor. PROCEDURE Ø: Time Period: BOD of Company within 30 days of arisen of Casual Vacancy appoint a Statutory Auditor on place of old Auditor. ØTerm of Appointment: Such Auditor will become auditor of the Company upto ensuing the consent form and eligibility certificates. ØAnnual General Meeting - Hold the Board Meeting and pass Board Resolution for appointment of auditor.

PROCEDURE FOR APPOINTMENT ØForm Filing: BOD will file ADT-1 within 15 days of passing of Board Resolution. ØCircular Resolution: Circular Resolution passed by Board Resolution is enough for appointment of auditor in case of casual vacancy.

APPOINTMENT OF AUDITOR BY SHAREHOLDERS IN CASE OF AGM OR SUBSEQUENT AUDITOR 1. As Per Section 139(1) Every Company’s Shareholders Shall Appoint At Its 1 st Annual General Meeting An Individual Or A Firm As An Auditor Of The Company 2. Appointment of an auditor can be done by passing the ordinary resolution 3. Auditor Shall Hold From The Conclusion Of That Meeting Till The Conclusion Of Its Sixth Annual General Meeting And Thereafter Till The Conclusion Of Every Sixth Meeting 4. As Per Section 142(1) Remuneration Of The Auditor Of A Company Shall Be Fixed In Its General Meeting Or In Such Manner As May Be Determined Therein 5. In case of foreign company, nationalized bank and any corporation formed under any special Indian law appoints auditor only by passing special resolution.

APPOINTMENT OF AN AUDITOR BY SHAREHOLDERS If a Casual Vacancy arises due to resignation of auditor then new auditor will be appoint by Board of Director but such appointment shall be approve by the Shareholder in their Extra-Ordinary General Meeting. PROVISIONS: Time Period: BOD of Company within 30 days of arisen of Casual Vacancy appoint a Statutory Auditor on place of old Auditor. Extra Ordinary General Meeting: Such appointment must be approved by the shareholders in their Extra. Ordinary General Meeting within 90 days of appointment of such auditor. Term of Appointment: Such Auditor will become auditor of the Company upto ensuing Annual General Meeting. He is liable to retire or may be re-appoint on ensuing AGM. Ordinary Resolution: Such appointment shall be approve by passing of “ORDINARY RESOLUTION” in General Meeting. Form Filing: BOD will file ADT-1 within 15 days of appointment of Auditor in Extra Ordinary General Meeting. Circular Resolution: Circular Resolution passed by Board Resolution is enough for appointment of auditor in case of casual vacancy. Filing of MGT-14: No need to file e-form MGT-14 in case of appointment of Auditor.

PROCEDURE BY COMPANY • File e-form ADT-1 within 15 days of passing of Ordinary Resolution in General Meeting. Resignation: {Section 140(2)} • Resigning Auditor will send letter of his resignation mentioning the reason of resignation to Company within 30 days of Resignation. • Resigning auditor will file e-form ADT-3 along with detailed resignation letter with ROC within 30 days of his resignation.

APPOINTMENT OF AN AUDITOR BY CENTRAL GOVERNMENT The central government may appoint an auditor in the following situations. 1. When no auditor is appointed or reappointed in a annual general body meeting. 2. Where a special resolution is required (discussed elsewhere in this chapter) for appointment of auditors, and the company fails to pass such resolution at the time of appointment. 3 Where the auditor, appointed at the AGM has not accepted the appointment. 4. Where the appointment of the auditors at AGM is void ab initio. 5. Special audit , in case of company violates the rules and regulation.

APPOINTMENT OF AN AUDITOR BY CENTRAL GOVERNMENT NOTES – 1. The company should apply to the Central Government, along with the list of names of the auditors, whom the company suggests for appointment of auditor. The Central government, after due consideration, appoints the auditor. 2. If the company fails to inform the central government about the situation mentioned above, the company and officers in default are punishable with fine to the extent of Rs 500/-.

APPOINTMENT OF AN AUDITOR BY CAG ØIn the case of a Government Company, the Comptroller and Auditor-General of India shall appoint the first auditor within sixty days from the date of registration of the company. ØIf the Comptroller and Auditor-General of India fail to appoint such auditor within the period of sixty days, the Board of Directors shall appoint the first auditors within the next thirty days. ØHowever, if the Board of Directors also fails to appoint the first auditors within thirty days they shall inform the members of the Company. ØThus, the members shall appoint the first auditors of the company within sixty days at an extraordinary general meeting. Also, the auditor so appointed shall hold the office until the conclusion of the first AGM.

APPOINTMENT OF AN AUDITOR BY CAG ØIn respect of a financial year, the Comptroller and Auditor-General of India shall appoint an auditor within a period of one hundred and eighty days from the commencement of the financial year. Such auditor shall hold office until the conclusion of the annual general meeting. ØAlso, the Comptroller and Auditor-General of India shall fill any casual vacancy in the office of the auditor of the Government Company within thirty days. If the Comptroller and Auditor-General of India fail to fill such vacancy within the period of thirty days, the Board of Directors shall fill such vacancy within next thirty days.

regarding the intention of")

Procedure for appointment of auditor 1. Intimate the proposed auditor(s) regarding the intention of appointing him/it as auditor and ask whether he/ it is eligible and not disqualified to be appointed as auditor of the company. 2. Obtain consent & certificate from auditor. 3. If audit committee required to be constituted under section 177, then obtain its recommendation (Section 139(11)). 4. Call Board meeting. 5. Approve the appointment of auditor at the first Board Meeting. 6. Intimate the auditor and file with ROC form ADT-1(to be attached in form GNL-2 as per MCA circular 09/2014 dated 25 th April, 2014) within 15 days.

THANK YOU

- Slides: 16